AMD Beats Q1 2026 With $5.8B Data Center Revenue and Guides $11.2B for Q2; Is AMD a Buy at $415?

AI Podcast

Advanced Micro Devices (AMD) reported Q1 2026 revenue of $10.3 billion, up 38% year-over-year, with EPS at $1.37. The Data Center segment drove this growth, generating $5.8 billion (+57% YoY), fueled by EPYC CPUs and Instinct GPUs. Non-GAAP gross margin reached 55%, reflecting a shift to AI solutions. Q2 revenue guidance is $11.2 billion. A technical pullback to $395-$408 is identified as a trade entry, with targets at $426 and $474. A daily close below $395 would negate the bullish outlook.

TradingKey - Meta: AMD beat Q1 2026 with $10.3B revenue (+38% YoY) and $1.37 EPS. Data Center hit $5.8B (+57%). Q2 guided $11.2B. Pullback to $395–$408 is the trade entry. Targets $426 then $474.

Advanced Micro Devices (AMD) dropped their Q1 2026 earnings on May 5th, truly blowing expectations out of the water. Every key metric that got reported in after hours trading sent the stock price rocketing upwards. Their revenue came in at a staggering $10.3 billion - a 38% year-over-year jump that utterly annihilated analysts consensus estimates. On a non-GAAP basis, EPS arrived at $1.37 - which is $0.09 better than forecast and has gone up a whopping 43% - making Q1 of 2026 one of the best for AMD in recent memory. The main reason for this huge success was the data center segment, which raked in an impressive $5.8 billion. That's a 57% increase over last year, and its thanks largely to a huge uptake in EPYC server CPUs by the big tech players and Instinct GPUs for AI training & work - they really are the driving forces behind this massive growth.

This sent non-GAAP gross margin soaring to a whoppng 55% - the direct result of the business (AMD) shifting over towards a lot more profitable AI solutions and away from the more up-and-down consumer space.

Q1 2026 Results - $5.8b Data Center Fragment Is Where Its At

You can't exactly say AMDs Q1 beat was universal - it was a bit more patchy than that. The data centre segment is where things really got exciting though , with a 57 % year on year jump to a whacking $5.8 billion. And that has everything to do with AMD still being the undisputed champ in the server CPU space - especially with the hyperscalers. and we also have to mention the growing demand from these same players for AMDs Instinct GPUs for learning and inference. This has meant that the data centre segment is now pretty much carrying the whole show - and pushing the company towards higher profit margins. Non GAAP gross margin leapt all the way up to a mind-boggling 55 % - a clear sign that the business is shifting out of consumer spaces and into the much more lucrative AI space - with client and gaming sector both contributing positively and embedded sector even creeping back into growth.

At the earnings call, AMD CEO Lisa Su said that demand for its AI bits and bobs was "sky high" - and we can take that as read that the Q2 guidance of $11.2 billion is just backing that up even further. This is a sequential growth of around $900 million from Q1 - it's a good deal more than what the market was expecting and it sent shares into a bit of a tailspin. The MI300 series has really taken off with the major cloud players and it's clear that the upcoming MI400-series accelerators and rack-scale platforms are well positioned to grab the next wave of hyperscaler AI infrastructure spending.

Wall Street is still pretty much all in on AMD - with the majority of analysts giving AMD a Buy or Outperform rating and price targets ranging from $220 right on up to over $300 - most of which are actually now below the current price following the immediate aftermath of the earnings call, with loads of people expecting further upgrades to come in.

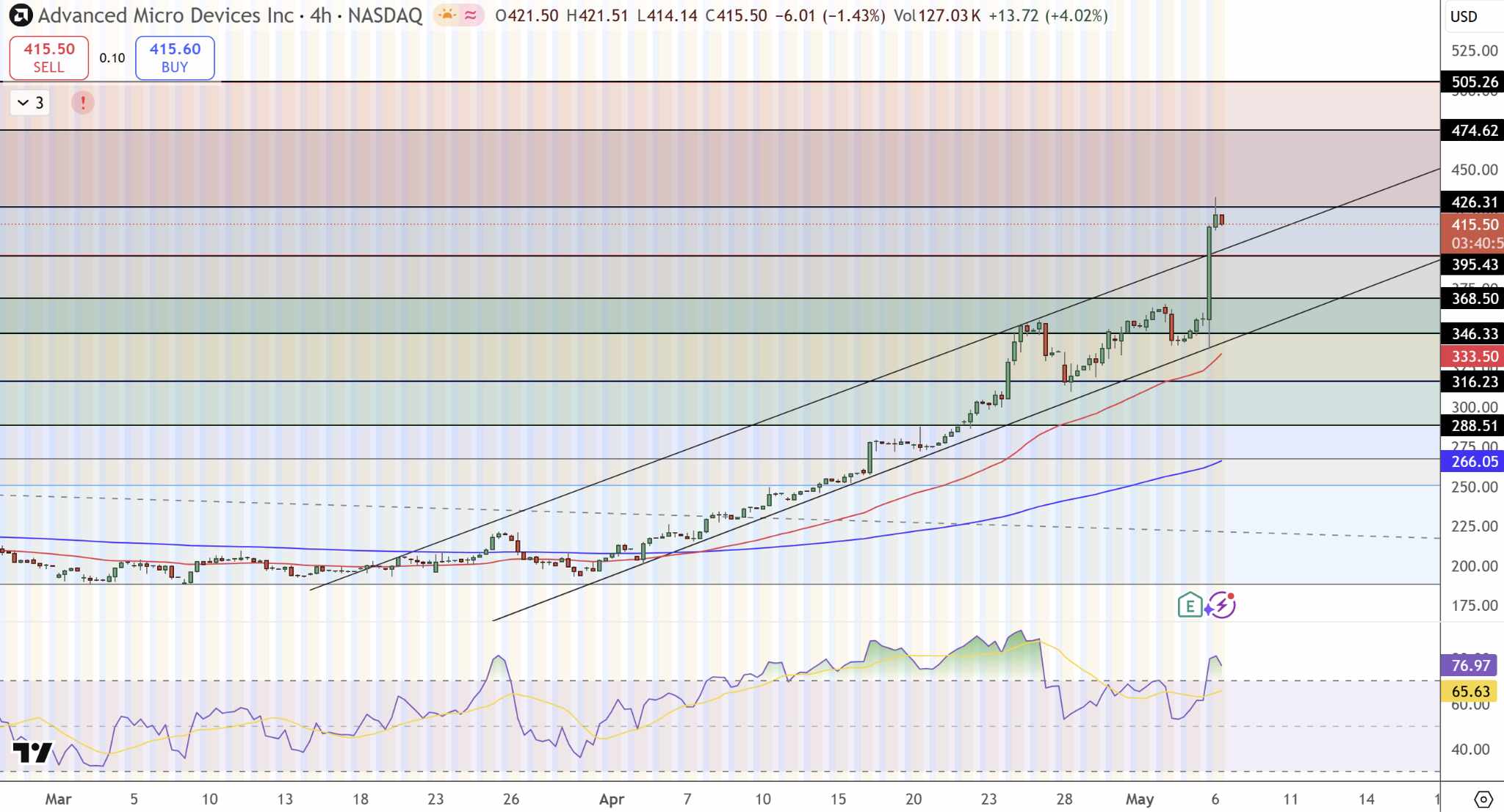

AMD Technical Analysis — Pullback to $395–$408 Is the Entry, Not the Exit

Cruising over the 4 hour chart for AMD, we see the stock hitting up against the upper edge of a pretty steep channel up around $426. It put up a 'shooting star' rejection candle, which is generally a sign that buyers are struggling at the resistance point, rather than necessarily a sign the trend is about to reverse.

We are now at $415.50, pulling back toward the lower end of the 2.0 to 2.272 Fibonacci cluster at $395 - $408, and the midline of the channel supported by the red moving average near $395 to $403.

Source: NASDAQ Tradingview

There's a slight cooling in the oscillator from 76.97 to 65.63 with a mild negative divergence on the 4 H highs, however it is still holding above 50 - and the trend of higher lows remains unbroken. There is secondary trendline support from early April near $368, currently untouched. No breakdown - no reversal signal - we are looking at a pull back in a confirmed uptrend from the March base.

Trade Setup

- Entry point: Looking for a bounce back up to the $408–$395 area - that's where you're likely to find some support around the 2.0-2.272 Fib level and the channel midline.

- First target : $426.31 - that's where the upper channel resistance kicks in, and also where the rejection candle was formed a few days back.

- Second target : $474.62 - that's the next big Fibonacci extension level above the channel, and a long way up.

- The stop loss point : daily close below $395 - if the channel support breaks, it's time to get out.

How Did AMD Perform in Q1 2026?AMD managed to blow past expectations, and its revenue shot up by a very respectable 38% to a whopping $10.3 billion. The non GAAP earnings per share came in at a pretty healthy $1.37 & Data centre revenue also took a 57% leap to $5.8 billion, heavily driven by the sheer demand for their EPYC CPUs and Instinct GPUs. Gross margins also moved up to a nifty 55%.

What is AMD’s Q2 2026 Guidance?Now AMD is looking ahead to Q2 and are predicting a revenue of around $11.2 billion, a $300 million buffer so nothing too specific there. They're looking pretty optimistic though, considering the next few months. They're banking on continued AI demand - still going strong - plus the growth they've been seeing in the MI300 and a bit of a contribution from the MI400 accelerators that are still to come.

Is AMD Stock a Buy After Earnings?Fundamentally, AMD's looking pretty healthy after this one but we're still holding out for a pullback entry around $395 to $408 before calling it a buy. If you can hold that zone you're looking at $426 & $474 in play. A daily close below $395 though and the whole bullish channel gets called into question & you know what that means - caution.

The Bottom Line

Now let's get past all the numbers and take a look at the bigger picture. AMD's Q1 2026 results were seriously impressive - they smashed it. Their Data Centre business came in at $5.8 billion, which is a pretty clear sign that those EPYC and Instinct chips of theirs are really gaining traction & the growth is only going to get more intense. And with that 55% non-GAAP gross margin - that's a really encouraging sign, it shows the business is shifting in the right direction. And then there's that $11.2 billion Q2 guidance - thats a pretty high bar for the MI400 to clear.

Right now the stock is sitting at $415, a 1.4% pullback from its high after it got rejected from near the channel resistance of $426. As for a sensible trade, $395 to $408 is the sweet spot - there's defined risk, the uptrend remains intact, and we've got plenty of catalysts coming down the line including MI400 deliveries & a slew of promising hyperscaler design wins forecasted for the rest of the year.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.