Adobe Earnings Beat Expectations, Why Did the Stock Price Still Fall?

AI Podcast

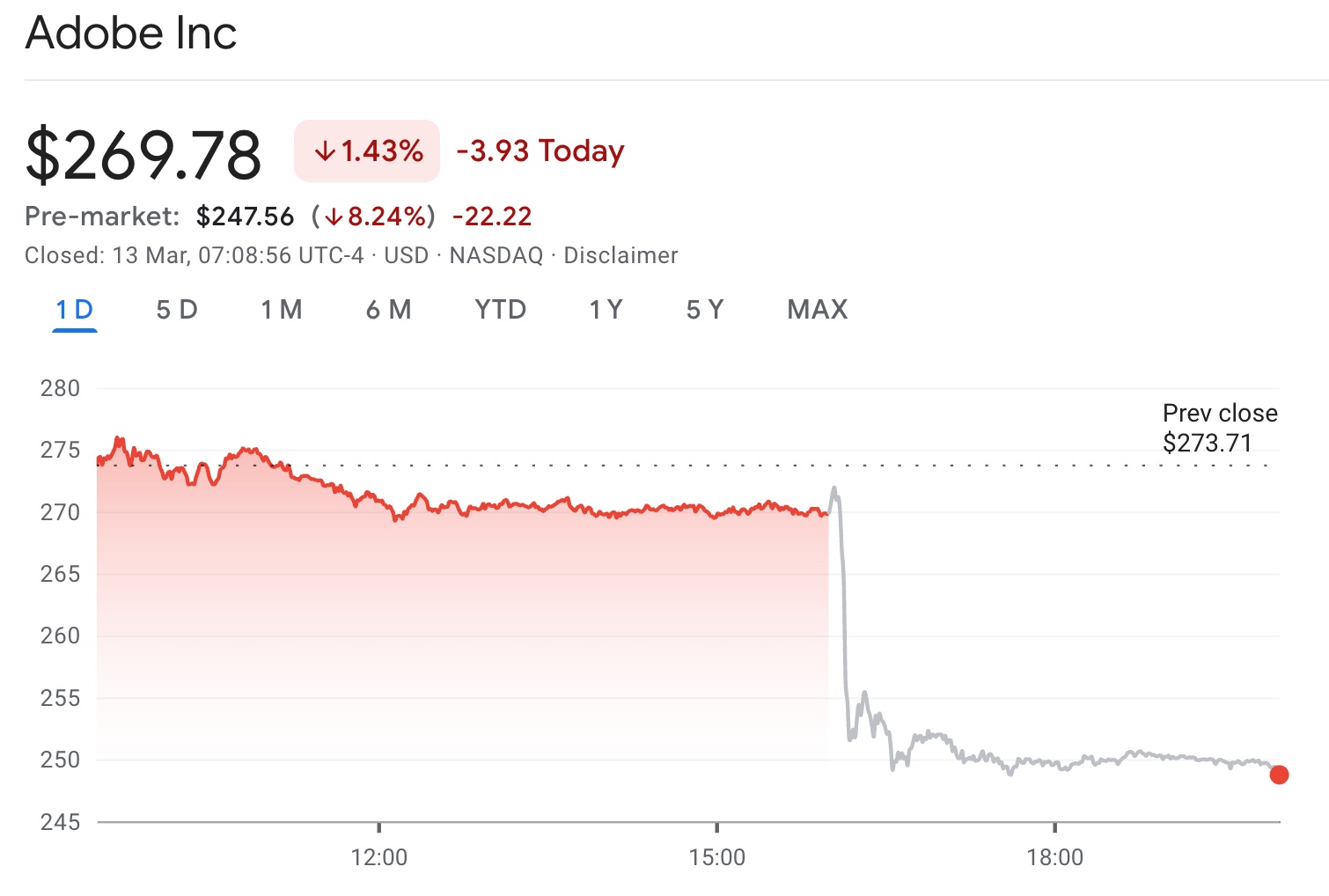

Adobe's stock fell nearly 8% pre-market despite exceeding Q1 2026 earnings and revenue expectations. Investors are concerned about slowing Annual Recurring Revenue (ARR) growth to 10.9% and competitive pressure from AI-native design tools. Questions remain on Adobe's ability to monetize AI products effectively and maintain its market leadership under new management, impacting its valuation and the broader software industry's reassessment of long-term moats.

TradingKey - Before the U.S. market open on March 13, Eastern Time, Adobe (ADBE.US) fell nearly 8% in pre-market trading. After Adobe released its latest quarterly earnings report following the previous trading session, its share price declined significantly in after-hours trading.

Despite delivering a quarterly report card that exceeded Wall Street expectations, the phenomenon of "beating earnings but falling stock price" reflects investors' multiple concerns regarding Adobe's future growth prospects.

Strong earnings performance, but market reaction was tepid

From a financial data perspective, Adobe's latest quarterly results were not lackluster. Revenue for the first quarter of fiscal 2026 reached approximately $6.4 billion, up about 12% year-over-year and exceeding market expectations; adjusted earnings per share were approximately $6.06, also surpassing the $5.87 previously estimated by analysts.

In terms of business structure, Adobe's core business continues to maintain steady growth. Among these, Document Cloud revenue grew by approximately 16% year-over-year, indicating that demand for enterprise document management and digital office solutions remains strong. At the same time, subscription revenue from the company's AI-related products also saw rapid growth, with "AI-first" Annual Recurring Revenue (ARR) achieving a significant increase.

The fact that Adobe's stock price still experienced a notable correction after the earnings release suggests that investors' focus has shifted from "current performance" to "future growth."

Annual Recurring Revenue (ARR), a metric closely watched by investors, has reached approximately $26 billion, but the growth rate slowed to 10.9% from the previous 11.5%.

For SaaS software companies, the ARR growth rate is often regarded as a core indicator of future revenue sustainability. When this metric shows signs of slowing, the market often worries whether the company's growth cycle has reached a plateau.

Especially in the context of rapid AI technological development, investors are more focused on whether software companies can leverage AI to achieve new growth curves. If ARR fails to re-accelerate, Adobe's valuation premium may be further challenged.

Another significant factor weighing on Adobe's stock price is the industry competition brought about by generative AI. In recent years, a group of AI-native creative tools has emerged rapidly, such as the design platform Figma and the online design tool Canva, which are exerting new competitive pressure on the traditional design software market.

These new platforms typically adopt lighter product structures and use AI to automatically generate design content, lowering the barrier to entry for users. This has led some small and medium-sized enterprises and individual creators to begin experimenting with alternatives to traditional design software.

For Adobe, although the company has launched the AI tool Firefly and integrated it into the Creative Cloud ecosystem, the market remains focused on a core question: can AI products truly be converted into new profit growth points? Currently, AI features are viewed more as added value for products rather than independent revenue sources. If AI technology lowers the professional barrier to creative software in the future, Adobe's long-established moat may face certain challenges.

In addition to industry competition, management changes have also brought new uncertainties to investors. Adobe announced that current CEO Shantanu Narayen will step down after a successor is found, news that has likewise impacted market sentiment.

The overall valuation of the software industry is undergoing a reassessment

From a more macro perspective, the decline in Adobe's stock price is also related to valuation adjustments across the entire software industry. Recently, the emergence of generative AI has changed the competitive landscape of the software sector, leading some investors to begin re-evaluating the long-term moats of traditional SaaS companies.

Over the past few years, software companies have generally relied on the stable cash flows provided by subscription models to achieve high valuations. However, as AI tools lower the barriers for software development and design, some market viewpoints suggest that entry barriers for the software industry may be declining. In this context, even if Adobe maintains steady growth, investors may demand higher growth rates to support current valuations.

In the short term, Adobe still possesses a powerful product ecosystem, including core creative software such as Photoshop, Illustrator, and Premiere Pro, maintaining its solid position in the professional design field.

In the long run, however, investors will focus more on two key variables: first, the commercialization capabilities of the company's AI products, and second, whether the new management can continue to maintain Adobe's industry leadership in the AI era. Against the background of rapidly evolving AI technology, Adobe's future development path will not only determine the company's own valuation but may also become an important bellwether for the transformation of the entire software industry.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.