Full Recap of Jensen Huang's Taipei Speech: Who Won, and Whose Moat Is Quietly Crumbling

AI Podcast

Nvidia unveiled new PC and data center chips, alongside a $150 billion Taiwan investment. While Nvidia gained, Qualcomm fell significantly on concerns over its PC market share. However, Qualcomm's core strengths in smartphone and automotive chips remain intact. Intel faces intensified pressure in both data center and PC markets. ARM Holdings, benefiting from its royalty model on all ARM-architecture chips, saw a substantial gain. TSMC is a confirmed beneficiary due to its critical CoWoS packaging capacity, essential for Nvidia's new platforms. Nvidia's long-term valuation hinges on its transition to a platform company, with key milestones in 2027.

On June 1st, at the Taipei Music Center, Jensen Huang stood on stage for nearly two hours in his signature leather jacket. He unveiled three things: a chip for ordinary computers, a CPU dedicated to data centers, and a reaffirmation of a $150 billion annual investment commitment in Taiwan.

When the speech ended and US markets closed, Nvidia had risen about 6%, Qualcomm had fallen 8.78%, Intel had fallen 4.67%, and AMD had fallen 1.16%. Many people's first reaction after seeing the day's market moves was: Nvidia won, Qualcomm is finished.

That judgment isn't wrong, but it only tells half the story. What investors really need to think through is which narratives changed after this event, which ones didn't, and where money should go in the next year or two. Let's go through them one by one.

First, Let's Recap the Announcements

The core of what Jensen Huang brought this time was three things.

The first is RTX Spark. This is Nvidia's first self-designed chip for personal computers, with chip platform codename N1X, co-developed with Taiwan's MediaTek, manufactured on TSMC's 3nm process. It features 20 CPU cores plus a Blackwell architecture GPU, supports up to 128GB unified memory, and delivers 1 PFLOP of AI computing performance. It launches this fall with the first wave of laptops, with partner brands including Dell XPS 16, Lenovo Yoga Pro, Microsoft Surface Laptop Ultra, HP OmniBook, ASUS ProArt, MSI, and Acer. Beyond laptops, it will also appear in Mini PC desktops.

Source: Nasi Lemak Tech

The second is the Vera CPU. This is Nvidia's first standalone CPU chip entering the data center CPU market, delivering 1.8x faster performance than x86 on AI inference workloads, with first customers including OpenAI, Anthropic, and SpaceX. We'll discuss the significance of this later in more detail, because the logic it implies is more far-reaching than RTX Spark.

The third is the $150 billion annual Taiwan investment commitment, along with Jensen Huang's personal visit to TSMC Chairman C.C. Wei to lock in the CoWoS advanced packaging capacity needed for mass production of the Vera Rubin platform. The Vera Rubin platform entered mass production in Q1 2026, the first Vera Rubin rack is already running in Microsoft Azure, with full delivery to major cloud providers beginning in H2 and mass production ramp of the NVL72 rack completing by year-end.

Three Announcements at a Glance

Product | Positioning | Process | Launch/Delivery | Key Competitors |

RTX Spark (N1X) | PC / Laptop SoC | TSMC 3nm | Fall 2026 | Qualcomm Snapdragon X, Intel Core Ultra |

Vera CPU | Data Center CPU | TSMC 3nm | H2 2026 | Intel Xeon, AMD EPYC |

Vera Rubin Platform | AI Data Center GPU+CPU integrated | TSMC 3nm (N3P) | H2 2026 delivery | AMD MI450 series |

A brief note on the name "Vera Rubin." Nvidia has a long tradition of naming chip architectures after scientists — Ada Lovelace (mathematician, computing pioneer), Grace Hopper (computer scientist), and David Blackwell (mathematician) have all appeared in Nvidia's product line. Vera Rubin was an American astronomer who, in the 1960s and 70s, discovered direct evidence for dark matter in the universe through observations of galactic rotation curves — a mysterious substance invisible and intangible, yet comprising about 85% of all matter in the universe. Naming the next-generation flagship platform after her, Jensen Huang's metaphor is thought-provoking: the power of AI may be like dark matter — you haven't fully seen it yet, but it is already reshaping the underlying rules by which everything operates.

Source: astronomy.com

Qualcomm: Possibly Emotionally Oversold

Qualcomm fell 8.78% on the day — the largest drop among all affected stocks. The surface logic is straightforward: Nvidia's RTX Spark directly targets the Windows ARM PC market, and Qualcomm's Snapdragon X series is currently almost the sole supplier in that market. Nvidia brought Microsoft, Dell, and Lenovo into the arena, and Qualcomm's lunch is being taken away.

But this logic has several important problems in its details.

First, Qualcomm's share of the PC market is not large to begin with. When the Snapdragon X series launched in 2024, shipments were under 1 million units; by early 2025, Qualcomm itself claimed approximately 10% of the high-end PC market (above $800). That 10% figure sounds significant, but it only covers the premium segment, and it took nearly a year to climb to. The entire PC market ships about 300 million units annually — Qualcomm's scale is simply not in the same league as Intel's 70%+ share.

Second, RTX Spark doesn't launch until fall of this year, with the first products explicitly positioned at the premium price tier — Nvidia and Microsoft haven't disclosed specific pricing, only saying it targets the high end. Even if the launch goes smoothly, how many units can actually ship by the end of 2026 remains an open question, and it won't show up in Nvidia's financials in the short term.

More importantly, Qualcomm's real moat was never in PCs. Many people, the moment they hear Nvidia is making PC chips, mentally jump to Qualcomm and assume it's been hit in a vital spot. But if you decompose Qualcomm's revenue structure, PC chips actually represent a very small share — and this was a new business Qualcomm only began building out in the past two years. Given that base, even if it gets cut in half, the impact on overall valuation is quite limited.

What truly sustains Qualcomm as a company is two things.

The first is smartphone baseband chips. This business is Qualcomm's core, built over decades. For every Android flagship sold globally, it almost certainly runs a Qualcomm baseband chip — Samsung, Xiaomi, OPPO, vivo all rely on Qualcomm for their high-end models. That position isn't easily replaced, because baseband chip development cycles are extremely long, certification processes are complex, and carrier compatibility has to be worked out carrier by carrier. MediaTek is catching up, but Qualcomm's advantage remains clear. RTX Spark is a PC chip — it doesn't even touch this business.

The second is automotive chips. Qualcomm's Snapdragon Ride platform has been making inroads into automakers one by one over the past two years. The logic here resembles the smartphone business: once an automotive chip enters a vehicle's supply chain, replacement costs are extremely high, because the entire software stack, sensor interfaces, and OTA upgrades are deeply bound to the chip — moving anything is a cascade of complications. And automotive product cycles are far longer than smartphones; one vehicle model sells for five years, and the chip eats five years' worth of volume with it. What Qualcomm is building here is a long-tail revenue model, not a one-time transaction.

Now look at Qualcomm's recent performance. Just about a month before Computex opened — on April 29th — Q2 FY2026 earnings were released, beating market expectations. The CEO also announced on the call that they had secured a custom chip order from a large hyperscale cloud customer, sending the stock continuously higher, with cumulative gains of over 34% through the end of May. Two things drove that rally: first, the data center custom chip order from a major hyperscale customer; second, automotive chip revenue reaching a record high of $1.3 billion, up 38% year-over-year. Neither of these has anything to do with the PC market. Qualcomm is quietly pushing its business boundaries toward data centers and automotive — that was the real reason the market got excited about that earnings report.

None of these dynamics changed after Jensen Huang's speech.

Qualcomm Business Breakdown: PC Is Just a Sliver

Segment | Share (Q2 FY2026) | Impact from RTX Spark |

Smartphone Baseband (Handsets) | ~57% | No impact |

IoT (incl. Snapdragon X PC chips) | ~16% | PC portion faces direct competition |

Technology Licensing (QTL) | ~13% | No impact |

Automotive (Snapdragon Ride) | ~13% | No impact |

So Qualcomm's decline on the day was more of an emotional reaction to the narrative of PC market share being taken away. If you believe Qualcomm's smartphone and automotive moats remain intact over the next two to three years, that drop looks more like an observation opportunity than a signal worth chasing to the downside.

Intel: Fighting on Two Fronts — The One That Should Actually Worry You

If Qualcomm was emotionally oversold, Intel is the company whose long-term thesis was most substantively damaged by this event.

The story starts with the data center CPU market. Before the AI wave, Intel held over 90% share in server CPUs — effectively a monopoly. Over the past three years, AMD's EPYC series has steadily eroded Intel's share through superior performance-per-watt, with AMD's revenue share in server CPUs approaching 40% by 2025. The data center CPU moat Intel depended on for its survival has been chipped away piece by piece.

Now the Vera CPU has arrived. Nvidia announced that its first Vera CPU customers are OpenAI, Anthropic, and SpaceX — precisely the top-tier customers with the most intensive AI infrastructure investment. Jensen Huang said this opens a new $200 billion market, and that market was precisely the heartland of Intel's data center business.

Data Center Server CPU Market Share Shifts

Period | Intel | AMD | ARM/Other |

Around 2020 | ~90% | ~10% | Negligible |

End of 2024 | ~64% | ~36% | Small and growing |

End of 2025 | ~59% | ~41% | Small and growing |

2027 Forecast | Continued decline | Continued rise | Growth accelerated by Nvidia Vera entry |

Meanwhile, Intel's pressure in the PC market is growing too. RTX Spark targets high-end PCs, AMD's share in the mainstream PC market is already approaching 30%, and now Nvidia is knocking at the door.

More troublesome is Intel's technology roadmap. Intel has been pinning hopes on the 18A process node to reclaim process leadership, but yield issues remain opaque, and 18A simultaneously introduces two entirely new technologies — RibbonFET and PowerVia — a combination no company in the industry has ever attempted simultaneously before, making the technical risk extremely high. With simultaneous pressure on technology, market share, and customer relationships, Intel's situation is the most difficult it has been in decades.

One detail worth noting: just around the time of the speech, Intel and Nvidia announced a collaboration in which Intel will manufacture custom x86 CPUs integrated into Nvidia's AI infrastructure platform. Many interpret this as competitive easing, but it can also be viewed from another angle: Intel has made its CPU a component supplier within the Nvidia platform. From an industry positioning standpoint, this is not a partnership of equals — it is a signal of control being transferred.

AMD's position in this event is relatively better. AMD's EPYC share in data center CPUs is already at a historic high, and the Vera CPU only just entered the market this year — it will take time to truly dent AMD's EPYC. AMD is also Nvidia's only competitor with real substance in the GPU market. The Vera CPU is a threat AMD needs to monitor closely over the next two to three years, but it hasn't yet created a direct immediate shock.

ARM Holdings: The Quietest but Possibly Most Important Winner

ARM Holdings had the largest gain on the day, rising 15%. Many people saw that number with some confusion: ARM doesn't make GPUs or PCs — why did it rise so much?

This is the most thought-provoking aspect of this whole event.

ARM's business model is very distinctive: it doesn't manufacture chips — it sells blueprints for chip design, i.e., architecture licenses. Every time a chip company uses the ARM architecture to design a chip, it pays ARM a license fee; every time a chip is sold, ARM collects a royalty. RTX Spark uses ARM architecture. The Vera CPU also uses ARM architecture. This means every PC chip or data center CPU that Nvidia sells puts money in ARM's pocket.

This logic doesn't apply only to Nvidia. Apple's M-series chips are ARM architecture. Amazon's Graviton is ARM architecture. Google's Axion is ARM architecture. Qualcomm's Snapdragon is ARM architecture. ARM is essentially the entity in this AI chip war from which it collects its toll no matter who wins. To use a blunter metaphor, ARM is the highway toll booth: Nvidia is on the left, Qualcomm is on the right, Apple, Amazon, and Google are passing through the middle — the more traffic, the more ARM collects.

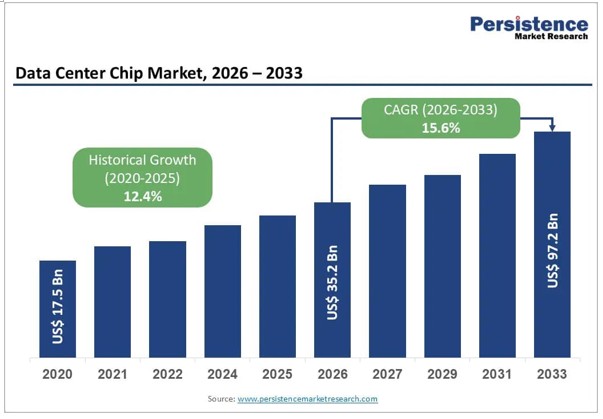

Source: Persistence Market Research

In data terms, ARM's total revenue for FY2026 is close to $5 billion, up over 20% year-over-year, with data center royalty revenue doubling for two consecutive years. Looking at the broader picture, the entire data center chip market is approximately $350 billion in 2026, expected to grow to roughly $970 billion by 2033. ARM's position on this growth curve is distinctive: it doesn't need to bet on which chip ultimately wins — whether it's GPU, CPU, or networking chip, as long as ARM architecture is used, it collects royalties.

One noteworthy detail: ARM currently holds approximately $2 billion in next-generation AGI chip orders, but is constrained by production capacity and can only fulfill about half of them at present. This is a scarcity signal where demand far exceeds supply, meaning ARM's revenue growth hasn't yet fully reflected the scale of existing demand.

ARM's current PE exceeds 400x, with a market cap above $400 billion — buying ARM today essentially means you're already paying for what it will be worth in 2034. Its annual non-GAAP net profit is approximately $1.9 billion, and the only justification the market has for this price is the belief that ARM will maintain high-speed growth for the next 8 to 10 years without a single stumble. This valuation isn't wrong in itself, but it leaves almost no margin for error — any quarter where growth falls below expectations, or any day Apple or Google starts reducing their architectural dependency, and the stock will correct without mercy.

TSMC: The Most Certain Beneficiary That's Being Underestimated

TSMC's stock reaction on the day was muted — but this may be precisely where the market was most shortsighted throughout this entire event.

Jensen Huang flew to Taiwan this time with a core mission beyond the keynote itself: to lock in TSMC's CoWoS advanced packaging capacity. The Vera Rubin platform begins shipping to hyperscale customers like Microsoft, Google, and AWS in H2 of this year, with mass production ramp completing by year-end. Whether that timeline can be met depends entirely on whether TSMC's CoWoS production lines can keep pace.

What is CoWoS? It is a packaging technology that stacks multiple chips tightly together using a silicon interposer — currently the only mature solution for achieving high-density interconnects between HBM high-bandwidth memory and GPU chips. Both Nvidia's Blackwell and the soon-to-ramp Vera Rubin depend on this technology. The problem is, only TSMC can do this in the world, and no one can replicate TSMC's CoWoS lines in the short term.

TSMC is currently executing one of the most aggressive capacity expansions in semiconductor history: CoWoS monthly capacity is planned to expand from approximately 35,000 wafers at the end of 2024 to over 100,000 wafers by the end of 2026. Nvidia is expected to consume approximately 60% of global CoWoS capacity in 2026, totaling roughly 600,000–700,000 wafers, and supply is still running tight.

Key TSMC Data at a Glance

Metric | Figure |

Q1 2026 Revenue | $35.9 billion, up 41% YoY |

Q1 2026 Net Profit Margin | 50.5%, net profit ~$18.2 billion |

CoWoS Monthly Capacity Target (end of 2026) | Over 100,000 wafers |

Nvidia's Estimated 2026 CoWoS Consumption | ~600,000–700,000 wafers, ~60% of global total |

2026 Full-Year Capex Guidance | $52–56 billion (upper end), ~+40% YoY |

2026 Full-Year Revenue Growth Guidance | Over 30% (USD terms) |

Against this backdrop, Nvidia announced approximately $150 billion in annual Taiwan investment — a roughly 10x increase compared to the $10–15 billion range of four or five years ago. A large portion of that money flows to TSMC. TSMC Q1 2026 revenue of $35.9 billion, up 41% YoY, is already a historic high — but the true mass production peak is in H2 of this year through 2027.

Investors often underestimate TSMC's upside by treating it as an already-consensus name. But TSMC's moat isn't just process leadership — its CoWoS packaging capability is a production bottleneck that Nvidia, AMD, and Apple cannot bypass for the next three to five years. The value of that locked-in capacity is very difficult to fully price in short-term stock fluctuations.

Now Let's Talk About Nvidia Itself

CUDA: The Wall You Can't See

Before discussing valuation, there's one thing worth addressing separately, because many people miss it when talking about Nvidia: the CUDA moat.

CUDA is the parallel computing platform Nvidia launched in 2006 — the foundational programming language and tool library that AI researchers and engineers use to write GPU programs. Over nearly 20 years, the global AI developer community has accumulated a massive body of code, models, and engineering expertise on CUDA. Today, over 5 million developers worldwide use CUDA for AI development. All the code these people have written is locked into Nvidia's ecosystem — switching to AMD or another vendor's GPU means the entire codebase needs to be rewritten or re-optimized. At large AI labs, the cost of that migration often runs into hundreds of millions of dollars.

Google and Meta jointly developed the TorchTPU project between 2025 and 2026, specifically to enable PyTorch to run seamlessly on Google's TPUs and thereby break CUDA's lock-in effect. This project is meaningful, but research institutions' assessments conclude that even in the most optimistic scenario, TorchTPU replacing CUDA in production environments would take 12 to 18 months or more. The reason is not only technical, but also ecosystem inertia — 5 million developers don't switch platforms overnight.

With every new chip generation, Nvidia simultaneously updates the accompanying CUDA libraries, operator optimizations, and scheduling tools, bundling hardware advantages with software advantages. This means that even if a competitor's hardware specs catch up on paper, without the accompanying software ecosystem, the performance simply can't be realized in practice. This is the fundamental reason why AMD's MI-series GPUs have long suffered from hardware without ecosystem — and the true underpinning of Nvidia's ability to maintain an 80% share in the AI accelerator market.

This moat is invisible, but harder to replicate than any single piece of hardware.

Physical AI: Jensen's Next Card, Which the Market Hasn't Fully Seen

There is one thread in this keynote that many people glossed over while focusing on RTX Spark and the Vera CPU — Physical AI.

Jensen Huang repeatedly emphasized throughout the speech: AI is evolving from answering questions to executing actions in the real world. This encompasses robots in factories, autonomous vehicles, and every physical device that requires real-time AI perception and decision-making. What Nvidia provides for this market is a three-layer architecture: AI training in data centers (DGX platform), virtual simulation environments (Omniverse + Isaac Sim), and the compute chip in the robot body itself (Thor) — three layers integrated into a complete closed loop.

Source:Quartz

Once robotics companies depend on this system, their migration costs are as high as migrating away from CUDA. Jensen Huang has repeatedly stated that robotics is the next trillion-dollar market opportunity after data centers. The logic behind that qualitative judgment is clear: Nvidia's positioning in the Physical AI market is almost identical to its positioning in the data center market — sell the infrastructure, not the end product, so that regardless of which robotics company ultimately wins, they all have to buy Nvidia's chips.

The AI-driven robotics market was approximately $45 billion in size in 2024, expected to grow to over $100 billion by 2030. This business line isn't yet broken out separately in Nvidia's financials, but it is the third game Jensen Huang is playing. Over the next two to three years, whether Physical AI revenue begins to appear as a separate line item in earnings reports will be a key indicator for judging whether Nvidia's valuation merits further expansion.

Nvidia's Valuation: The Framework Problem

Finally, the hardest question: what is Nvidia itself worth right now?

DBS Bank's target price for Nvidia is $250. Rosenblatt is currently the most aggressive on the sell side, at $325. The consensus target price among 37 Wall Street analysts sits around $298. These numbers aren't the point. What matters is the framework these analysts are using to value Nvidia.

Traditional semiconductor company valuation uses a cyclical logic: revenue fluctuates with AI capex cycles, with a 25–30x PE multiple. But what Nvidia is doing now has gone beyond selling chips. It has the CUDA ecosystem — a programming environment used by 5 million AI developers worldwide, with extremely high switching costs; it has AI software platforms like NIM and NeMo; it has Physical AI (robotics/autonomous driving) buildout; and now it has added PC chips and data center CPUs. Jensen Huang's words in the speech are worth repeating: "Nvidia is becoming the builder of AI factories" — meaning, we don't just sell equipment, we help customers build complete AI production infrastructure.

If that narrative holds, Nvidia's valuation framework should look more like a platform company such as Microsoft or Apple, earning not just hardware profits but a toll on the entire ecosystem. Platform companies typically support 35–45x PE or higher. Nvidia's own figure is that the cumulative demand visibility for the Blackwell and Rubin platforms already exceeds $1 trillion — even if that's an optimistic estimate of real demand, the number implies Nvidia's revenue ceiling in the coming years is higher than what any model currently being built can capture.

But there is one problem that needs to be honestly acknowledged: RTX Spark and the Vera CPU are products launching this fall, with real volume production not until 2027. What Jensen Huang's speech announced is a direction — not a realized financial figure. Investors buying Nvidia today are essentially prepaying a premium for the judgment that "Nvidia will become a platform company in the AI era." That judgment may well be correct, but the time at which it gets validated is 2027–2028, not tomorrow.

Tallying It Up: Whose Logic Changed, and Whose Didn't

Summing up all of the above analysis, we can walk through the situation for each major name after this keynote.

TSMC's logic is the most certain. CoWoS capacity is the bottleneck for the entire industry, Nvidia has locked in the largest share, the mass production peak hits in H2 of this year, and TSMC's revenue growth has a clear and concrete path to realization. The stock didn't react much in the short term, but that doesn't mean the fundamentals didn't change.

ARM's logic is the most flexible. The royalty model makes it a natural beneficiary of the entire ARM ecosystem's expansion — Nvidia, Apple, Amazon, and Google are all paying it. Data center royalty revenue has doubled for two consecutive years, FY2026 revenue is close to $5 billion, and growth of 20%+ annually is expected to continue for the next three years. The only thing to watch is its already-elevated valuation — the market has little tolerance for disappointment.

Qualcomm's logic is largely unchanged. The PC market share threat is real, but it's not the core variable in Qualcomm's valuation. The smartphone and automotive businesses are intact, the data center custom chip business just landed a new customer, and the recent decline looks more like an emotional reaction.

Intel's logic has been substantively challenged. Double-sided pressure in the data center CPU market, a new competitor in the PC market, and ongoing 18A yield issues — this is a name that requires serious re-evaluation.

AMD is in a wait-and-see zone. Vera CPU's short-term impact on AMD is limited, EPYC share is still at historic highs, but the competitive landscape after 2027 needs continued monitoring.

Nvidia itself is the biggest winner of this keynote — but also the hardest one to judge. The direction is right, the CUDA moat is real, Physical AI is a third growth curve taking shape, but the valuation logic of upgrading from chip company to platform company won't be numerically validated until RTX Spark and the Vera CPU are actually shipping at scale.

Post-Keynote Logic Change Summary

Name | Logic Change | Current Market Pricing | Key Observation Milestone |

TSMC | CoWoS capacity locked in, mass production peak H2 this year | Underpriced in short term | Q3–Q4 2026 earnings |

ARM Holdings | Royalties cover full ARM ecosystem, data center share rising | Expensive, but growth logic clear | Quarterly royalty revenue growth rate |

Nvidia | Upgrading from chip company to AI platform company, time verification ongoing | Partially priced in; upside depends on CPU/PC execution | 2027 full-scale Vera production data |

Qualcomm | PC share base is small, smartphone/automotive moats intact | Short-term overreaction | Next quarter earnings confirming smartphone/auto revenue |

AMD | EPYC at historic highs, short-term Vera CPU impact limited | Fairly priced, no clear catalyst | Re-evaluate after Vera CPU lands in 2027 |

Intel | Data center + PC double pressure, 18A still unproven | Long-term risks may not be fully priced | 18A yield and external customer progress |

Those two hours of Jensen Huang's speech weren't about Nvidia's story for the next quarter — they were about its ambitions for the next five years. The market's reaction on June 1st was the first pricing of that ambition, but it is absolutely not the last. The truly interesting things will happen one by one over the next four to six quarters: RTX Spark's launch, Vera Rubin's production ramp, Vera CPU landing its first meaningful batch of orders — or any one of those going sideways.

That is the main thread worth following continuously from here.

Disclaimer: This article is based on publicly available information, all data cited with sources, provided for reference only and does not constitute investment advice. Markets carry risks; any names mentioned in this article do not represent a buy or sell recommendation.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.