RTX: Driving Breakthroughs in Defense Technology and Commercial Aviation

Investment Thesis

RTX Corporation (NYSE: RTX) is a dominant force in aerospace and defense, perfectly positioned to ride the wave of growing global defense budgets and a booming commercial aviation market. With long-term contracts and leadership in hypersonic missiles and AI-driven systems, RTX offers retail investors a powerful mix of growth and stability. Here’s why RTX is a must-have and how to play it smart.

Why RTX?

· Powerhouse Portfolio: Raytheon’s Patriot missiles and Pratt & Whitney’s F135 engines for the F-35 make RTX a global defense leader, while Collins Aerospace provides top-tier avionics.

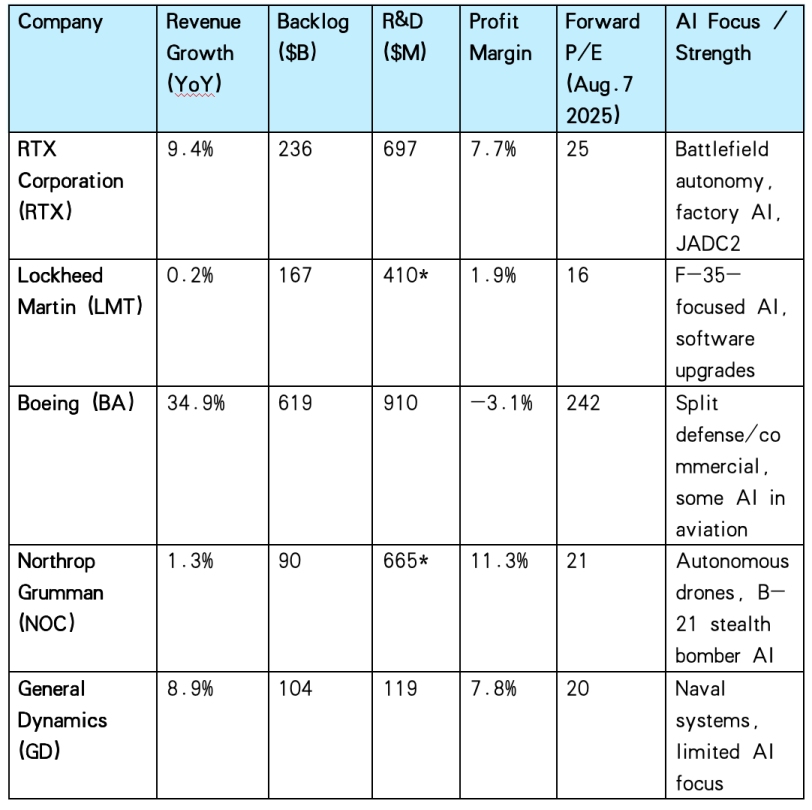

· Huge Backlog: A $236 billion order book secures revenue for years, backed by deals like a $50 billion Defense Logistics Agency contract through 2045.

· Cutting-Edge Innovation: RTX leads in hypersonics and AI-powered targeting, aligning with the Pentagon’s vision for future warfare.

· Balanced Revenue: RTX’s revenue is supported by a strong foundation of reliable government contracts and a rapidly growing commercial aerospace segment, providing both steady income and growth potential.

Upside Potential: Using a forward P/E range of 25–34x applied to expected EPS of $6, RTX has a target price of $150–$204, offering up to 30% upside from current levels.

Strategy: RTX shares trading below $150 may offer a chance to align with the potential $165–$204 target range. Dips often happen during earnings reports or market downturns, making these moments worth watching for entry points.

Source: TradingKey

Company Overview

From its Arlington, Virginia headquarters, RTX Corporation drives innovation across aerospace and defense, employing 167,000 people to deliver solutions that span battlefields to boardrooms. Formed through the 2020 union of Raytheon’s missile expertise and United Technologies’ aerospace legacy, RTX operates three divisions: Raytheon, crafting missile systems and defense technologies; Pratt & Whitney, building engines for fighter jets and commercial planes; and Collins Aerospace, supplying avionics and mission systems. Approximately half of RTX’s revenue comes from U.S. and allied government contracts. The other half is generated from commercial clients, including major aerospace companies like Airbus. RTX’s ability to arm nations with Patriot missiles while powering global air travel with A320neo engines makes it a versatile giant in a world of rising conflicts.

.jpg)

Source: RTX

Financials — Quarterly Highlights (Q2 FY2025)

RTX delivered strong Q2 2025 results (ended June 2025), surpassing expectations.

· Revenue: $21.6 billion, up 9% YoY, beating forecasts of $20.68 billion by 4.45%. Growth was driven by a 16% increase in the commercial aftermarket, 7% increase in the commercial original equipment, and 6% increase in defense sales.

· EPS: Adjusted EPS of $1.56, up 11% YoY, exceeding consensus of $1.44 by 8.33%. GAAP EPS was $1.22, impacted by $0.28 in acquisition accounting adjustments and $0.06 in restructuring costs.

· Free Cash Flow: Outflow of $72 million, impacted by $250 million in compensation costs due to defects in powdered metal engine parts requiring extra inspections and repairs, and $175 million in tariff expenses, partially offset by operational improvements.

· Backlog: Record $236 billion, up 15% YoY, driven by $5 billion in Raytheon missile defense awards and 1,000+ Pratt & Whitney GTF engine orders.

· Capital Returns: $1.3 billion returned so far in 2025 via dividends and buybacks, with an 8% dividend increase; approximately $37 billion in total capital returns from 2020 through the end of 2025.

Despite the strong performance, a four-week work stoppage at Pratt & Whitney and tariff headwinds ($125 million in H1 2025) pressured cash flow. RTX mitigated tariff impacts through USMCA exemptions and pricing actions, with full-year tariff costs revised to $500 million.

Q3 Guidance and Outlook: RTX raised its full-year 2025 adjusted sales outlook to $84.75–$85.5 billion (from $83–$84 billion) and EPS to $5.80–$5.95 (from $6.00–$6.15), reflecting tariff headwinds but strong demand. Free cash flow guidance remains at $7.0–$7.5 billion, supported by H2 recovery from the Pratt work stoppage and improved cash taxes.

Revenue Breakdown (Q2 FY2025)

.jpg)

Source: RTX, TradingKey

RTX’s revenue reflects its diversified portfolio, balancing defense reliability with commercial growth.

Collins Aerospace contributed approximately $7.62 billion (35%) of total RTX revenue. This division designs avionics like cockpit displays, provides ejection seats for military jets such as F-15 and F-22, and cabin systems for commercial planes. It achieved about 13% growth in commercial aftermarket upgrades and an 11% increase in defense programs including the F-35.

Pratt & Whitney generated about $7.63 billion (35%), producing engines like the F135 for the F-35 and the geared turbofan (GTF) for the Airbus A320neo. Despite a four-week work stoppage, this division achieved roughly 12% revenue growth.

Raytheon Technologies reported sales of approximately $7.00 billion (32%), delivering missile systems such as Patriot and AMRAAM and advanced sensor systems. Raytheon’s reported sales grew by 8% YoY, driven by strong global demand for defense programs.

Growth Potential

RTX is soaring on a global tailwind, with defense budgets racing toward $2.5 trillion by 2030 and air travel climbing 5% annually. The U.S. 2025 defense budget of $849 billion, including $50 billion for air and missile defense, fuels Raytheon’s Patriot and AMRAAM programs. A $50 billion, 20-year Defense Logistics Agency contract, running through 2045, and a $3.5 billion AMRAAM deal lock in decades of revenue.

Pratt & Whitney benefits from rising airline demand, with aftermarket sales surging 16% as global fleets expand. RTX’s innovation pipeline is equally compelling: the Hypersonic Attack Cruise Missile, slated for 2027, promises Mach 5+ speeds, while the MTS-A HD targeting system enhances naval helicopter precision, drawing interest from Australia to Saudi Arabia.

RTX’s AI push, through a partnership with Shield AI, embeds autonomous target recognition in systems like MTS-A HD, while its proprietary AI platform slashes avionics development time by 30% at Collins Aerospace, boosting efficiency. Contributions to the Pentagon’s JADC2 program weave real-time data across air, land, and sea, cementing RTX’s role in future wars.

Competitor Analysis

RTX holds a 12% share of the U.S. defense market with a diverse portfolio in missile defense, aerospace engines, and commercial products. Its Patriot missile system, used by 19 nations, competes effectively with Lockheed Martin’s more specialized THAAD. Pratt & Whitney’s exclusive F135 engine powers the F-35, a key asset in U.S. military aviation.

RTX also leads in advanced radar and electronic warfare, offering integrated defense solutions across air, land, and sea. Supported by a strong backlog, its balanced defense-commercial mix delivers stability and innovation. While AI enhances capabilities like autonomous targeting, it complements RTX’s core strengths.

Note: R&D figures marked * are estimated for Q2 2025 by applying each company’s historical R&D-to-revenue percentage to reported quarterly revenue. Data sources include StockAnalysis and TradingKey as of Q2 2025.

Valuation

RTX trades at a forward P/E of about 25x, above the peer average near 21x (excluding Boeing), reflecting its hybrid defense-commercial model, strong AI innovation, and a sizable billion backlog that offers multi-year revenue visibility and lowers short-term risks. Higher R&D spending supports its technology leadership and growth outlook. For comparison, Lockheed Martin’s forward P/E near 16x reflects its narrower government focus and lower growth potential.

With a trailing P/E of about 34x based on a $4.6 EPS, the forward P/E based on the 2025 EPS forecast of $6 would naturally decrease to around 25x, reflecting the expected earnings growth.

Thus, a reasonable forward P/E range is 25x to 34x, and the target price is $150–$204:

· 25x reflects earnings-based valuation,

· 34x reflects the current market premium for growth and innovation.

Risks

· Supply chain bottlenecks, especially in semiconductors, may delay Pratt & Whitney engine production and Raytheon missile deliveries.

· Tariffs, estimated at $500 million in 2025, could compress margins despite mitigations like free trade zone usage.

· A potential de-escalation of global conflicts might reduce defense spending growth.

· Competitors are advancing in hypersonics and AI, posing challenges to RTX’s leadership.

· Regulatory changes, including stricter export controls, may restrict international sales.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.