Mobile Phone Market Cools, Why Apple Posted 20% Growth in China Market in Q1

AI Podcast

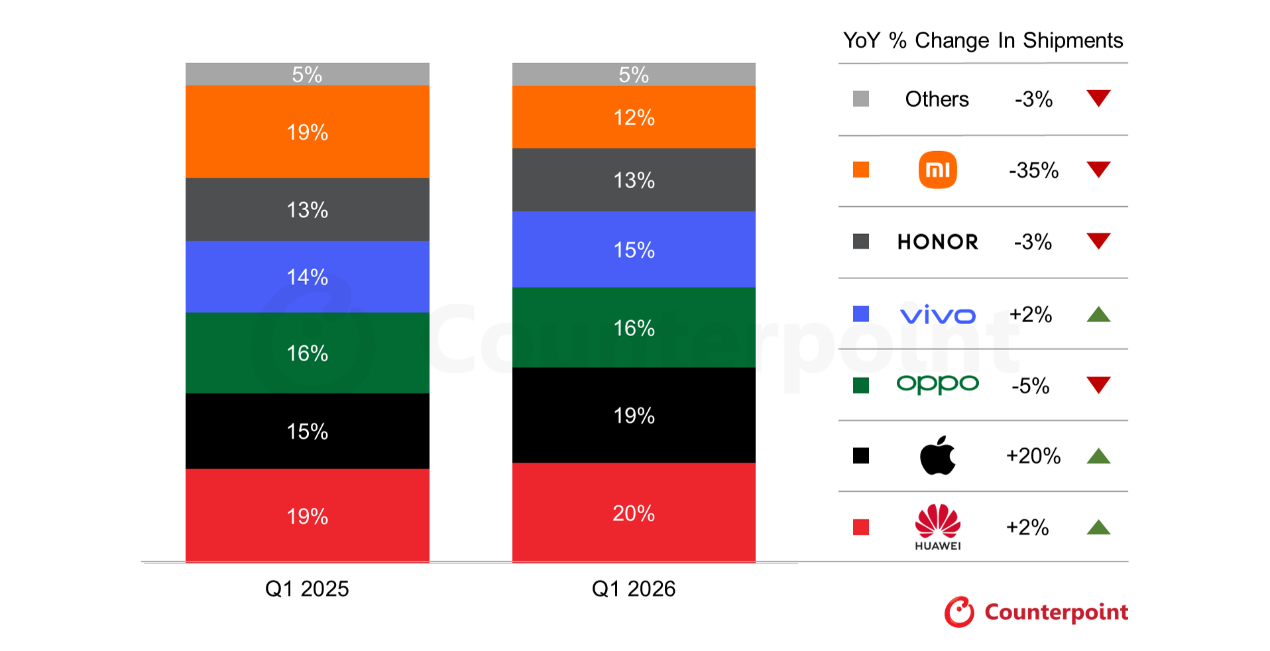

In Q1 2026, China's smartphone market saw a 4% year-on-year shipment decline, attributed to supply chain issues and rising memory chip prices. Apple defied the trend with 20% shipment growth and a 19% market share, securing second place. This performance was driven by its value proposition, durability perception, and internal cost absorption for the iPhone 17 series. Huawei led with 20% market share and 2% growth, bolstered by its product synergy and local supply chain. Other manufacturers, like Xiaomi, faced significant declines due to cost pressures and pricing strategies. Elevated component costs are expected to continue impacting the market, with full-year shipments projected to fall 9%.

TradingKey - Against the backdrop of overall industry pressure, Apple emerged as the standout highlight in the Chinese smartphone market in the first quarter of 2026, driven by a 20% shipment growth rate.

A report on the Chinese smartphone market for the first quarter of 2026, released by Counterpoint Research on April 17, showed that overall domestic shipments fell 4% year-on-year, impacted by the dual factors of supply chain disruptions and surging memory chip prices. However, Huawei and Apple continued to perform strongly despite the general market downturn.

Counterpoint analyst Ivan Lam stated: "The rise in component costs has begun to push up retail prices, affecting not only the pricing of existing models but also raising the launch prices of new devices. This trend is expected to cause the Chinese smartphone market to continue facing significant downward pressure in the second quarter."

He added: "However, the premium smartphone segment has demonstrated strong resilience; major OEMs are effectively stimulating replacement demand by introducing innovative features such as breakthrough imaging hardware, foldable screen technology, and AI smart assistants."

Apple Bucks the Trend to Break Through

Apple's shipments surged 20% year-on-year, outperforming other leading manufacturers by a wide margin. It climbed to second place in the industry with a 19% market share, trailing only Huawei, which held a 20% share.

While most competitors raised prices due to cost pressures, the value proposition of Apple's products became increasingly prominent. Chinese consumers widely recognize the iPhone's durability of at least three years, and this long-term value has become a key decision factor in a market where consumers are cautiously weighing costs.

Additionally, the strong performance of the iPhone 17 series, targeted promotional price cuts, and deep supply chain expertise have enabled Apple to absorb rising cost pressures internally, facilitating further market share expansion.

In fact, Apple's growth is not a short-term spike but a structural continuation. As early as the second quarter of 2025, iPhone sales in China ended an eight-quarter decline with an 8% growth rate. By October 2025, the iPhone accounted for one-fourth of China's smartphone sales, reclaiming a dominant position.

Counterpoint specifically noted that, leveraging its high-end product portfolio and robust supply chain management, Apple is the best-positioned manufacturer to weather the current global memory chip shortage and is expected to continue expanding its market share through internal cost absorption in the short-to-medium term.

Furthermore, Apple's recovery in the Chinese market is remarkably strong. By recent industry standards, this rebound appears sustainable; even after a two-year market downturn, the brand's allure among Chinese consumers has not faded.

However, it is worth noting that the core factors driving the first-quarter sales surge—relative cost-effectiveness amid overall market weakness, the gap created by competitors' collective price hikes, and the product cycle dividends of the iPhone 17 series—are not stable long-term pillars of growth.

Huawei Regains Top Spot

Huawei continued to lead the domestic market with 2% year-on-year growth, while regaining the top spot in the Chinese market with a 20% market share, marking its highest quarterly market share since the fourth quarter of 2020.

Huawei's growth momentum was driven by synergy across its entire product line; improved supply of the flagship Mate 80 series, along with core strengths like HarmonyOS 5.0 and NearLink technology, continued to enhance brand appeal and attract high-end users seeking cutting-edge experiences.

The Enjoy 90 series, which targets the budget market, successfully reached price-sensitive consumers during Lunar New Year promotions with its affordable pricing and solid performance, becoming a vital pillar for overall shipments.

Crucially, Huawei's heavy reliance on its local supply chain provided a natural cost buffer during periods of volatile global memory prices, allowing it to maintain price stability while competitors raised prices, further consolidating its market standing.

Survival space for small and medium-sized manufacturers is under pressure.

While Huawei and Apple's performances remain relatively stable, other brands are facing severe challenges.

Xiaomi suffered a major setback in first-quarter shipments, which plunged 35% year-on-year as its market ranking slipped to sixth. Analysts believe this was primarily due to Xiaomi's cautious pricing strategy under the pressure of rising memory costs, which weakened product competitiveness, as well as a high base effect from the same period last year caused by government subsidies and significant price cuts, making the year-on-year comparison look particularly bleak.

Bucking the market chill, vivo achieved a 2% growth in shipments, largely driven by strong sales of low-to-mid-range models during the Lunar New Year period; in particular, the Y50 and S50 series successfully attracted price-sensitive consumers with their precise market positioning and stable performance.

OPPO’s performance was mixed, with overall shipments declining 5% year-on-year, though its sub-brand OnePlus achieved high-speed growth of 53% fueled by the strong performance of the Ace 6 and Turbo 6 series. However, OPPO's "profit-first" strategy led it to be among the first to raise prices on certain legacy models, a move that suppressed market demand to some extent.

Market research firms have issued warnings that memory chip costs are expected to remain elevated throughout 2026, forcing smartphone manufacturers to make difficult choices between maintaining profit margins and securing shipment volumes. As major brands generally raise retail prices for both new and old models, market demand may weaken further, and the consumer replacement cycle could continue to lengthen.

Analysts expect the Chinese smartphone market to remain under significant pressure in the second quarter of 2026; although the 618 shopping festival may bring a brief recovery in demand, it is unlikely to reverse the overall downward trend. Full-year smartphone shipments are projected to fall 9% year-on-year, indicating that the market winter will persist.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.