MGM Resorts International (MGM): Huge Potential in Online Gaming

.jpg) Source: TradingView

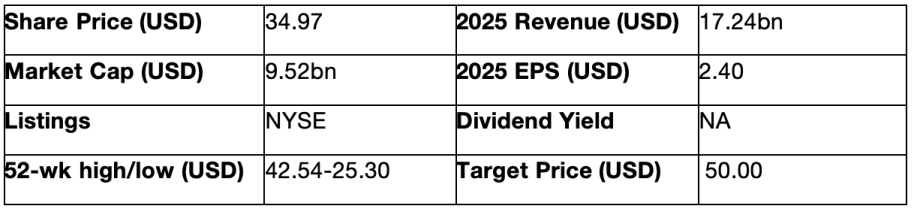

Source: TradingView

Investment Thesis

TradingKey - MGM seems undervalued, as the market does not appreciate the potential of the company’s online betting business, which has a very high growth at 25% and real possibility to have much higher profitability than the traditional on-ground casino business. Also, the economic headwinds the traditional business is facing in the USA and Macau are mostly temporary.

Company Background and Comparison with Sands

MGM Resorts is one of the main casino developers and operators globally. As we previously covered Las Vegas Sands, we would like to continue exploring the casino industry with research on MGM and outline the main differences in their business models.

As of this year, the company operates around 30 resorts globally, but unlike LVS which is more Asia-focused, MGM has a solid domestic base with casinos in Las Vegas, as well as regional properties on the East Coast and the American mid-West. The company still has footprints in Macau, yet at a much smaller scale. They even have hotels in Mainland China (of course, just the hotel and without the casino).

.jpg)

Source: CasinosAvenue

Revenue Breakdown

MGM derives half of its revenue (51%) from casino operations, this may sound a lot but actually it’s the lowest percentage if we compare it with Sands (75%) or Wynn (60%).

The rest of the MGM revenue unsurprisingly comes from hotel accommodation, food & beverage, entertainment and other retail.

What is special about MGM is that among the big traditional casino operators, they make the greatest progress in online gaming, and here comes BetMGM. BetMGM is an integrated platform for sports betting and online casino, with the potential to be a substantial contributor for the company’s profit in the near future. BetMGM is a joint venture between MGM and the British firm Entain. BetMGM revenue is not incorporated in the income statement, however the profit is recorded in the “Income (Loss) from Unconsolidated Affiliates” line (or the very bottom of the P/L statement). For 2024, the total revenue of the BetMGM entity was $2.1bln.

Apart from BetMGM, MGM records a revenue segment called “Digital” which is 3% of the total revenue, but it included other online casino ventures apart from the joint venture.

.jpg)

Source: Company Financials

As mentioned, MGM operations are heavily skewed towards the US, and that reflects on the top line as well – over 70% of the revenue is derived domestically (mostly from Las Vegas) and the rest from Macau, primarily.

However, this will change in the coming years, as there are projects under construction in both Japan and UAE, expected to be completed in the next 3-5 years.

Industry Landscape

LVS performance is way more tied to the Chinese consumer sentiment and post-COVID recover, but in America, MGM faces a different game. In the US, there is no license system, and the market has many participants.

US vs Macau

.jpg)

Source: CasinosAvenue

Las Vegas vs Regional

The US gambling industry can be divided in two geographical sub-segments – Las Vegas and Regional. Las Vegas is way more dependent on tourism and performs better when the economy is doing well. The regional industry is more stable in terms of revenue as it relies on regional consumers, thus it outperforms Las Vegas during less rosy economic times.

.jpg)

Source: CasinosAvenue

BetMGM and the Future of Online Casinos

Currently, the online casino industry is growing rapidly with DraftKings, FanDuel and BetMGM being the top 3 players. Despite the fact that barriers of entry are low, unlike in physical casinos, MGM have a good chance to consolidate more market share due to its expertise in the field and ability to deploy large amounts of capital.

Growth Potential

Currently, the market does not like MGM much due to its exposure to the US casino market – a very mature, highly saturated market with current consumption headwinds. However, there are few major sources of growth:

BetMGM: The iGaming arm of MGM is currently growing at 25%+ year-over-year, and it is about to turn operationally profitable. The main plus of online casinos is the asset-light model allowing quick margin expansion. DraftKings, the main competitor expects EBITDA margin of 25% in 2027, this can serve as a good guidance for BetMGM too.

Macau Recovery: As discussed in LVS, Macau recovery is not yet completed, as many gamblers from lower tier cities have not yet returned to Macau.

Overseas Expansion: The MGM projects in Osaka and Dubai will have a capacity of 2,500 and 1,500 rooms respectively – not as big as MGM Grand Las Vegas (7,000 rooms), bit it’s a great first step of expansion towards new market.

Valuation

.jpg)

Source: TradingKey

Currently, the market leader DraftKings has $21 billion market cap. This means BetMGM by itself should proportionally be around $9.2 billion, and considering that BetMGM is a joint venture, the MGM stake of BetMGM should be valued at around $4.6 billion.

Currently, the market cap of MGM is $9.2 billion itself. If we see it from P/E perspective. The ex-BetMGM market cap of $4.2 billion is just around six times the net income (6.1x PE) as the 2024 net income for the company’s own business is around $750 billion, which is 6.1x

From a P/B point of view, the book value of the equity of the company is around $4 billion. Basically, by buying MGM stock for $9.3 billion market cap, we are getting $4.6 billion worth of online gaming business and a traditional casino business valued at approximately 1x P/B ratio.

Aggressive Share Buyback

.jpg)

Source: Company Reports

The aggressive share buyback program is another supporting point for the valuation of the firm as it demonstrates the conviction of the senior management that shares are undervalued.

Risks

As BetMGM represents the bigger portion of the investment thesis, the biggest risk is also here. Currently, the online casino industry is at early stage, and the competition will be particularly intense, mostly due to the low barriers of entry. If MGM makes strategically bad decisions, this will cost them the whole war.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.