NVIDIA Q2 FY2026: Surfing the AI Surge with Blackwell, Steering Through China’s Export Challenges

TradingKey - NVIDIA Corporation (NASDAQ: NVDA) reported strong Q2 FY2026 results on August 27, 2025, after market close, driven by robust AI-powered demand and adoption of its next-generation Blackwell GPU platform. The company delivered significant revenue and profit beats overall, with impressive operational leverage and strong free cash flow, reinforcing NVIDIA’s leadership in AI data centers and gaming.

However, its key Data Center revenue slightly missed analyst forecasts, reflecting regulatory restrictions on H20 product shipments to China. This shortfall, combined with cautious Q3 guidance excluding H20 sales to China, generated investor uncertainty. As a result, NVIDIA’s stock declined by about 3% in after-hours trading despite the solid quarter, reflecting market concern over near-term headwinds. Investors remain focused on the sustainability of AI growth amid evolving regulatory and market dynamics.

Source: TradingKey

Key Financial Results

Metric | Q2 FY2026 | Q2 FY2025 | Beat/Miss | Change (YoY) |

Total Revenue | $46.7B | $30B | Beat | +56% |

EPS | $1.08 | $0.67 | Beat | +61% |

Gross Margin | 72.4% | 75.1% | Beat | -2.7pp |

Operating Income | $28.4B | $18.6B | — | +53% |

Data Center Revenue | $41.1B | $26.3B | Slight Miss | +56% |

Gaming Revenue | $4.3B | $2.9B | Beat | +49% |

Professional Visualization Revenue | $601M | $454M | — | +32% |

Automotive Revenue | $586M | $346M | — | +69% |

OEM and Other Revenue | $173M | $88M | — | +97% |

Source: NVIDIA Q2 FY26 Earnings Release

Q3 FY2026 Guidance

• Revenue: $54.0 billion ± 2%, reflecting expected sequential growth but conservatively excluding H20 shipments to China.

• Gross Margins: GAAP 73.3%; Non-GAAP 73.5% ± 0.5%, indicating continued margin improvement.

• Operating Expenses: GAAP $5.9 billion; Non-GAAP $4.2 billion, consistent with sustained R&D and AI ecosystem investments.

• Tax Rate: Approximately 16.5% ± 1%, excluding discrete items.

Segment Performance

Data Center: The Growth Engine

NVIDIA’s Data Center revenue surged 56% YoY to $41.1 billion, accounting for nearly 88% of total revenue. This growth was powered by strong demand for the Blackwell platform, with Blackwell Data Center revenue growing by 17% sequentially. Production of Blackwell Ultra GPUs is running at roughly 1,000 racks per week and is expected to ramp further in Q3. Demand remains broad-based with about half of Data Center revenue from major cloud providers and significant contributions from enterprises and sovereign AI initiatives. Hopper GPUs continues to serve diverse AI workloads beyond advanced reasoning tasks.

CEO Jensen Huang highlighted Blackwell’s roughly 10x energy efficiency improvement for reasoning AI, positioning it as the foundation for a multi-trillion-dollar AI infrastructure investment over the next decade. However, no H20 chip sales occurred in China this quarter due to export restrictions, limiting near-term revenue visibility, though NVIDIA recognized $180 million from previously reserved H20 inventory sold outside China.

Gaming: Accelerating Momentum

The Gaming segment revenue increased 49% YoY to $4.3 billion, supported by strong adoption of the Blackwell-powered GeForce RTX 5060—the fastest ramping "x60" class GPU ever. Expansion of NVIDIA DLSS 4 technology into over 175 titles and enhancements to the GeForce NOW cloud gaming platform further expanded the gaming ecosystem’s reach and engagement.

Professional Visualization and Automotive: Expanding Ecosystem

Professional Visualization revenue grew 32% YoY to $601 million, fueled by new RTX PRO GPUs and partnerships like Siemens advancing industrial digitalization. Automotive revenue jumped 69% YoY to $586 million as the DRIVE AV software platform reached full production and newly launched Jetson AGX Thor AI supercomputers power robotics and autonomous transportation deployments.

Strategic Developments & Financial Discipline

Rubin Architecture and AI Leadership

CEO Jensen Huang highlighted NVIDIA’s ongoing innovation in AI infrastructure beyond Blackwell, introducing Rubin as the next-generation GPU architecture slated for release in early 2026. Rubin is expected to deliver over twice the AI inference performance of Blackwell, with approximately 50 petaflops of FP4 compute—a significant leap from Blackwell’s around 20 petaflops. Rubin GPUs will feature 288 GB of HBM4 memory per GPU and significantly increased memory bandwidth of about 13 TB/s.

Rubin Ultra, arriving in 2027, will further double this performance to 100 petaflops of FP4 compute and substantially increase memory capacity to 1 TB of HBM4e memory per GPU, using four GPU chiplets per package. Rubin Ultra will support extreme rack scaling with up to 576 GPUs per rack, delivering up to 15 exaflops of FP4 inference compute at the rack level.

While Blackwell currently powers NVIDIA’s leading AI platforms such as the RTX PRO 6000 Blackwell Server Edition, Rubin will drive the subsequent wave of AI model training and inference with cutting-edge improvements in compute performance, memory bandwidth, and interconnect speed.

These advancements position NVIDIA to maintain technological leadership in accelerating increasingly complex AI workloads. Collaborations with OpenAI, Novo Nordisk, and others underscore NVIDIA’s deepening role across AI innovation, spanning from model training to drug discovery and industrial AI applications.

Regulatory Impact: H20 Export Restrictions

NVIDIA’s H20 AI chip, primarily designed for the China market, recorded no shipments to Chinese customers in Q2 due to U.S. export license restrictions. CFO Colette Kress explained that the company’s data center compute revenue declined sequentially, mainly because of a $4 billion reduction in H20 sales. NVIDIA’s Q3 FY26 revenue guidance of $54 billion excludes any China-based H20 sales but acknowledges potential shipments if geopolitical conditions permit. Depending on how export licenses evolve, NVIDIA could realize between $2 billion and $5 billion in H20 revenue in Q3.

CEO Jensen Huang emphasized the real possibility of bringing the next-generation Blackwell AI chip to China if export restrictions are lifted and reiterated the strategic importance of U.S. technology leading the Chinese AI market, projected to grow approximately 50% annually with an estimated $50 billion opportunity.

Competitive Landscape: ASICs and Broadcom

NVIDIA’s CEO Jensen Huang highlighted the company’s unique approach, distinct from ASIC-focused competitors. Unlike ASICs, which often struggle to scale due to the complexity of accelerated computing, NVIDIA’s full-stack co-design supports evolving AI models, from generative to multi-modal transformers, across cloud, edge, and robotics. The Blackwell and Rubin platforms integrate fast memory, low-power caches, CPUs, GPUs, and advanced interconnects like NVLink and Spectrum XGS, delivering unmatched performance-per-watt for power-constrained data centers. NVIDIA’s unified programming model and robust software ecosystem solidify its leadership in AI computing, setting it apart from ASIC-only solutions.

Capital Returns and Share Buybacks

In H1 FY26, NVIDIA returned $24.3 billion to shareholders via repurchases and dividends. With $14.7 billion remaining from the previous buyback authorization and a newly approved $60 billion (roughly 1.5% of NVIDIA's current market capitalization) no-expiration repurchase program, NVIDIA signals significant confidence in sustained cash flow and shareholder value generation.

Margin Recovery and Investments

GAAP gross margins rebounded sharply to 72.4%, recovering nearly 12 points sequentially due to easing supply constraints and product mix improvements. The company targets mid-70% non-GAAP gross margins by year-end. Operating expenses increased 38% YoY, reflecting continued investments in R&D, infrastructure, and AI software ecosystems to fuel long-term growth.

Conclusion and Outlook

NVIDIA's Q2 FY2026 results confirm its dominant position in AI, driven by record revenue growth and strong Blackwell platform adoption amid a $3-4 trillion AI infrastructure buildout. The $60 billion share buyback program signals financial strength and shareholder confidence. However, cautious Q3 guidance, due to ongoing China export restrictions on H20 chips, tempers upside, projecting about 15% sequential growth versus a possible 20-25%. Margins are recovering but shifts in product mix and rising R&D require attention.

Looking ahead, NVIDIA's product roadmap through Blackwell and Rubin, combined with its scalable ecosystem including NVLink and Spectrum networking, supports capturing over 50% of the rapidly expanding AI Accelerator Chip Market. Key risks include regulatory hurdles in China, supply chain constraints, and broader macroeconomic pressures. NVIDIA’s forward P/E of around 34-40x is reasonable given its robust growth and strategic AI investments. Stock dips may present buying opportunities in this AI infrastructure leader, though investors should watch geopolitical and market risks that could affect near-term momentum.

What to Watch in Nvidia’s Q2 FY2026 Earnings: AI Growth, Margins, and Market Impact

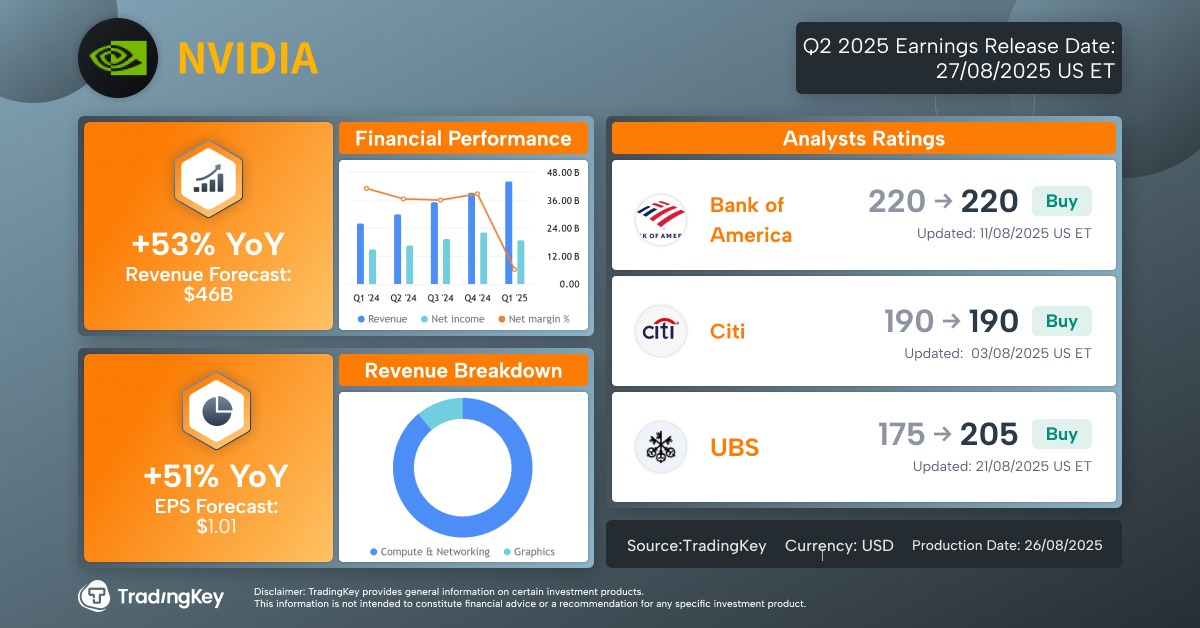

TradingKey - NVIDIA Corporation (NASDAQ: NVDA) will report its Q2 FY2026 earnings on Wednesday, August 27, 2025, after the U.S. market closes. The earnings call is scheduled for 5:00 p.m. Eastern Time. With Nvidia being a bellwether in AI, gaming, and data center markets, and carrying significant weight in major indices such as the S&P 500 and Nasdaq—this earnings report will be closely watched not only for company-specific guidance but also for broader market sentiment.

Since the start of 2025, NVIDIA's stock has risen approximately 30%, reflecting sustained investor optimism around its dominance in AI accelerators. The shares hit a record high of around $182 in mid-August 2025 before a slight pullback, closing at $177.99 on August 22, 2025, amid broader market volatility and anticipation of earnings. This follows a remarkable rebound of over 90% from April 2025 lows, pushing NVIDIA's market capitalization to roughly $4.3 trillion. Despite the gains, the stock trades at a forward P/E multiple of about 40x, underpinned by strong demand for its Hopper and upcoming Blackwell platforms, though concerns over export restrictions to China and potential AI spending slowdowns have introduced caution.

Source: TradingKey

Market Forecast

Metric | Q2 FY2026 Estimate | Q2 FY2025 Actual | Change (YoY) |

Total Revenue | $46B | $30B | +53% |

EPS | $1.01 | $0.67 | +51% |

Gross Margin | 71.8% | 75.1% | -3.3pp |

Data Center Revenue | $41.3B | $26.3B | +57% |

Gaming Revenue | $3.9B | $2.9B | +34% |

Source: Nvidia, Yahoo Finance, S&P Global, TradingKey

Key Investor Focus Areas

AI Data Center Demand and Platform Adoption: Nvidia’s growth is driven mainly by its Data Center segment, which contributes about 89% of revenue. Demand from major hyperscalers like Microsoft, Meta, Amazon, and Google remains strong. Important areas include the rollout of the new Blackwell GPU architecture, expected to deliver up to 4x faster AI training. Insights about order visibility, supply chain status, and the transition from Hopper to Blackwell will shed light on growth sustainability. Any signs of reduced demand, such as hyperscalers developing their own chips, could add pressure, while multi-billion-dollar deals would affirm long-term strength.

Supply Chain and Capacity Updates: GPU supply has been tight, especially for gaming and professional users, though recent signs show easing constraints. Given ongoing macroeconomic challenges and changing regulations in China, clarity on foundry partnerships (TSMC, Samsung) and inventory levels will be pivotal for near-term revenue visibility.

Gaming Segment Outlook: Gaming continues to be a key revenue contributor. New GPU launches and next-generation console cycles may either boost sales or pressure margins due to promotional pricing and costs. Tracking RTX adoption rates, PC hardware spending, and competition from AMD and Intel helps understand potential upside or risk.

Gross Margin and Capital Efficiency: Nvidia targets a gross margin around 71.8% for Q2, rebounding from prior supply chain and export-related setbacks, with plans to reach mid-70% margins later in the year. Monitoring how wafer costs, supply investments, and AI software ecosystem spending affect margins is critical.

Market Impact: Given Nvidia’s massive market capitalization and influence on major U.S. indices, its results often drive broader market trends. Positive surprises could fuel rallies in tech stocks, while any setbacks may trigger wider market sell-offs, especially in semiconductors.

Recent Events and Regulatory Trends

Blackwell Innovations and Production: Nvidia unveiled the Blackwell Ultra GPU at Hot Chips 2025, showcasing substantial gains in AI performance and scalability, with Q4 production ramp expected. Engineering adjustments, including the China-compliant B30A chip, demonstrate adaptability to export controls. Strategic partnerships with Oracle and Dell expand Nvidia’s AI infrastructure ecosystem.

Supply Chain and Trade Pressures: U.S. export restrictions on sales to China, which represent about 20% of Data Center revenue, and potential tariffs amid the election cycle create regulatory uncertainty. While Nvidia’s domestic data center focus limits direct impact, supply chain bottlenecks at TSMC prompt diversification to Samsung packaging solutions. Hyperscalers’ annual AI capital expenditure exceeds $200 billion, but energy consumption concerns and antitrust scrutiny could influence future demand.

Conclusion

Nvidia’s Q2 FY2026 earnings will be a critical test of the AI-driven growth story amid a market near record highs and potential rate cuts ahead. Success depends on the progress of the Blackwell GPU rollout, resilience against China export restrictions, and margin recovery after prior supply constraints. Strong demand and operational execution could drive upside, reinforcing Nvidia’s leadership and lifting broader tech markets. However, risks from regulatory challenges and aggressive capital spending require attention. Clearance on these key issues will help investors clearly see which parts of the growth are real and sustainable, and which may be short-term hype. Staying cautiously optimistic while closely watching these factors is important, as Nvidia’s earnings results could influence the overall market direction into the fall.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.