Size Matters? Royal Caribbean Cruises Don’t Think So

Investment Thesis

TradingKey - Royal Caribbean Group (RCL), as the world’s second-largest cruise operator, demonstrates industry-leading recovery and competitive strength in the post-pandemic era through robust revenue growth (18.6% increase in 2024, with net income surging 70.6%), exceptional operational efficiency (17.45% net yield, 108.50% occupancy rate), prudent financial management (debt reduced to $19.7 billion, liquidity at $7.1 billion), and forward-looking growth strategies (new ship programs and exclusive destination development).

Compared to Carnival Corporation (CCL) and Norwegian Cruise Line Holdings (NCLH), RCL achieves higher profitability and market adaptability, generating greater revenue per unit of capacity while solidifying its position in the premium market through innovative technology and diversified strategies, making it a top investment choice in the cruise industry.

Source: TradingView

Source: Royal Caribbean Cruises, TradingKey

Company Overview

Royal Caribbean Group (RCL), the world’s second-largest cruise operator (behind Carnival Corporation), operates three cruise brands: Royal Caribbean International, Celebrity Cruises, and Silversea Cruises, and owns expanding land-based vacation experiences such as Perfect Day at CocoCay. As of Q1 2025, Royal Caribbean Group operates 67 ships with nearly 180,000 berths, covering all seven continents, over 120 countries, and more than 1,000 destinations.

Revenue Breakdown

Royal Caribbean Group’s revenue primarily comes from ticket sales and onboard spending. According to 2024 annual report data, ticket sales account for 70% of total revenue, covering various itineraries and cabin types, while onboard spending, including dining, beverages, casinos, spas, shore excursions, and shopping, contributes 30%. The North American market accounts for 64% of revenue, indicating a high concentration in its primary market.

Industry Competitive Analysis

The global cruise industry, having faced severe challenges during the pandemic, is experiencing a robust recovery. Royal Caribbean Group (RCL), Carnival Corporation (CCL), and Norwegian Cruise Line Holdings (NCLH), as the industry’s three major players, have adopted different strategies to address market changes and achieve growth. According to Cruise Market Watch data, Carnival held a 42.9% market share in 2024, followed by Royal Caribbean at 25.7%, Norwegian at 14.1%, and MSC at 7.2% (Cruise Market Watch Market Share). In terms of fleet size, Royal Caribbean’s fleet is second only to Carnival’s 92 ships, far surpassing Norwegian’s 32 ships. However, Royal Caribbean has shown a clear lead in stock price performance over the past two years.

(For detailed information on CCL, please refer to: Carnival Corp (CCL): Debt is still a Stone on the Neck )

Analysis of Stock Price Disparities

Revenue Growth and Profitability

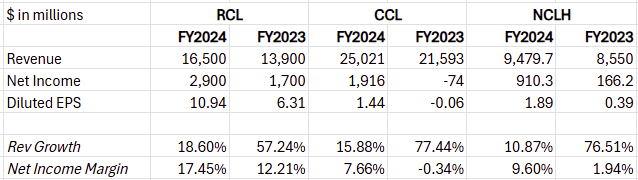

In the post-pandemic era, RCL demonstrated industry-leading recovery in 2024. Its total revenue reached $16.5 billion, up 18.6% year-over-year, with net income surging 70.6% to $2.9 billion and earnings per share rising 73.4% to $10.94, showcasing exceptional profitability. In comparison, CCL’s total revenue grew 15.9% to $25.021 billion, with net income turning positive at $1.916 billion and earnings per share at $1.44. NCLH reported total revenue of $9.4797 billion, up 10.9%, with net income increasing to $910.3 million and earnings per share at $1.89, though its base is relatively smaller. RCL’s outstanding performance and positive 2025 guidance further solidify its leadership in the cruise industry’s recovery. Meanwhile, NCLH’s revenue decline and losses in Q1 2025 highlight a clear divergence in industry momentum.

Source: Company Reports, TradingKey

Balance Sheet Strength

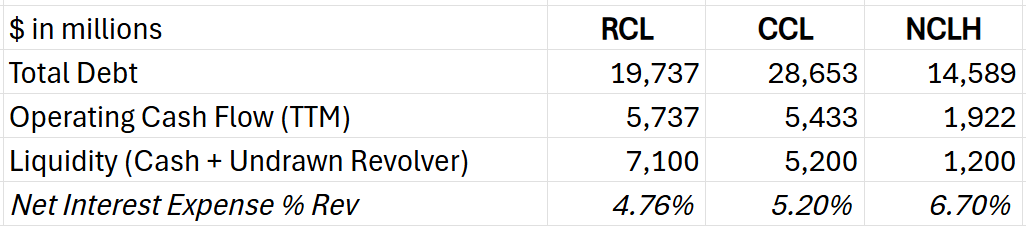

RCL demonstrates exceptional debt management capabilities and robust financial performance. From a total debt of $23.4 billion in 2022, RCL reduced it to $19.7 billion by 2025, significantly optimizing its balance sheet. Meanwhile, its operating cash flow increased to $5.7 billion, with liquidity reserves reaching $7.1 billion, highlighting strong financial resilience. In contrast, CCL and NCLH maintain non-investment-grade credit ratings, resulting in borrowing costs approximately 0.5% higher than RCL's on average. In 2024, RCL successfully achieved investment-grade credit metrics and proactively repaid all secured and collateralized debt, substantially lowering financing costs and further strengthening its market competitiveness.

Although CCL has made some progress in debt reduction, NCLH's debt increased due to new ship deliveries in the first quarter of 2025, reflecting its current phase of intensive capital expenditure and significant short-term leverage pressure. With its outstanding financial strength and risk management capabilities, RCL not only exhibits greater market resilience but also secures new financing on more favorable terms, laying a solid foundation for future development.

Source: Company Reports, TradingKey

Operational Excellence and Capacity Management

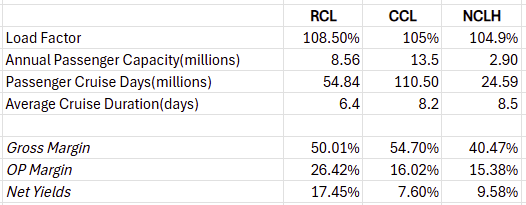

RCL’s net yield of 17.45% significantly outperforms CCL’s 7.60% and NCLH’s 9.58%, demonstrating superior profitability. Its 108.50% occupancy rate indicates that RCL achieves higher revenue with the same capacity through premium services, differentiated products, and precise pricing. Although its gross margin is slightly lower than CCL’s, RCL’s operating margin of 26.42% far exceeds CCL’s 16.02% and NCLH’s 15.38%, driven by efficient cost management, reflecting an excellent cost structure and operational efficiency. In terms of itinerary duration, RCL focuses on short- to medium-length voyages, as longer voyages yield slower marginal profit growth, highlighting its differentiated operational strategy.

Overall, compared to CCL’s larger capacity scale, RCL achieves higher revenue and profit contribution per unit of capacity through higher occupancy rates and net yields, enabling faster profit growth and higher market valuation with a smaller scale.

Source: Company Reports, TradingKey

Growth Potential

By 2027, global cruise giants Royal Caribbean (RCL), Carnival (CCL), and Norwegian Cruise Line (NCLH) are all focusing on fleet expansion and modernization, but their strategies and growth potential differ significantly.

Comparison of Expansion Strategies: RCL is pursuing an aggressive innovation strategy, planning to launch Star of the Seas (2025) and Icon of the Seas (2026), adding over 11,000 berths, while undertaking “amplification” upgrades for flagship vessels like Oasis of the Seas and Harmony of the Seas, incorporating cutting-edge facilities and experiences to enhance appeal in the premium market. CCL is focusing on steady expansion, planning to receive eight new ships between 2025 and 2033, including Sun Princess (2025) and “Excel”-class vessels (2027), adding nearly 30,000 berths. NCLH’s expansion cycle is longer, with plans to deliver 13 new ships by 2036, adding over 25,000 berths. While all three face short-term pressures from new ship capital expenditures and drydock capacity losses, RCL’s rapid introduction of new ships and large-scale upgrades positions it to quickly capture a larger share of the premium market, demonstrating stronger short-term revenue growth potential.

Strategic Differences and Cost-Benefit Analysis in Destination Development: In terms of destination development, RCL is the most proactive, planning to have six exclusive destinations by 2027, four of which are newly developed, covering markets in Mexico, the Bahamas, and the South Pacific. These new destinations significantly enhance appeal to the high-end market through unique experiences (such as water parks and cultural villages), boosting both onboard and onshore spending revenue while substantially reducing long-term port costs through economies of scale and the elimination of third-party port fees, with expected savings of 20% to 30%, further improving profit margins. In contrast, CCL plans to develop one new destination, while NCLH has no plans for new private destinations, relying more on existing destinations and third-party ports, resulting in lower cost savings.

Valuation

Royal Caribbean (RCL), through proactive debt management and flexible capital allocation, demonstrates exceptional financial flexibility, providing a stronger buffer against future external shocks. Its diversified destination strategy and forward-looking technology investments (such as Starlink internet service) give it a competitive edge in market adaptability, showcasing a more agile operational strategy. This is the primary reason why RCL's current price-to-earnings ratio (29x) commands a premium over Carnival (16x) and Norwegian Cruise Line (16x).

However, the market has largely priced in most of RCL's positive factors, leaving limited room for further margin improvement. To sustain its high valuation, RCL must rely on new destinations coming into operation to further drive revenue and profit growth, particularly by enhancing high-end market appeal and onshore spending revenue through unique experiences (such as water parks and cultural villages), thereby solidifying its industry-leading position.

Risk

- Economic Recession: Reduced consumer spending could lead to lower cruise demand.

- Geopolitical Instability: Political unrest or conflicts could impact itinerary safety and passenger confidence.

- Fuel Price Volatility: Rising oil prices could increase operating costs and affect profitability.

- Intensified Competition: Competitors launching new ships or promotional campaigns could impact market share and pricing power.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.