Nvidia Q3 Earnings Preview: Can Blackwell's Ramp-Up Break the Slowdown and Save the U.S. Stocks?

TradingKey - NVIDIA (NVDA) is set to report its Q3 FY2026 earnings after market close on Wednesday, November 19, positioning itself as a key market focus amid a broader U.S. stock market pullback fueled by AI bubble concerns and liquidity pressures.

Analysts widely anticipate NVIDIA will deliver its strongest quarterly growth in several periods, driven by an accelerated ramp-up in its Blackwell cabinet production. This could potentially reverse the "growth deceleration narrative" and ease fears of an AI bubble.

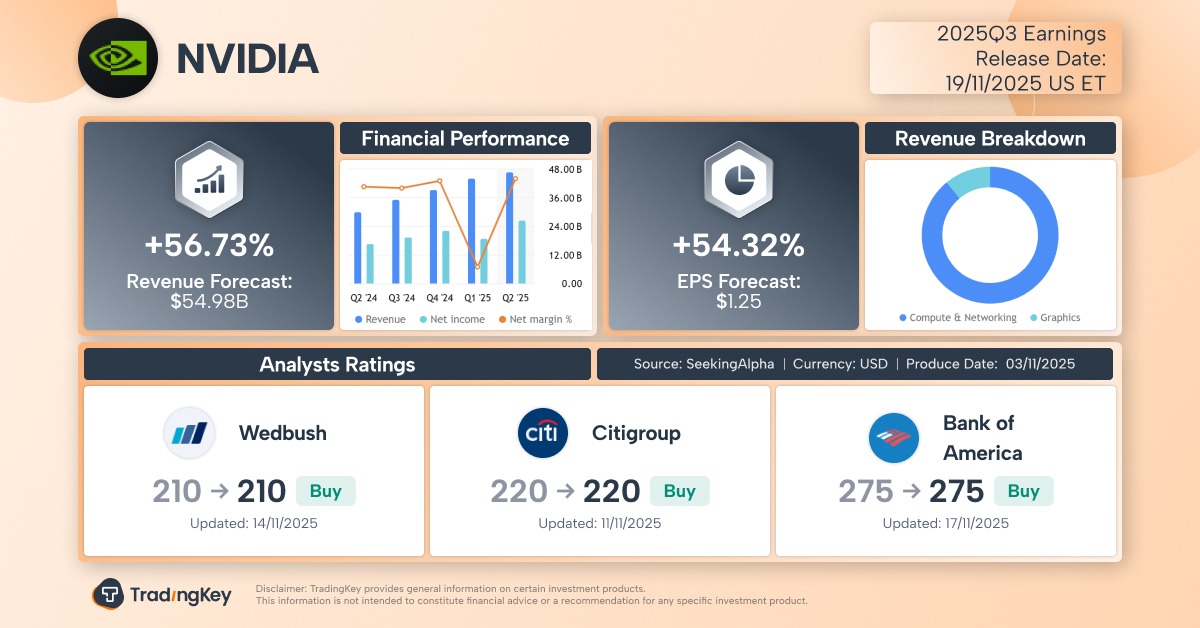

According to Seeking Alpha, analysts project NVIDIA's Q3 FY22026 (roughly equivalent to calendar Q3 2025), ending October, to report a 56.73% year-over-year revenue increase to $54.98 billion. Additionally, earnings per share (EPS) are expected to grow 54.32% year-over-year to $1.25.

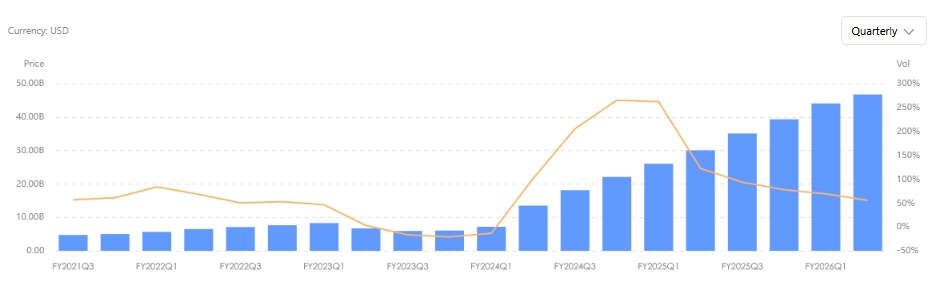

Based on these consensus financial forecasts, NVIDIA's revenue growth is anticipated to move past the Q2 low of 55.60% and return to a faster growth trajectory. NVIDIA's growth has decelerated for six consecutive quarters since peaking at 265.28% in Q4 2023. This trend has fueled concerns that the explosive growth in AI demand, spearheaded by NVIDIA's chips, might be topping out.

NVIDIA Historical Revenue, Source: TradingKey

Several factors are currently contributing to investor sentiment shifting from euphoria to caution, and even pessimism, regarding the AI boom. These include signs of weakness revealed in Q3 earnings from AI cloud infrastructure companies like CoreWeave, the unprecedented reliance of companies such as Meta and Oracle on corporate bond issuance, and warnings from Wall Street institutions like Morgan Stanley about tech stock valuations reaching historical highs.

With the S&P 500 index retreating over 3% from its October record high, capital markets are pinning their hopes for a market rebound on NVIDIA's Q3 earnings report.

Investors will scrutinize NVIDIA's earnings for insights into whether the AI chip leader has overcome Blackwell GPU supply bottlenecks. Furthermore, they will assess management's outlook on AI demand, the positivity of Q4 financial guidance, progress in China market chip sales, and the effectiveness of its diversified businesses.

Significant Blackwell Production Breakthrough

NVIDIA's management has consistently emphasized strong customer demand in recent quarters, stating that Blackwell architecture chips, despite full-throttle production expansion, remain in short supply. From this perspective, supply chain factors partly explain NVIDIA's sequential revenue growth deceleration, rather than a deterioration in demand.

NVIDIA CEO Jensen Huang stated earlier in November that demand for the most advanced Blackwell chips is exceptionally robust. NVIDIA not only manufactures GPUs but also CPUs, networking components, and switches, meaning numerous chips are tied to the Blackwell ecosystem.

Morgan Stanley's industry chain surveys indicate a significant upward inflection point in industry sentiment since October. Blackwell cabinets have fully entered an accelerated ramp-up phase, leading the firm to project Q3 as NVIDIA's strongest quarter in recent memory.

Morgan Stanley noted that NVIDIA has fully resolved earlier rack-related issues. While demand is rapidly increasing, bottlenecks are now predominantly in ancillary areas such as storage, servers, power, and space, rather than limiting GPU shipments.

On the customer side, NVIDIA's major clients have collectively raised their Q3 cloud service capital expenditure forecasts by $142 billion, with four large-scale cloud service providers each increasing their spending by at least $20 billion.

Although a portion of these tech giants' substantial capital expenditures may flow to competitors like AMD and Google's in-house TPUs, NVIDIA, holding the vast majority of market share, remains the primary beneficiary.

Buy-side analyst Michael Del Monte also observed that data center GPUs typically have a useful life of 1-3 years. Hyperscale cloud service providers might initiate the refresh cycle for their first-generation AI infrastructure next year. Microsoft management has previously hinted at an upcoming replacement demand for aging CPU equipment.

This implies that cloud service providers will need to allocate not only growth capital but also maintenance capital for AI infrastructure, creating a cumulative capital expenditure effect over several years. Consequently, this reinforces a positive outlook for NVIDIA's sales.

From the supplier perspective, ODM manufacturers such as Quanta, Wistron, and Foxconn have indicated strong growth expectations, ranging from high double-digit increases to doubling within a few months. This rapid production expansion by these supply chain giants significantly boosts NVIDIA's order visibility.

JPMorgan also reported that NVIDIA's supply chain partners have demonstrated robust execution in increasing Blackwell series rack shipments over the past three to four months. The firm projects Q3 production to rise 50% quarter-over-quarter to 10,000 units, with a similar growth rate expected for Q4.

Morgan Stanley has raised its revenue forecasts for NVIDIA's October and January quarters to $55 billion and $63.1 billion, respectively. The firm anticipates quarterly sequential growth of $8 billion for both October and January, which would mark an industry record.

JPMorgan believes there is further upside potential for NVIDIA's revenue. They expect Q3 revenue to surpass the consensus estimate of $55 billion, and Q4 revenue to reach $63 billion to $64 billion, exceeding market expectations of $61.5 billion.

China Market Recovery Potential and Diversified Strength

The absence of an estimated contribution from the China market in NVIDIA's previous earnings guidance of $54 billion in Q3 revenue was a "disappointment point" in the Q2 report. This suggested that NVIDIA's management held little hope for a short-term resumption of chip exports to China.

Following a noticeable easing in US-China economic and trade relations, spurred by a rare meeting between the leaders of the two nations, markets are hopeful that the Trump administration will expedite the relaxation of export restrictions on NVIDIA products.

Jensen Huang anticipates that the Chinese market could present a $50 billion business opportunity for NVIDIA this year. When asked if he was willing to sell advanced Blackwell chips to China, he expressed a desire to do so but noted it was a decision only the Trump administration could make.

The data center business, accounting for 88% of NVIDIA's revenue, is undeniably its pillar. However, it's also important to note that other segments achieved robust double-digit growth in Q2, underscoring NVIDIA's diversified revenue generation capabilities.

NVIDIA's Gaming segment revenue grew 49% year-over-year in Q2, while its Professional Visualization segment increased 32%, and the Automotive and Robotics segment saw a 69% rise.

Can NVIDIA's Earnings Rescue US Stocks?

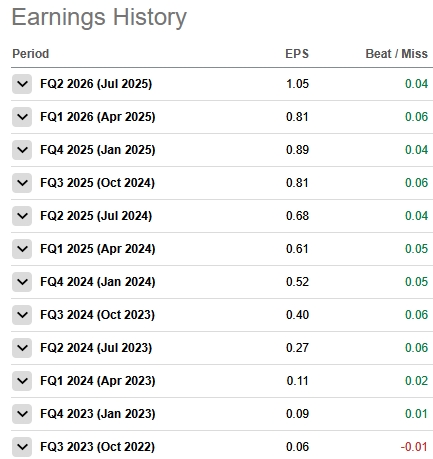

To date, NVIDIA has surpassed Wall Street analysts' EPS estimates for 11 consecutive fiscal quarters. Furthermore, despite its revenue growth rates fluctuating from a low of 21% to a high of 265% in the past, NVIDIA's revenue growth has exceeded market expectations for at least 20 consecutive fiscal quarters.

NVIDIA Historical EPS, Source: Seeking Alpha

While NVIDIA's financial strength is undeniable, investors tend to be discerning. NVIDIA's stock has not risen after its earnings announcements, having fallen following its last three quarterly reports.

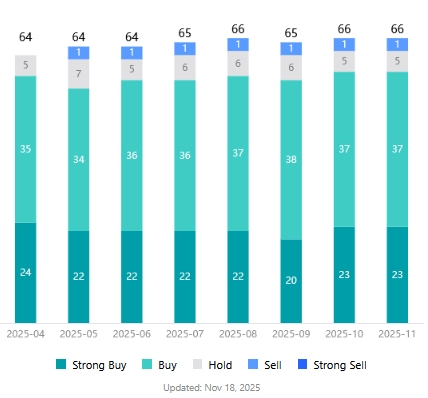

TradingKey's stock scoring tool indicates an average analyst price target of $234.404 for NVIDIA shares, implying approximately 26% upside from its latest price. Among the 66 analysts covering NVIDIA's stock, only one issued a 'Sell' rating, while 60 analysts have 'Buy' ratings.

NVIDIA Stock Analyst Ratings, Source: TradingKey

Gene Munster, an analyst at Deepwater Asset Management, highlighted NVIDIA's dilemma: overly strong results could intensify concerns about AI over-investment, while moderate growth might be interpreted as a return to normalized expansion. Consequently, investors "trading the NVIDIA earnings" face significant volatility risks.

If NVIDIA's earnings once again shine, and Jensen Huang offers a more optimistic outlook on supply-demand balance, could NVIDIA serve as the "brake pad" to halt the US stock market's decline?

Wedbush analyst Daniel Ives stated that Wall Street will closely monitor NVIDIA's results, guidance, and commentary to assess the health of the broader AI megatrend.

NVIDIA is the cornerstone of this AI revolution. Given the abundance of positive information from the Asian supply chain, coupled with the substantial capital expenditure figures reported by hyperscale tech companies at the end of October, Ives anticipates NVIDIA's performance will significantly surpass Wall Street expectations.

Goldman Sachs, Citi, and Morgan Stanley, who recently raised NVIDIA's price targets, are also clearly bullish. Institutions like Citi and UBS indicate that operational milestones, including significant Blackwell GPU shipments, are key drivers supporting their bullish stance on NVIDIA shares.

However, Mizuho analyst Jordan Klein cautioned that companies, stocks, and expectations are now being so excessively analyzed that it's challenging for any company to immediately spark a buying frenzy post-earnings.

Klein pointed out that investors are on edge, highly alert to AI capital expenditures having reached excessive levels that cannot be financed through existing credit markets.

Under these circumstances, Klein believes NVIDIA's short-term stock outlook is unfavorable. Nevertheless, he left room for upside: if NVIDIA provides Q4 revenue guidance of $65 billion, exceeding market expectations of $62 billion, the stock could still see an increase.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.