Carnival Corp (CCL): Debt is still a Stone on the Neck

Share Price (USD) | 29.79 | 2024 Revenue (USD) | 25.02bn |

Market Cap (USD) | 38.71bn | 2024 EPS (USD) | 41.44 |

Listings | NYSE | Dividend Yield | - |

52-wk high/low (USD) | 30.46-13.78 | Target Price (USD) | 30.00-35.00 |

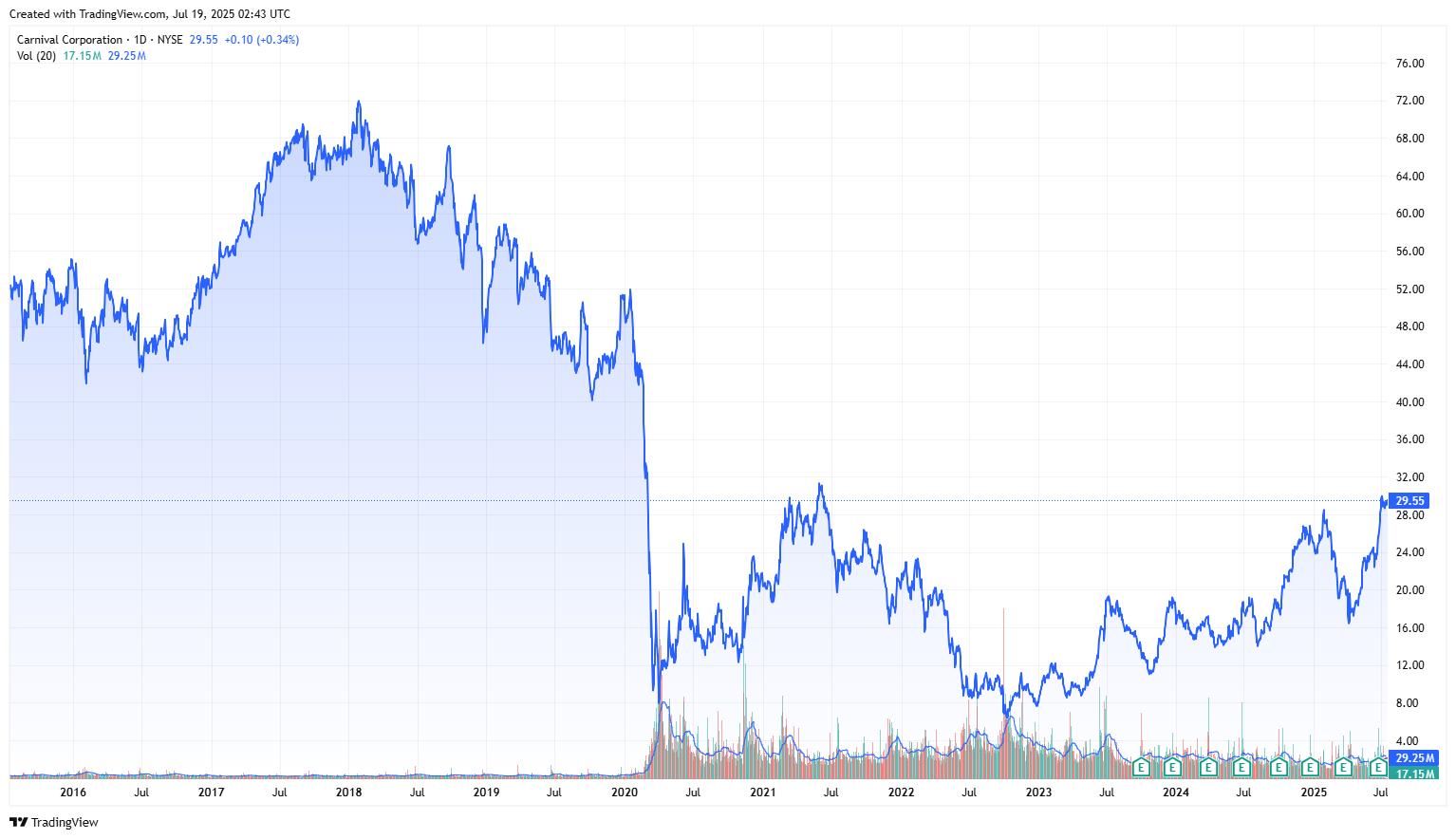

Source: TradingView

Investment Thesis

TradingKey - The huge debt of Carnival remains a stone on the neck, as this will prevent the company renewing its already old fleet (in contrast with competitors). However, the overall interest towards cruise trips, as well as the development of exclusive-port amenities, will bring modest top line and margin expansion.

Company Description

Carnival Corporation (CCL) is a cruise line operator with leading brands. The company's portfolio consists of nine different brands that are diversified across product offering, target consumer, and travel destinations.

Source: Company’s Official Page, Cruise Solutioner’s Comprehensive Guide

The company operates several cruise destinations across the Caribbean, exclusively for Carnival guests (most notably Half Moon Cay, Amber Cove, Mahogany Bay, and Celebration Key as the newest).

How Does Carnival Make Money?

65% or nearly two thirds of CCL revenue is sourced from passenger tickets with the remaining 35% coming from onboard. Passenger tickets often include accommodation, meals, amenities, childcare, destinations visits, and various forms of entertainment. Onboard revenues are goods and services sold in excess of items included in the passenger tickets. These goods and services often include beverage sales, casino gaming, shore excursions, retail sales, photo sales, internet, spas, specialty restaurants, art, and laundry/dry cleaning.

The company mostly caters travelers from North America and Australia - 70%, while the remaining 30% are predominantly from Europe.

For FY '24, 33% of the fleet is located in the Caribbean, 17% in Europe (ex. Mediterranean), 14% in Mediterranean, 6% in Alaska, 7% in Australia and New Zealand, and 23% in Other.

Industry and Competition

There are three companies that control the entire cruise industry and CCL is the largest one. The other two are Royal Caribbean Group (RCL) and Norwegian Cruise Line Holdings (NCLH). In terms of passenger volume CCL holds 42%, RCL – 27% and NCLH – 15%. Carnaval also has the biggest fleet with 92 ships (vs RCL 65, and NCLH 32). The market share of the company has been rather stable throughout the years, implying high barrier for new potential entrants.

However, Carnival EBITDA margin has recently been around 28%, compared to the other two – 35% each. We can explain this with the fact that Carnaval being the largest one is more exposed to mass market unlike the others being exposed towards more high-end customers. Additionally, CCL’s fleet is the oldest (16 years vs the competitors – 12-13 years), and older fleet is less fuel-efficient.

Growth Drivers

The Cruise Lines International Association (CLIA) has predicted both the passengers’ volume and the revenue for the whole industry to grow at high single digits in the coming years.

However, the situation with CCL is a bit more complex. They will probably not grow as fast as the rest, and here’s why:

CCL operates at a highest capacity among the three companies at above 100%. The way to solve this is to do a more aggressive fleet renewal. This could increase the capacity and also cut the fuel-related costs (because newer fleet is more cost-efficient). However, here comes the issue of the large debt. Among the three, CCL has the largest amount of debt and pays the most expensive debt, forcing the company to focus on debt repayment rather than investing in new fleet. Carnival did not order any new ships for delivery in 2025, unlike Royal Caribbean and Norwegian, which are expanding more rapidly.

Source: Company Reports

This seems like the biggest obstacle for Carnival to expanding the profitability. However, there will be certain tailwinds for the margins:

CCL is already focusing on restructuring the debt. Currently, the operating cash flow track record after COVID is strong and if that continues (high certainty), the credit rating of CCL will improve, and it will allow them to further refinance the debt at a way more favorable rate.

Focusing on exclusive ports. Celebration Key is the newest line-exclusive port for the company, which opened last week. CCL is also renovating Half Moon Cay and Mohogany Bay. This means there will be better facilities and amenities where travelers can spend more time and money, creating more of a closed circle economy.

Valuation

Our DCF model implies a target price of $30.00-$35.00, a moderate upside reflecting both the headwinds and the tailwinds. Further to this, the current PE ratio is not far from the historical average.

Source: Macrotrends

Risks

Tax: Recently there have been suggestions to impose taxes on the cruise industry. Currently, CCL pays minimal taxes to the US government despite the large-scale operations. This is because Carnival is registered in Panama, and most of the cruises travel under non-US flag. If the industry gets taxed properly, this will be a significant hit towards their profitability. However, crafting such law is quite complex as it directly interferes with Maritime Law, as cruises are part of the broader shipping industry, and such law revamp will affect not only cruises but also tankers, making the impact quite big.

Macro remains a risk: Cyclical downturn may drive lower discretionary spending for cruises and passenger spending, and this can affect the cash flows, which can affect the path of CCL to improve its credit ratings and get better financing. We should bear in mind that CCL is the most exposed to the mass consumer.

Competitive pressures may intensify: The other two players are expanding fleet more aggressively, which can make CCL a lagger when it comes to price and overall quality of service.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.