Micron, SanDisk Both Plunge Over 6%; Apple, Microsoft Price Hikes Backfire on Market, Memory Stocks Face Loosening Earnings Logic

AI Podcast

On June 29 Eastern Time, US memory stocks declined as investors questioned whether sharp price hikes might dampen end-consumer demand. Despite persistent supply shortages driven by AI infrastructure needs—expected to last until 2027—major manufacturers like Samsung, SK Hynix, and Micron face a class-action lawsuit alleging price manipulation. Concurrent aggressive capacity expansions, including South Korea's $5.2 billion investment, aim to double DRAM production by 2028. Analysts warn that simultaneous global capacity increases could trigger an oversupply downcycle if AI demand fails to meet expectations, despite current bullish sentiment from firms like Morgan Stanley.

Tradingkey - On June 29 Eastern Time, US memory stocks suffered a collective setback today after the South Korean government announced its largest-ever investment plan for the semiconductor and AI industries, with SanDisk ( SNDK) and Micron ( MU) both falling over 6%.

This is another new catalyst for the memory sector following Micron Technology's optimistic earnings outlook released last week. However, judging by today's market reaction, investors do not seem to buy into it. It is reported that Apple and Microsoft's Xbox raised prices on the same day last week, prompting the market to reassess whether this round of sharp memory price increases—which drove profit expansion in the chip sector—comes at the expense of sustained pressure on end-consumer demand.

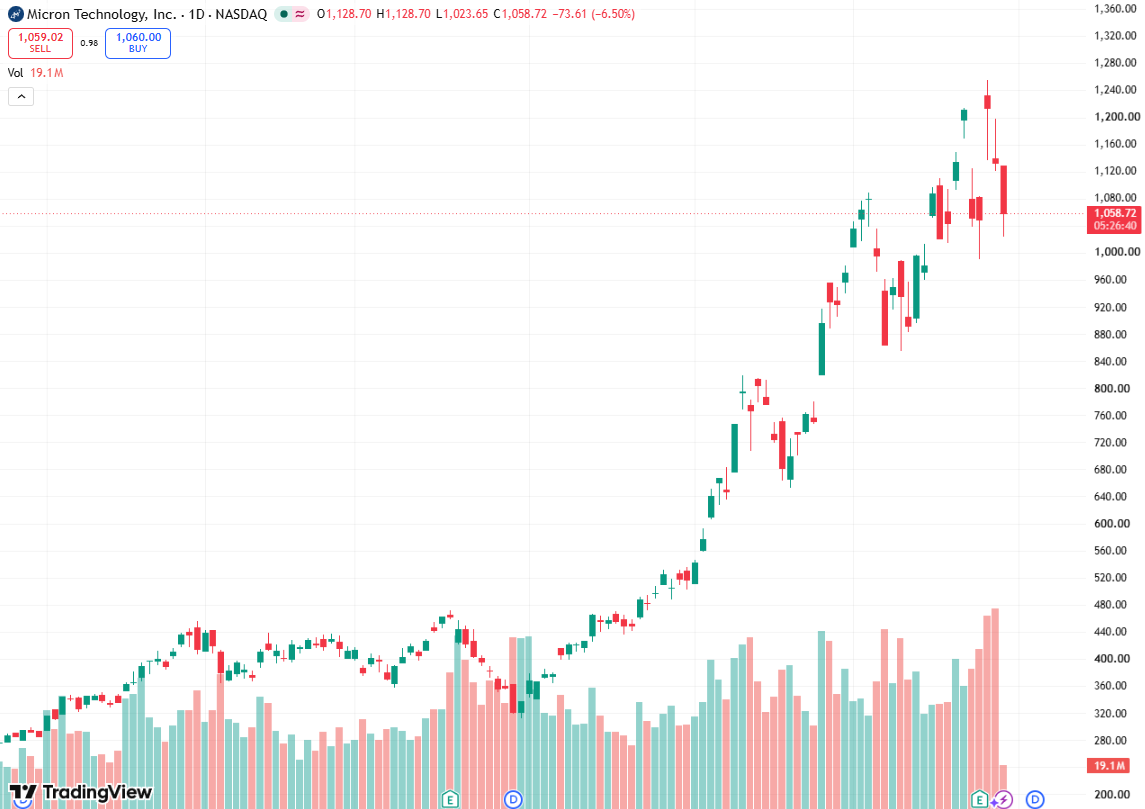

[Source: TradingView]

Currently, the global memory shortage crisis is intensifying. The CEO of Synopsys (SNPS), a leader in the EDA and semiconductor IP space, stated that most memory chips from the world's top manufacturers are "going directly to AI infrastructure, but many other products also require memory, so these other markets are now struggling due to insufficient capacity." He also emphasized that the chip "shortage" will persist into 2026 and 2027.

Recently, market research firm Counterpoint Research stated that in the current memory market, demand will not decrease even if prices rise. The supply shortage is unlikely to be substantially resolved until at least the second half of 2027, as the demand for server DRAM and High Bandwidth Memory (HBM) to build AI data centers has already outstripped the demand of the entire market.

Morgan Stanley recently stated that memory chip stocks performed strongly in 2025 and will continue to lead the market in 2026, but the bank believes this strong run is not yet over. Morgan Stanley noted that there is increasingly no quick fix for memory, which will drive tight memory supply to persist for two to three years (or longer). This suggests underlying weakness in DRAM, and the same goes for NAND flash.

Against this backdrop, the world's three largest memory suppliers—Samsung, SK Hynix, and Micron—have been hit with a class-action lawsuit by US consumers, who accuse them of manipulating memory prices and restricting global supply.

According to the complaint, these three companies monopolize nearly the entire global DRAM market supply, yet they tightened the supply of legacy DRAM products during a period of surging prices, further escalating the already severe memory shortage crisis.

In addition to facing litigation pressure, the three major memory suppliers have also kicked off an unprecedented capacity race. In its earnings report last week, Micron stated that its capital expenditures for the full fiscal year 2026 will reach approximately $27 billion, with quarterly capex expected to rise even further in 2027.

Today, South Korean President Lee Jae-myung announced an investment of approximately 800 trillion won (about $5.2 billion) in the southwestern region to build four chip factories, with Samsung Electronics and SK Hynix each constructing two, aiming to double DRAM production capacity within five years. On the other hand, South Korea plans to invest over 1,000 trillion won in the AI data center sector by 2035.

Market analysts noted that with all three memory suppliers expanding capacity simultaneously, if future AI computing power and end-user demand fall short of expectations, the industry could return to an oversupply downcycle after the centralized release of new capacity in 2028.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.