Investing in Digital Payments & Blockchain

- Payments are shifting from cash to cards/mobile wallets and blockchain rails, reshaping how money moves and how businesses monetize.

- Digital networks cut fees and delays, enable global and cross-border commerce, and drive financial inclusion in emerging markets.

- Blockchain introduces stablecoins, programmable money, and CBDC experiments, expanding functionality while also introducing regulatory and volatility risks.

- Investors can play incumbents (Visa/Mastercard), fintechs (PayPal/Block/Adyen), back-end rails and cloud, and selective crypto/ETFs, best via a balanced, long-term allocation.

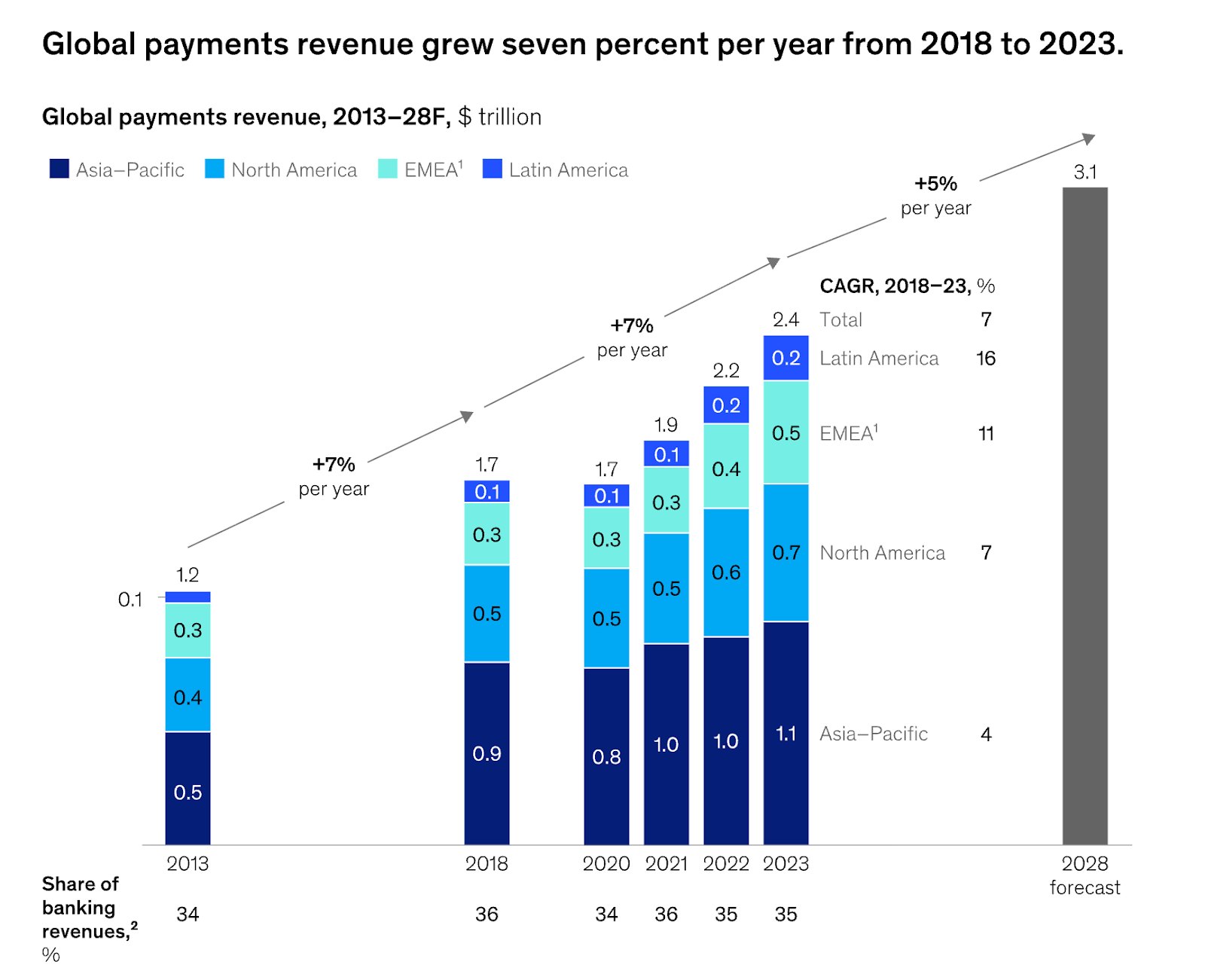

The Cashless Revolution

TradingKey - The global payments system is undergoing one of the most profound restructuring episodes in its history. Cash is being rapidly replaced by digital substitutes, ranging from contactless cards and wallets on mobile devices to blockchain-based networks. What’s at play here is more than convenience, a fundamental shift in how payments flow, how business model payments are made from transactions, and how payment recipients engage with payment systems. For investors, digital payments and blockchain represent a structural growth narrative with roots deep in both technology and finance.

Accelerated pandemic trends were already underway. Online commerce exploded, mobile payments became mainstream, and digital wallets such as PayPal, Apple Pay, and Alipay became widely used tools. Meanwhile, built-on-blockchain payment systems were coming of age, with stablecoins and border settlement solutions pushing against established rails. Complementing fintech with blockchain presents a vast horizon of opportunities for long-term investors.

Source: https://www.mckinsey.com

Why Payments Matter Digitally

Digital payments are a solution to inefficiency at their very core. Old-game banking systems are sluggish, costly, and geographically constrained. Credit card networks are costly, with high interchange fees. Cross-border payments may remain stuck for days. But digital payment networks are fast, scalable, and cost-effective. They enable merchants to go global, consumers to buy and sell with seamless ease, and businesses to build out business models that include subscription and micro-payments.

For emerging economies, the impact is more profound. Mobile payments have leapfrogged traditional banking infrastructures, helping millions access the global economy. On the continent of Africa, it created a similar revolutionary breakthrough with the use of platforms such as M-Pesa, transforming the face of receiving and sending payments. For the investor, this presents a twinned narrative of developed-market modernization and emerging-market leapfrogging.

-2a4164232b0d49f2a0e9abd342673158.jpg)

Source: https://www.gsma.com

The Role of Blockchain

Blockchain is revolutionizing payments through providing decentralized programmable, and borderless alternatives. Stablecoins, such as USDC and USDT, enable payments in dollar denominations on blockchain networks while bypassing established systems. Decentralized payment networks like Stellar and Ripple are trying to simplify remittances. Programmable money is possible through innovative contract systems like Ethereum, with payments triggering further automated financial operations.

Central banks are also coming into the picture with Central Bank Digital Currencies (CBDCs), which may redesign the delivery of monetary policy and funds to consumers. Early-stage CBDCs illustrate how blockchain-based architecture goes mainstream.

For investors, blockchain is a disruptive and complementary layer to payments. Firms that implement blockchain for efficiency gains are poised to be winners while new arrivals could disrupt incumbents in the cross-border and settlement spaces.

Growth Enablers

The payments digital segment has the advantage of several tailwinds. The ongoing growth of e-commerce translates into consistent demand for online payments. End-customer demand for mobile-first experiences drives wallet and app adoption. Efforts from the government to promote a less-cash society further widen support.

On the blockchain network, institutional adoption has become faster. Major payment companies such as Visa and Mastercard now accommodate crypto settlements in certain instances. PayPal and Square also added crypto wallets. Cross-border payments, as a multi-trillion-dollar segment, have always been one of the most lucrative opportunities that blockchain disruption has presented.

Another driver is embedded finance. Non-financial platforms build payment solutions into their ecosystems, such as Uber, Shopify, or TikTok. It blurs the lines between tech companies and financial institutions, expanding the competitive landscape as much as the addressable market.

-3f7830ce4e664fde9050aac825ab3ac5.jpg)

Source: https://www.axios.com

Investment Opportunities

Investors can enter the digital payments market with a variety of themes. Card networks, such as Visa, Mastercard, and American Express, comprise the core of the card industry, boasting a worldwide scale and recurring revenues. Digital native businesses like PayPal, Block (previously Square), and Adyen capitalize on e-commerce and mobile growth. Infrastructure providers and merchant acquirers, such as Fiserv and Global Payments, gain exposure to the back-end rails.

In blockchain, opportunities span from publicly listed companies trying crypto integrations to indigenous crypto assets. Coinbase offers exposure to crypto exchanges, and Ripple Labs, albeit private, a prototype of cross-border disruption, layer-1 protocols like Solana and Ethereum anchor decentralised payment systems. For risk-averse investors, possessing specific tokens creates exposure.

ETFs that are fintech or blockchain-based offer diversified entrance points. Those risks are diversified across incumbents, disruptors, and infrastructures, making them quite handy for investors who are unsure about selecting winners.

Risks and Challenges

Even with strong tailwinds, digital payments and blockchain are threatened. Regulation hangs heavy. Governments are critical of fees, anti-competitive behaviour, and the system-wide effects of blockchain. In countries such as China, the regulatory hammering of Ant Group highlights the unpredictability of policy. Competition is fierce. Prices squeeze as newcomers displace incumbents. Technological disruption remains a constant threat, as blockchain undermines established networks.

Blockchain itself embodies volatility risk. Tokens may wildly oscillate and influence investor mood even in companies with no real connection. Adoption challenges persist, extending beyond scalability and consumer confidence.

Lastly, valuations in the segment can become overheated. Investors tend to favour companies with high-growth potential and are less tolerant of mistakes. A slowdown in transaction growth or regulatory headwinds can induce steep corrections.

Portfolio Positioning

For ordinary investors, digital payments should be part of a portfolio's growth allocation. Big-cap incumbents such as Visa and Mastercard offer stability, dividends, and international coverage. Mid-cap disruptors such as Adyen or Block promise faster growth and greater volatility. Exposure to blockchain offers speculative upside, but it needs to be sized judiciously in terms of risk.

A balanced strategy merges such buckets. Anchoring with proven participants insulates against shocks, and exposure to innovative companies takes shots at innovations. For blockchain, ETFs or token-sized direct commitments can grant optionality minus grand-scale risks.

The time horizon needs to be long-term. Digital payments represent a structural change, not a fleeting trend. Volatility, whether short-term due to regulation or market fluctuations, is unavoidable; yet, the secular trend remains.

Conclusion: Money at the Crossroads

The globe is heading towards a cashless economy driven by digital Rails and blockchain technologies. For investors, that’s not about chasing fintech fever; it’s actually about getting in with one of the world’s most transformative global finance trends. These are extensive opportunities ranging from established giants that control global commerce to blockchain initiatives rewriting the rules of money crossing borders.

Risks, regulation, competition, and valuation are legitimate issues; yet, none of the structural imperatives go away. Ultimately, a bet on digital payments and blockchain is a bet on the future of the economy’s infrastructure. As once with railroads and the Internet before it, digital rails will redefine commerce anew in the 21st century. Patient investors are drawn to the space due to a unique combination of growth, innovation, and survivability.

-b0e51e34cedf43f1a6f5efda61f7cc98.jpg)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.