Adobe’s Quiet Reinvention Is Working

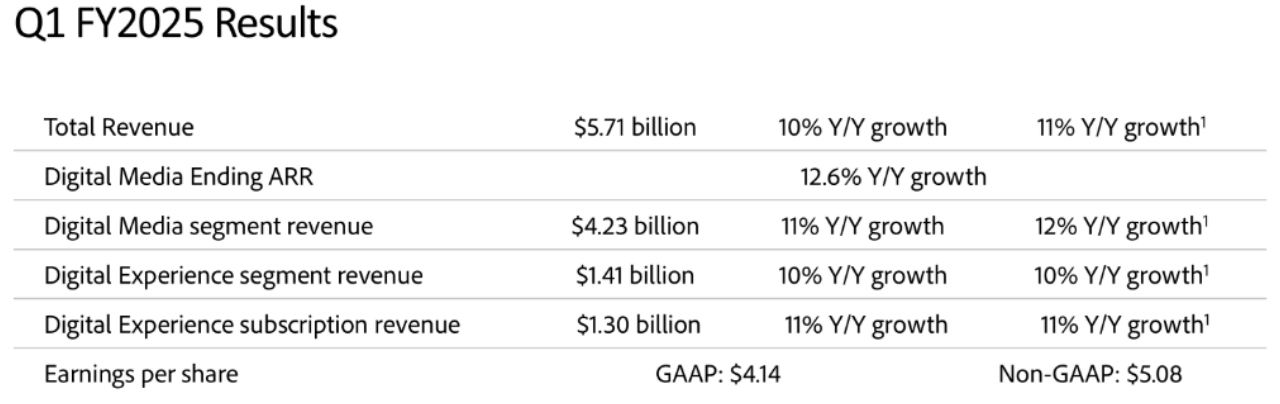

- Adobe reported Q1 FY25 revenue of $5.71 billion, with non-GAAP EPS up 13% year-over-year to $5.08.

- Business Professionals & Consumers segment grew 15% YoY, outpacing the 10% growth in Creative & Marketing Professionals.

- Firefly and GenStudio reached $1.125 billion in ARR, with 90% of paid users adopting new video generation features.

- Operating cash flow hit a Q1 record of $2.48 billion, supporting $3.25 billion in share buybacks during the quarter.

Adobe's (ADBE) Q1 FY25 results show a company under the process of a strategic transformation that transcends margin sustainability or AI jargon. While Wall Street is concentrating on the reconfirmed guidance as well as the all-time-high $5.71 billion revenue, the actual tale is one of the way Adobe is re-architecting its product framework and segmentation for tapping AI-native revenue streams across both customer sets: “Creative & Marketing Professionals” and “Business Professionals & Consumers.” In a world where platform versatility is the mark of enterprise longevity, Adobe is making the transition from a product-led model to a solutions-based flywheel. Far from a bet against macro volatilities, it's a rewiring from the very roots of the growth engine to maintain a high-margin, high-ARR digital kingdom for a decade from now.

The crux of Adobe's transformation is the intentional segmentation strategy at the heart of the company, unmasking operational realities hidden behind all-in-one ARR numbers. The 15% YoY growth in the Business Professionals & Consumers division has now surpassed the 10% growth in the erstwhile leading Creative & Marketing division. The spike captures the monetization growth tip of Acrobat AI Assistant and native embedding of Express flows into documents, a harbinger that Adobe is no longer selling tools but cognitive productivity embedded.

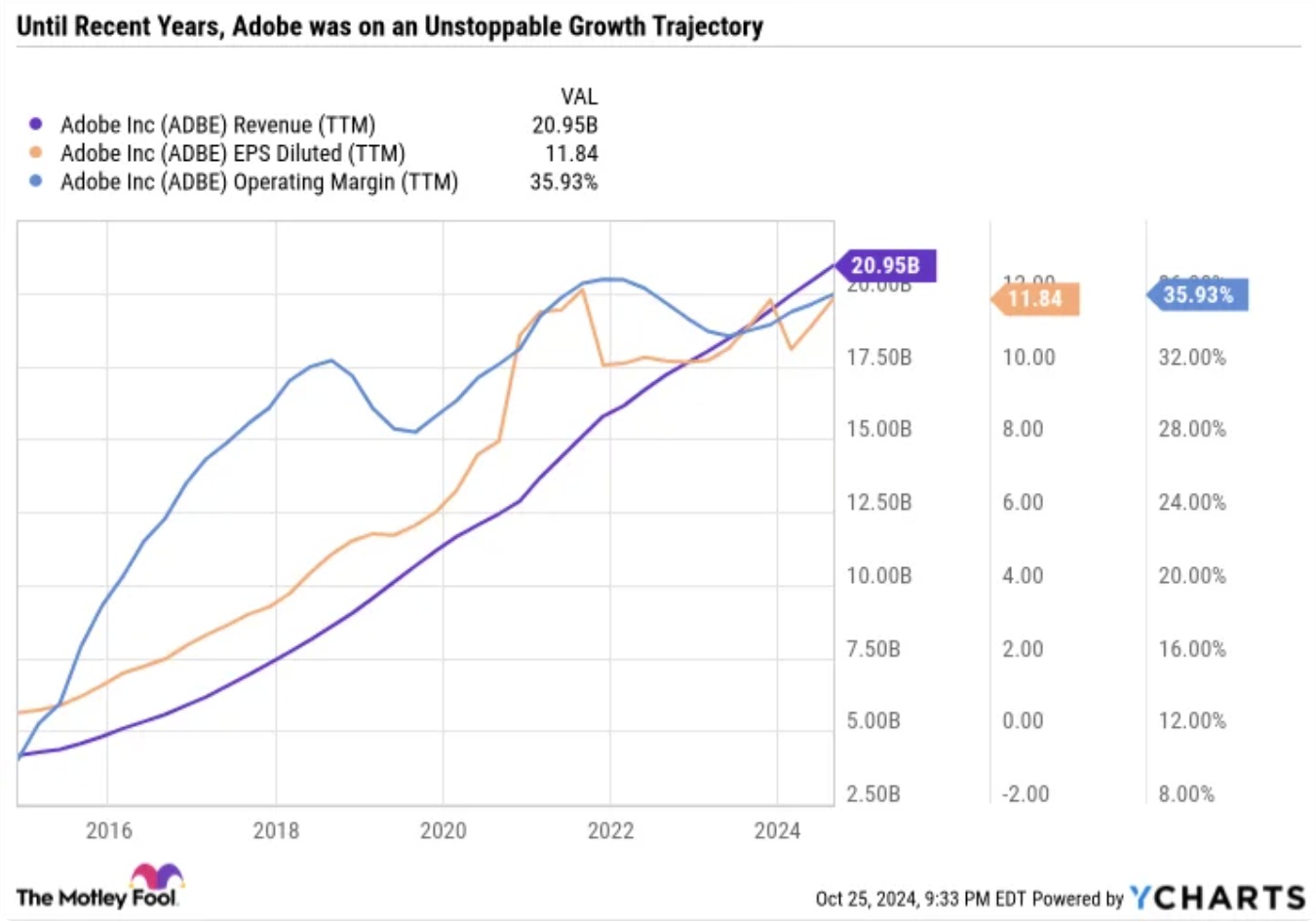

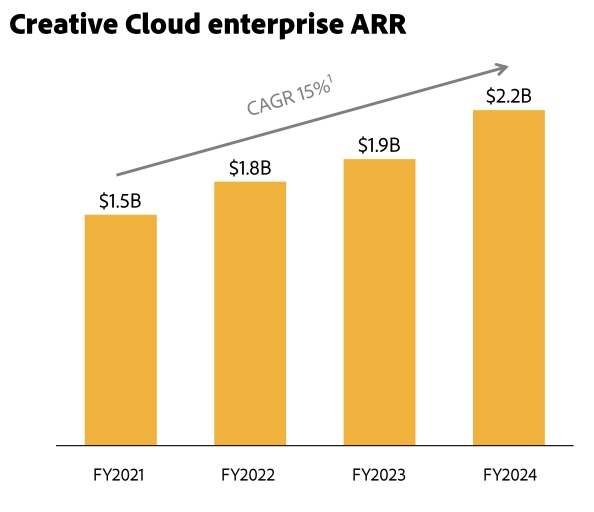

The transition unlocks downstream pricing, stickier usage, and subtle de-risking of dependence on fluctuating creative marketplaces. But this is not a zero-sum play; it's a two-way flywheel model, with enterprise-class GenStudio products and Firefly APIs enabling a compounded ARR impact in marketing automation. If Adobe pulls it off, it will not only ride the AI wave, it will also encode AI into the daily workflow of knowledge workers, creators, and advertisers as well. This shift didn’t start with Firefly or Acrobat AI — Adobe’s transformation into a recurring-revenue powerhouse began over a decade ago, as the chart below shows:

Scaling Adobe's Cognitive Operating System

The three pillars of Adobe's business model are its Creative Cloud, the Document Cloud, and the Experience Cloud, with the underlying infrastructure unified by workflow convergence and generative AI. The Creative Cloud, with the generative capability of Firefly, drove $4.23 billion in Digital Media revenue during Q1 FY25, up 11% YoY. The Document Cloud, with the inclusion of AI Assistant and Express, has grown from a static PDF platform to an interactive, cross-device productivity platform. The Experience Cloud registered $1.41 billion in revenue, supported by a 50% YoY increase in Adobe Experience Platform (AEP) and related app subscriptions.

Source: Adobe Q1FY25 Earnings Call Script

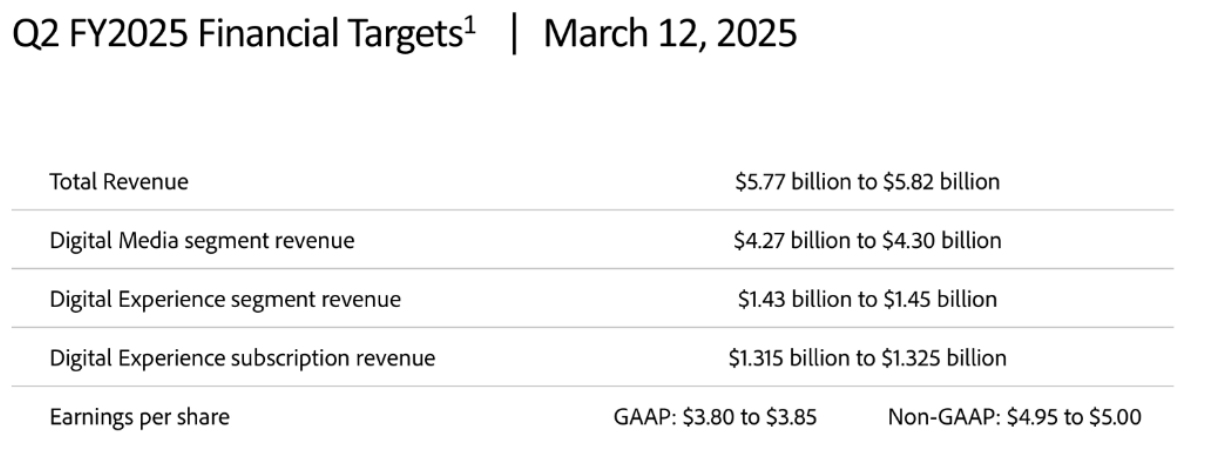

Source: Adobe Q2FY25 Earnings Call Script

Adobe's shift towards generative AI is much more than skin-deep. Already, products such as Firefly Services, Firefly App, and GenStudio have achieved a $125 million ARR book of business by the end of Q1, which Adobe forecasts will double by the end of the year. Significantly, GenStudio now exceeds $1 billion in ARR, exhibiting its development as a platform for enterprise content personalization. For creators, Firefly's most recent update brings video generation, complementing its current capabilities in vector and image creation. More than 90% of paid Firefly Pro and Standard customers are now leveraging video generation features, an excellent harbinger for monetization prospects down the line.

What is transformational is the way Adobe is merging productivity with creativity. The firm has integrated Express with Acrobat workflow so that users can seamlessly move from static PDF to dynamic presentation and infographic with a single click, essentially redefining how organizations make their content. The cross-functional utility thus spurred the usage of Express through Acrobat 10x YoY, and Acrobat web usage grew 50%. With form factor merging with functionality and fidelity, Adobe is becoming less of a set of tools and more of a complete-stack cognitive operating system for content.

Adobe vs. the Field: Reinventing the Moat in the AI Arms Race

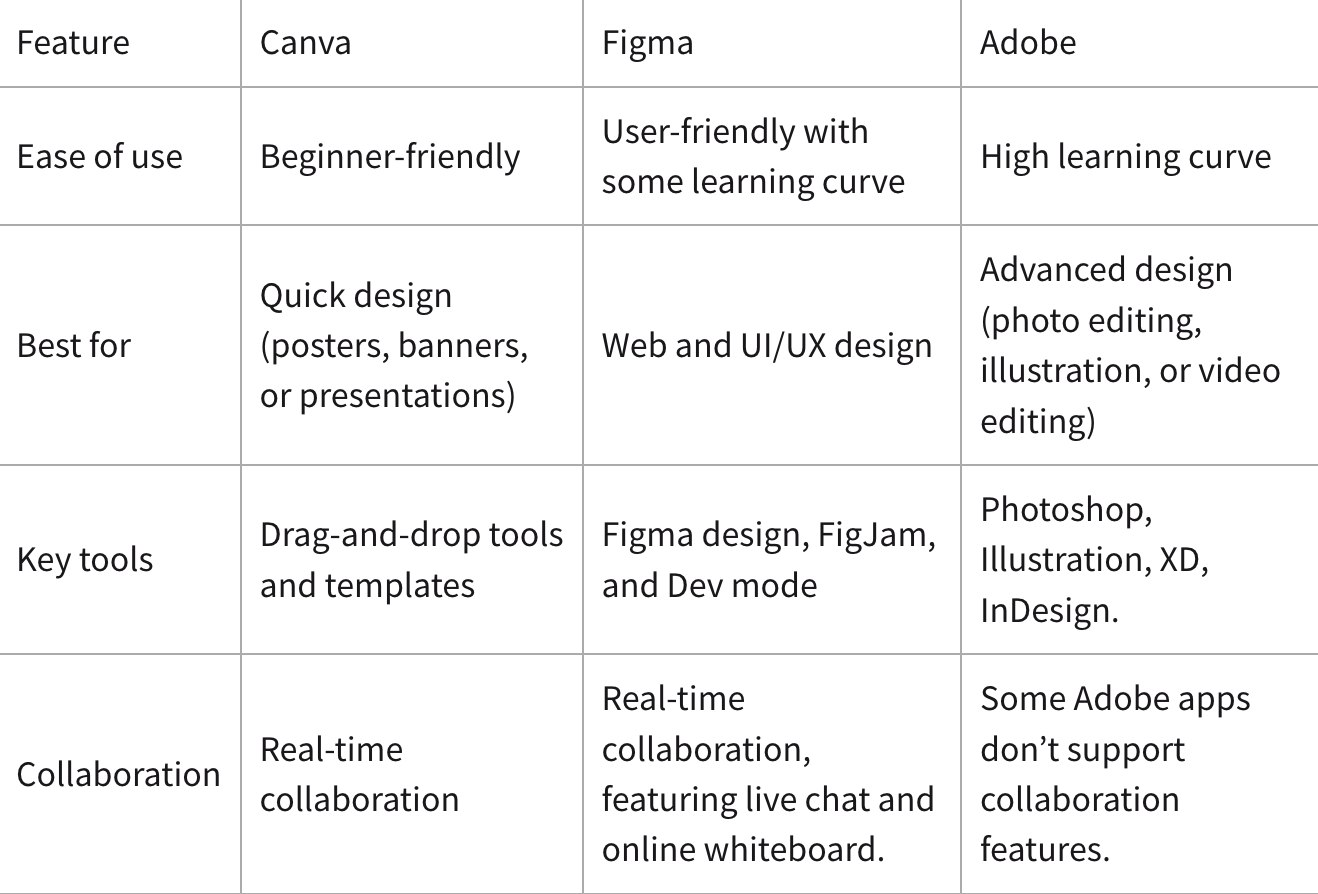

Adobe's competitive reality is divided between established productivity suites (e.g., Microsoft 365, Google Workspace) and design disruption newcomers (e.g., Canva, Figma, OpenAI tools). Adobe's moat in the past was rooted in file format control and brand allegiance. Nowadays, however, AI-first startups and hyperscalers are a credible threat with low-cost, modular, cloud-first alternatives. The $20 billion+ acquisition (later dropped following regulatory opposition) of Figma proved the threat.

But Adobe is winning the battle anew by going deep within the value chain, converging static design tools with intelligent engagement systems. GenStudio directly competes with Salesforce Marketing Cloud and Oracle CX by simplifying the creation of content, personalization, and activation in one stack. With its integration with AEP AI Assistant, it further supports real-time segmentation of customers, ingestion of data, and campaign execution, functions that incumbent players outsource by using multiple discrete tools.

On the SMB and consumer side, Adobe's freemium Express and mobile Photoshop products address Canva's head start in graphic content creation. Adobe owns the entire rendering pipeline, from ideation (Firefly) through production (Photoshop) to delivery (Acrobat, AEP). Such integrated architecture, particularly when combined with AI agents and third-party extensibility of models, gives Adobe a decided advantage in lock-in and enterprise IT compliance.

Adobe's margin protection and ARR expansion capability also outsize its closest peers. Its FY25 non-GAAP operating margin goal of 46% is unprecedented among SaaS peers of the same ARR size. Microsoft is the only peer for Adobe that shares the same level of size and margin profile. Adobe's further verticalization into marketing and media, though, confers a unique functional capability in non-office content spaces.

Source: PutraCetol

Monetization Engines and Margin Mechanics

Adobe's Q1 FY25 results validate the transition of the company to a capital-light, AI-led, subscription-driven enterprise. Revenue rose 10% YoY (11% constant currency) to $5.71 billion. Operating cash flow rose to a Q1 record of $2.48 billion and GAAP operating income to $2.16 billion with a 35% margin. Non-GAAP EPS was $5.08, up 13% YoY, against $4.14 GAAP EPS. What is most notable is the simultaneous acceleration of both ARR and returns of capital: Adobe repurchased $3.25 billion during the quarter, out of a $25 billion authorization, reflecting faith in intrinsic value over macro weakness.

Segment-level analysis uncovers monetization nuances. The Business Professionals & Consumers segment experienced 15% YoY growth in subscription revenue, outpacing the 10% increase from the Creative & Marketing Professionals segment. The divergence is a result of the ramp of low-CAC, high-LTV products such as Acrobat AI and Express, cross-distributed across web, desktop, and mobile. Education channel adoption and mobile-first use cases drove 85% YoY growth in Express student usage. Paid web and mobile Creative Cloud subscriptions increased 35% YoY, demonstrating success in the onboarding of next-gen creators via freemium funnels.

On the cost structure side, Adobe is efficient in scaling. R&D increased to $1.03 billion but stayed flat as a percent of revenue. SG&A expenses, at $1.49 billion, included spending related to AI headcount and go-to-market partnerships but were mitigated by operating leverage from the cloud subscription scale. Deferred revenue growth of $231 million, with RPO growing to $19.69 billion (+12% YoY), supports strong visibility for the future. Cash and short-term investments are at $7.44 billion, more than adequate to cover CapEx, buybacks, and future M&A.

Valuation Mismatch or Fair Premium?

On the surface, Adobe's headline multiple looks rich, an enterprise-value-to-sales (EV/S) multiple of 7.47x forward and 7.95x trailing, well above the sector median of 2.85x and 3.11x, respectively. The multiples receive a relatively poor grade (D) and superficially imply overvaluation. However, a closer forensic read, particularly when viewed against the historically high operating leverage and FCF conversion of Adobe, suggests a subtle dislocation between normalized earnings power and perceived valuation.

Adobe’s non-GAAP (TTM) P/E of 21.72x is close to the sector average of 21.57x, though 40% lower than its 5-year average of 36.25x. More illustrative is the forward (non-GAAP) P/E of 20.29x, down 8.8% from the sector average and 40% lower than its historic norm. Such differences are not a sign of structural decline at Adobe; indeed, Q1 FY25 results highlight strengthening ARR growth, AI monetization, and margin resilience. Instead, they are a temporary compression in valuation against the backdrop of SaaS derating and macroeconomic concerns.

Free cash flow-based measures validate the underappreciation. Adobe is trading at 18.75x forward P/FCF, only slightly above the 18.60x sector median but 36.66% lower than its 5-year average. The disconnect, together with a $2.48 billion operating cash flow per quarter and large buyback capacity, suggests the company is generating excellent cash at a lower-than-normal premium.

The sole red flag is a result of EV/S and Price/Sales multiples. A Price/Sales (FWD) of 7.50x, over 160% above sector medians, would be a cause for concern if Adobe did not have margin expansion or recurring revenue tailwinds. But Adobe commands >45% operating margins on non-GAAP and 90 %+ recurring revenue. The premium is reasonable, even appropriate, when put against vertical peers such as Salesforce (~30% margin, lower FCF yield) or Datadog (wider growth, narrower margins).

Source: Yahoo Finance

When we break down Adobe's valuation using a sum-of-the-parts approach and utilize conservative multiples:

- Document Cloud + Express: ~$5.5 billion implied ARR → 9–11x EV/S = $49.5 billion – $60.5 billion

- Creative Cloud: ~$12 billion ARR (est. from Q1 mix) → 13–15x EV/S = $156 billion – $180 billion

- Experience Cloud (GenStudio): ~$6 billion target FY25 rev → 8–10x EV/S = $48 billion – $60 billion

Source: ADBE Investor Presentation

Together, the enterprise value of Adobe would logically be in the $253 billion – $300 billion range. With ~433 million shares outstanding and net cash, this implies a per-share fair value of $585–$695, which suggests 42–68% above current levels of ~$412.

Thus, the market is mis-anchoring Adobe's valuation to historical revenue multiples and neglecting a multi-segment margin expansion and generative AI monetization trend. The investors purchasing at the current prices are buying a structurally advantaged, platform-levered company at a normalized multiple not seen since the 2020 technology sell-off.

Risks: Regulatory, AI Cannibalization, and Execution Complexity

Adobe's upside case is robust, though risks exist. First, regulatory attention, particularly following the breakdown of the Figma deal, can cap inorganic growth or spark antitrust barriers in particular verticals. Secondly, the danger of AI eating into Adobe's pro creative tools is genuine. With generative tools becoming increasingly commoditized, customers will swap Photoshop with lighter-weight, AI-oriented replacements. Adobe's response, integrating Firefly and launching freemium smartphone applications, depends on careful management of the pricing tiers so as not to compress margins.

Third, Adobe's wide go-to-market change (merging Express with Acrobat, GenStudio with Experience Cloud, etc.) heightens execution risk. Channel complexity, particularly with B2B and freemium motions running simultaneously, can blur the brand's focus or stretch sales organizations. In addition, the competition from the hyperscalers Microsoft and Google, both of which incorporate generative AI capabilities within their productivity packages, will become even more aggressive, particularly in the SMB and enterprise segments.

Finally, macro headwinds like reduced IT spending or slowing digital transformation would hurt top-line growth. While Adobe's diversified base insulates against cyclical factors, extended dips in advertising or creator economies would still hit ARR growth in the Creative & Marketing group.

Conclusion

Adobe's Q1 FY25 results are not just a beat, though - they are a strategic turning point. The company is de-risking its revenue streams systematically by hardwiring AI throughout user cohorts and adding new monetization levers on top through Express, Firefly, and GenStudio. With compounding ARR, operating leverage preserved, and a twin-flywheel architecture unfolding, Adobe is building the kind of high-margin, high-durability platform that can perform well in both bull and bear markets. With the competition heating up and regulatory overhang looming, Adobe's rebirth as a cognitive workflow engine merits its premium and, indeed, a re-rating.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.