Four Key Disappointments in Nvidia’s Q2 FY2026 Earnings That Investors Can’t Ignore

TradingKey - AI chip leader Nvidia (NVDA) delivered revenue and profit growth above expectations in its second fiscal quarter ended July, with over 50% year-on-year growth, showcasing its strong momentum and leadership in artificial intelligence. However, capital markets viewed the report as “not dazzling,” citing concerns over China market uncertainty, slowing growth momentum, and customer concentration.

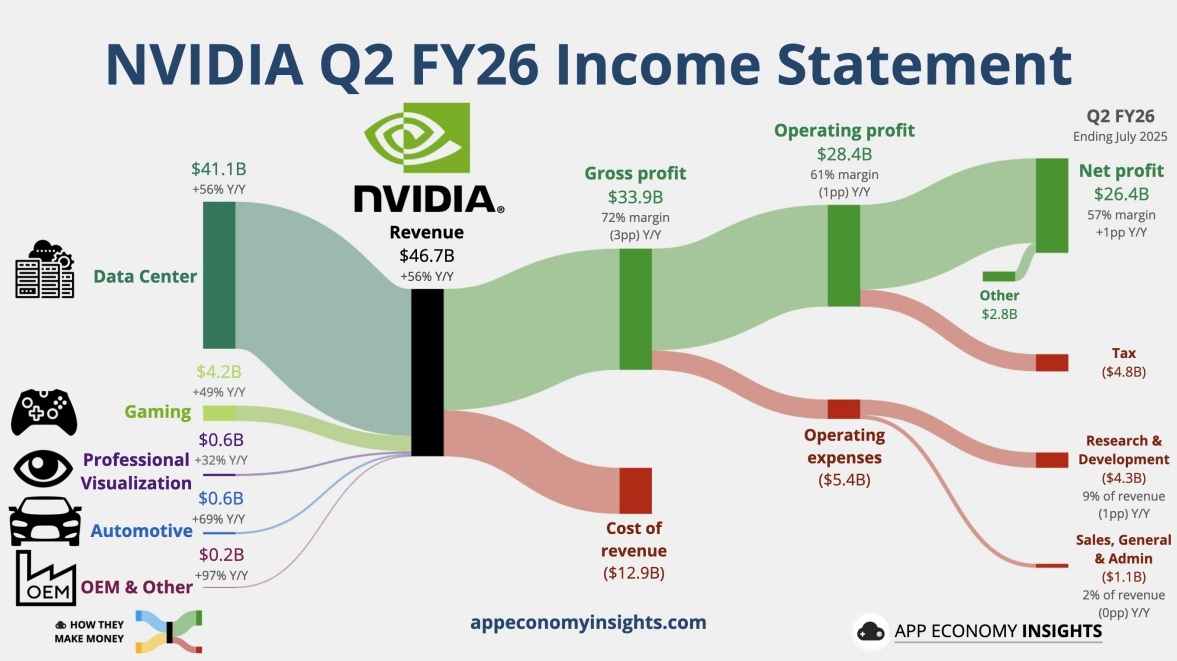

In the second fiscal quarter, Nvidia reported:

- Revenue: $46.743 billion, up 56% YoY, exceeding the $46.23 billion consensus and the high end of its guidance ($45.9 billion)

- EPS: $1.05, up 54% YoY (or $1.04 excluding H20-related impacts), above the $1.01 consensus

After the results were released on Wednesday, August 27, Nvidia’s stock fell around 5% in after-hours trading, though the decline later narrowed. Analysts from Goldman Sachs and other firms said the overall results were solid and slightly above expectations, but investors were hoping for even stronger growth — making the report “not flashy enough.”

1. China Market Supply Risk: The Absence of H20 Revenue

Although the U.S. government approved the resumption of exports for Nvidia’s China-specific H20 chip, the 15% revenue share demanded by the U.S. and potential order cuts from Chinese clients due to the “backdoor security” remain major obstacles to Nvidia’s expansion in this critical market.

Nvidia’s largest revenue segment — data center — grew 56% YoY to $41.1 billion, but missed the $41.29 billion consensus, marking the second consecutive quarter of falling short of Wall Street expectations.

This was partly due to no H20 shipments to China in Q2, as the lifting of export restrictions had not yet translated into revenue recovery. Nvidia CFO Colette Kress noted that data center compute revenue grew 50% YoY to $33.8 billion, while the $4 billion decline in H20 sales led to a 1% sequential drop.

Not only did Nvidia lose out on this lucrative revenue stream in Q2, but it also remained cautious about future China supply — its Q3 revenue guidance does not include any H20 exports to China.

Deepwater Asset Management said this was “shocking,” as Wall Street analysts had expected a $2 billion revenue guidance bump in Q3 following the lifting of export restrictions.

Bloomberg noted that this is disappointing for those who assumed the “floodgates” would open immediately after U.S. licensing approval. But in the long run, it may help investors set lower expectations.

Kress reassured investors that Nvidia is waiting for the U.S. government to issue a formal regulation to resume exports, and expects to ship $2–5 billion worth of H20 chips to China in Q3. Additionally, the U.S. government’s plan to take 15% of China revenue has not yet been codified, leaving room for Nvidia to potentially sell in China without paying the “commission.”

2. Growth Slowdown: A New Reality

Nvidia’s overall quarterly revenue growth has slowed from 69% in Q1 to 56% — the lowest in over two years, far from the triple-digit growth seen last year. Data center revenue growth slowed from 73% in Q1 to 56%.

The company’s Q3 revenue guidance of $54 billion is in line with expectations, though some analysts had forecast as high as $60 billion.

Nvidia CEO Jensen Huang projected that core customers may spend $3–4 trillion on AI infrastructure over the next five years — a massive opportunity for Nvidia.

However, eMarketer analysts warned that if near-term returns on AI applications remain hard to quantify, large data center operators may tighten spending at the margin.

Reuters commentator Jonathan Guilford noted that Nvidia and AI are almost synonymous — when a tech giant invests in AI, it’s effectively investing in Nvidia. But U.S.-China relations could threaten this logic.

Guilford added that a growing body of research is now focused on developing alternative chips and software, even though Huawei and others are not yet at the same level. AI remains a major investment, but breakthroughs may emerge elsewhere — and the cost of losing Nvidia’s dominance is hard to calculate.

Goldman Sachs highlighted four key risks:

- Potential slowdown in AI infrastructure spending

- Market share erosion from competitors like AMD

- Intense competition threatening high margins

- Supply chain bottlenecks limiting revenue growth

3. Market Expectations Were Too High

Among AI players, few can match Nvidia’s ability to sustain over 50% growth after years of triple-digit expansion. Yet the market remains demanding of this leader.

Running Point Capital’s CIO said Nvidia’s growth curve is still impressive, but no longer exponential.

“I think people might have been looking for a little bit more on that side,” said a Horizon Investment Services analyst. “I'm not surprised that the stock in the after-market is down a bit, but it is not down a ton, especially given the strength that the stock is showing so far this year.”

Blue Chip Daily Trend Report strategists expect Nvidia to face some near-term downside testing, as results didn’t significantly exceed forecasts. But beyond short-term volatility, Nvidia remains the benchmark AI stock — the most direct way to invest in AI.

4. Customer Concentration Risk

CFO Kress noted that large cloud service providers drove Blackwell revenue growth in the data center segment, with top customers accounting for 50% of that revenue.

Bloomberg reported that while this was the case three months ago, investors are hoping to see this trend decline — signaling that AI computing is spreading across the broader economy, rather than being concentrated in a few tech giants.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.