Are Drones the Next Big Opportunity in the AI Boom?

TradingKey - Drone stocks in the U.S. have taken off recently, and it’s not just hype. The rally is being driven by a series of executive orders signed by President Trump aimed at loosening regulations and speeding up the rollout of next-gen aviation technologies. Investors are taking note—shares of Archer Aviation, Joby Aviation, and Vertical Aerospace surged again this week, signaling growing confidence that drones may be entering a new phase of growth.

At the center of it all is a push for the FAA to fast-track rules for "Beyond Visual Line of Sight" (BVLOS) operations. In plain English, that means drones could soon be allowed to fly beyond what a human operator can physically see. This one regulatory shift could unlock commercial use cases that were previously stuck on the runway—think last-mile delivery, crop spraying, infrastructure inspection and more. These are high-frequency, high-need applications that simply haven’t been scalable—until now.

Meanwhile, eVTOL aircraft (electric vertical take-off and landing vehicles), which are essentially “flying taxis.” Companies like Joby and Archer have made real progress in test flights, but red tape around certifications has been a roadblock. These new policies show that Washington is finally ready to move, with government backing that could bring eVTOLs to the market as soon as 2025. This could be a game-changer for short-distance travel—and the U.S. wants to be a global leader in the space.

Notably, the U.S. government is making a stronger push to reduce its reliance on foreign-made drones, especially from China. Currently, DJI dominates the global market, with over 70% share, and an even higher footprint in the U.S. That’s raised growing concerns around data security and supply chain resilience. Washington is now turning this into a strategic priority—creating an opening for domestic drone makers to step up and fill the gap, especially on the defense and enterprise side.

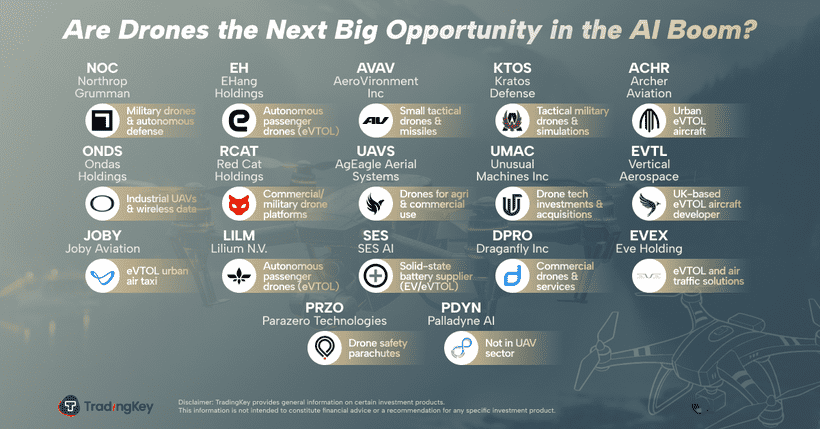

The U.S. drone industry is taking shape across two broader segments. On one hand, defense-focused firms such as Northrop Grumman, Kratos Defense, and AeroVironment are positioned to benefit from consistent government contracts and expanding military budgets. Northrop, for instance, is known for its high-performance surveillance and strike drones, which increasingly integrate AI for swarm and autonomous operations. Kratos, by contrast, focuses on cost-efficient, mass-deployable systems ideal for fast-paced missions. AeroVironment has carved out a niche in small, portable drones used by frontline units. These platforms tend to have steady funding and relatively high reliability from an earnings perspective, making them attractive during periods of geopolitical uncertainty.

The commercial side of the market is equally dynamic, though earlier in its monetization cycle. Alongside the high-profile eVTOL players, there’s growing activity in the broader drone infrastructure ecosystem—particularly in areas like flight control algorithms, autonomous navigation, airspace integration and remote communications. AI-driven technologies are at the core of this evolution. For example, SES AI and Ondas Holdings are working on the "operating systems" of advanced drone flight—making these systems smarter, faster, and more energy-efficient, all while reducing cost and increasing safety.

Beyond the flashier headlines, there’s also a strong real-economy segment developing in industrial and professional-grade drone deployments. These range from precision agriculture and surveying to utility maintenance and emergency services. Companies including AgEagle and Red Cat are developing drones tailored for crop health monitoring, pesticide optimization, and farm analytics. Draganfly is tackling healthcare logistics, with UAVs capable of delivering medical supplies to remote or emergency locations. ParaZero is focused on safety solutions, designing drone parachutes to enable risk-managed landings in mission-critical environments. While these use cases may not attract the same media buzz, they tend to offer stable demand, faster deployment, and stronger visibility into near-term revenue.

From an investor’s perspective, this new wave of drone disruption looks like a multi-stage opportunity. Over the short term, defense-oriented players are better positioned to capture growth through repeat contracts, driven by government spending and heightened global tensions. Looking toward the mid-term, commercialization milestones within eVTOL and AI-based drone control—especially type certification—could bring step changes in both adoption and valuation.

Longer term, the real upside may lie with companies that can operate across the full stack—building not just the aircraft, but the supporting platforms, services and infrastructure. As low-altitude airspace becomes increasingly regulated and connected, those end-to-end integrators could emerge as dominant players in a new aerial economy.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.