Applied Materials: The Hidden Giant Powering AI

.jpg)

- Applied Materials reported Q2 FY2025 revenue of $7.1 billion, up 7% YoY, with record non-GAAP EPS of $2.39.

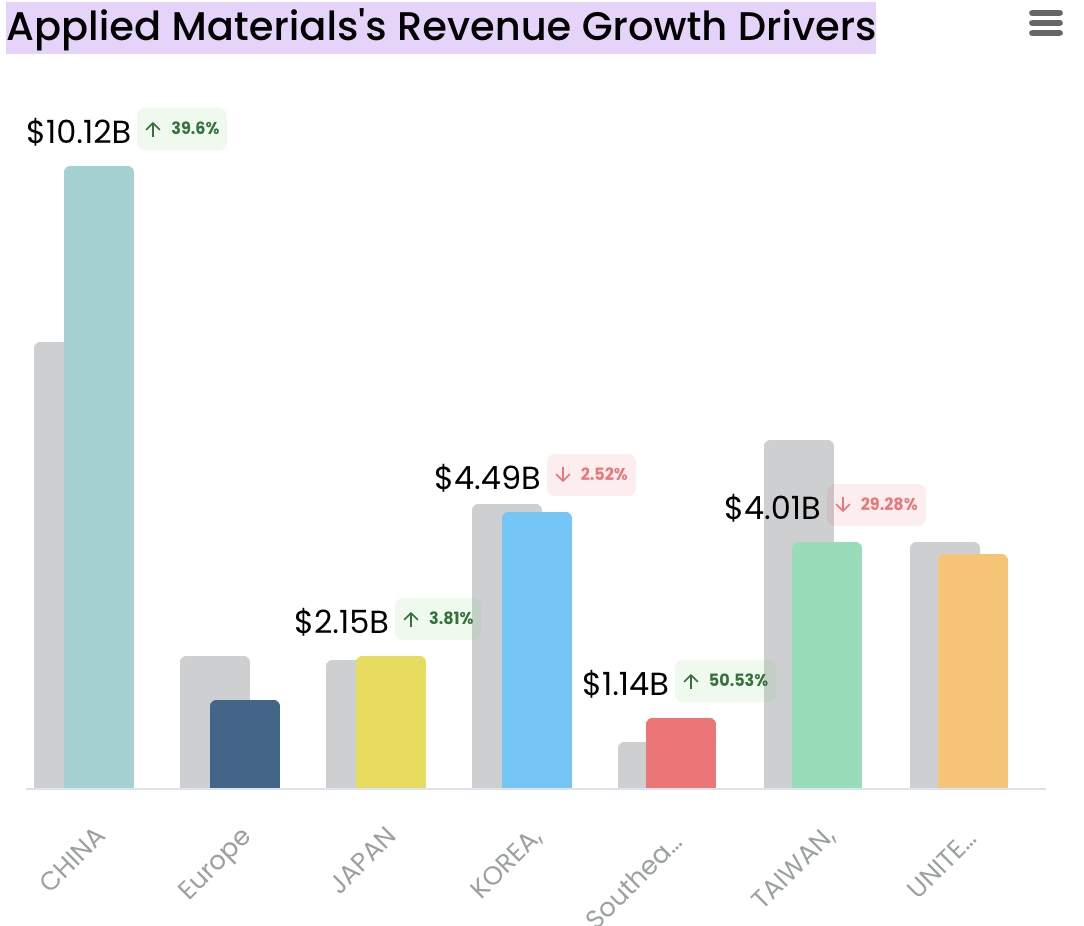

- China revenue share dropped from 43% to 25%, while Taiwan and Korea now contribute 50% of total sales.

- Over $1.2 billion in revenue generated from Sym3 Magnum since launch; recurring services revenue now exceeds $1.05 billion.

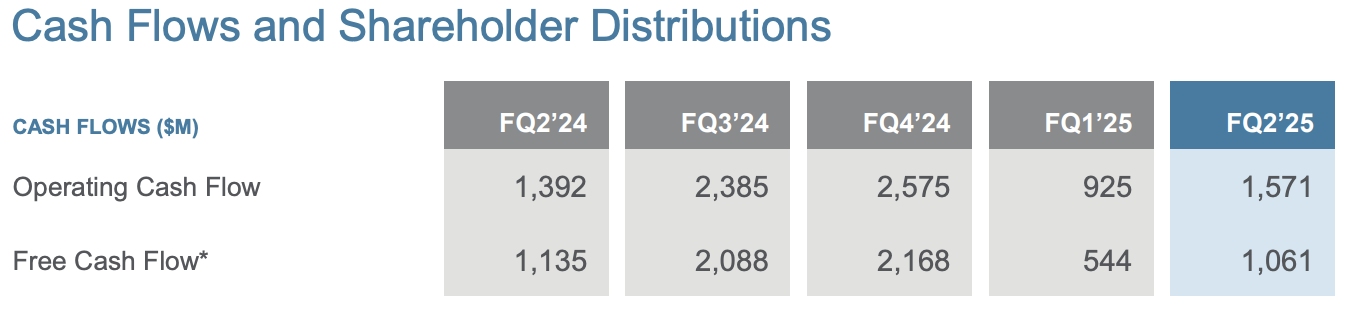

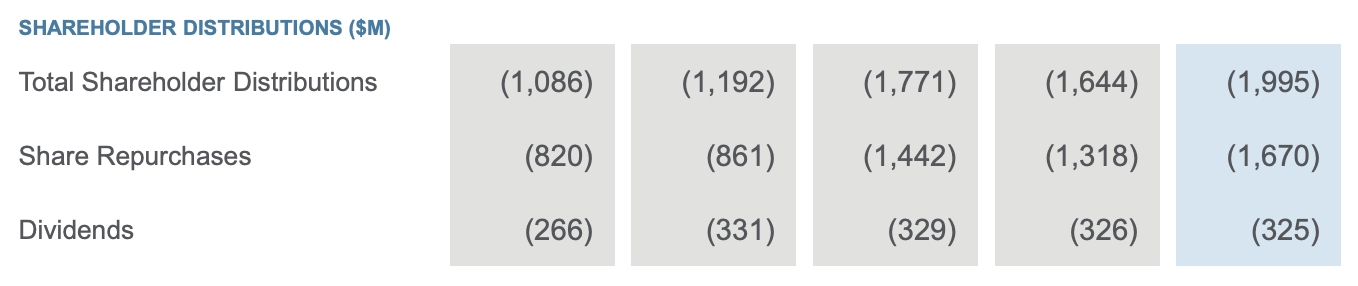

- Free cash flow hit $1.06 billion despite $510 million in EPIC investments; $1.7 billion in buybacks and $325 million in dividends.

Unlike the general perception that semiconductor spending is cyclical and now overextended, Applied Materials' (AMAT) Q2 FY2025 results provide a strong argument for structural re-rating.

The company is not only a part of the AI wave; it is woven into the very fabric of the architecture of next-gen chips, with exposure in the fastest-growing technology inflections: gate-all-around (GAA) transistors, backside power delivery (BPD), and high-bandwidth memory (HBM). Device architectures that are vital for delivering power-efficient AI computing are a long-term trend that is in the early stages of a multi-decade infrastructure buildout.

Source: PwC

Where peers are increasingly dominated by China dependence or exposure to legacy nodes, Applied has rebalanced its portfolio from trade-vulnerable geographies to leading-edge foundry-logic and DRAM markets. Indeed, China's share of revenue plunged to 25% from 43% a year ago, with Taiwan and Korea accounting for 50% of sales, despite a focus on strategic alignment with leading-edge manufacturing centers. These changes are not a short-term hedge, however. They represent a longer-term rebalancing towards where future wafer fab equipment (WFE) demand will be focused.

Source: BullFincher

The payoff is now apparent: a 7% year-over-year revenue growth to $7.1 billion, record non-GAAP EPS of $2.39 (14% increase), and the highest gross margin (49.2%) since FY2000. But more notably, Semiconductor Systems, the largest sector for the company, increased 7% year-over-year and achieved a 150 basis point margin expansion, confirming Applied’s leverage to advanced node spending.

Source: BullFincher

Moat through Compounding: from Product Breadth to Platform Supremacy

Applied Materials is well established for its expansive portfolio across deposition, etch, metrology, and inspection. However, Q2 FY2025 results highlight a move from component vendor to co-architect of technology. The firm's "high-velocity co-innovation" model, based on the EPIC platform, facilitates live R&D collaboration with customers. Such a model is materially reducing the commercialization cycles and integrating Applied further into customers' process development roadmaps.

Definitive evidence is in the $1.2 billion of revenue achieved since the February 2024 introduction of its Sym3 Magnum system, which integrates etch and deposition to cure EUV-induced line edge roughness. The second-generation Cold Field Emission eBeam system is also driving yield ramp-ups in GAA and HBM, supporting all-time highs for Applied's Process Diagnostics and Control division.

Additionally, more than two-thirds of the firm’s $1.57 billion of service revenue is now recurring subscriptions. Not only are the contracts stable, but growing in size through broad service contracts that correlate with tool complexity and install base penetration. This service flywheel, which is underappreciated in headline numbers, equates to strong margin resilience and capital-light incremental growth.

Behind the Numbers: Disciplined Capital vs. Efficient Reinvestment

On the financial side, Applied Materials is still bucking the trend. Operating margin was 30.7% non-GAAP, up 170 basis points year-over-year. Free cash flow was $1.06 billion even with a $510 million spending spike, with most of it related to EPIC development. Shareholders are still treated to aggressive yet manageable returns: $1.7 billion in buybacks and a $325 million dividend, supported by $6.2 billion in cash and a sub-1x net debt-to-EBITDA.

Source: Applied Materials, Second Quarter Fiscal 2025 Earnings Presentation

Source: Applied Materials, Second Quarter Fiscal 2025 Earnings Presentation

But what distinguishes Applied is its capital efficiency of reinvestment. Spending across research and development climbed to $893 million in the period, but overall operating expenses as a percent of revenue stayed flat because of reductions in general and administrative expenses. The capital deployment towards long-cycle projects such as EPIC confirms Applied is planting the seeds for asymmetric leverage rather than running after near-term growth.

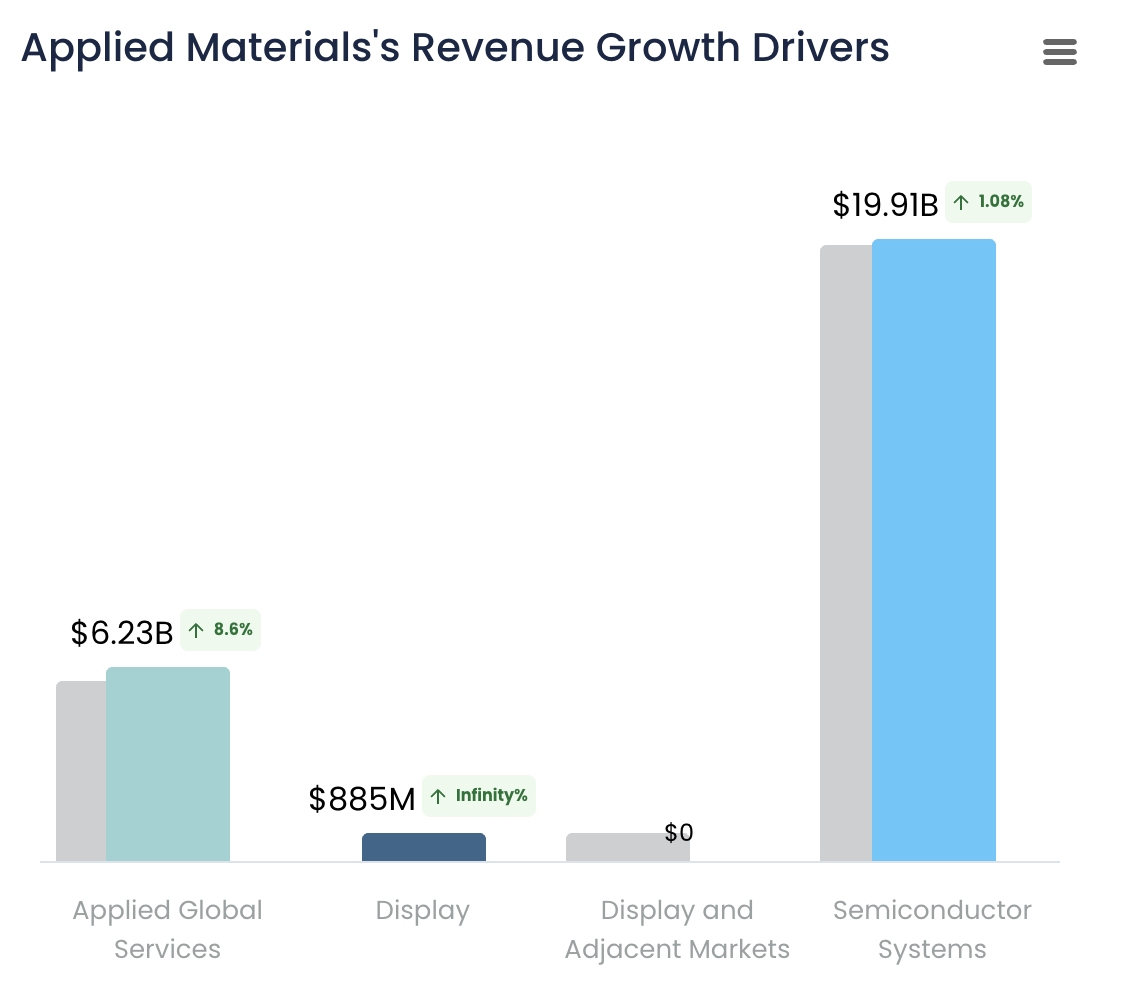

Even the Display division, which is normally a volatility factor, registered 45% year-over-year revenue growth, with operating margins increasing to 26.3% from a meager 2.8% a year earlier. Though the division is small, it demonstrates incremental operating leverage even in the non-core space.

The market is still approaching Applied Materials with a skeptical eye, giving it a forward P/E of about 19.7x and an EV/Sales multiple of about 4.6x, rates consistent with a cyclical or margin-risky company. But that analysis fails to acknowledge a number of structural dynamics at the heart of the business. To begin with, Applied is transitioning from an equipment vendor to a recurring revenue, high-margin player. More than two-thirds of its services revenue, $1.57 billion in the latest period, is based on a subscription model, with the stability akin to SaaS models for software. Such embedded monetization underpins multiple expansions.

Also, the FY2025 run rate for the company's non-GAAP EPS is above $9.50, as guided by the midpoint of the upcoming quarter’s guidance of $2.35 ± $0.20, which translates to a conservative all-year range of $9.30 to $9.70. Based on such a base, a 22x to 24x multiple for earnings, albeit lower than peers like ASML (ASML) or even Lam Research (LAM), projects a fair value of between $209 and $228 per share. If the advanced DRAM and GAA adoption momentum is sustained, or Chinese revenue starts to recover even to a partial degree, such estimates are likely to be proved too conservative.

Source: Seeking Alpha

On a free cash flow basis, the tale is just as compelling. With Q2 FCF of $1.06 billion and trailing twelve-month FCF near $7 billion, Applied trades at a FCF yield of nearly 4.8%, which is the kind reserved for low-growth industrials. The disconnect is particularly surprising when you factor in the firm's CapEx discipline (only 7.2% of each quarter's revenue) and commitment to returning 80–100% of FCF to the shareholder base by way of dividends and buybacks. The firm still has $15.9 billion of repurchase authorization remaining, which sets a meaningful floor under the stock.

In contrast, ASML sells for more than 34x forward earnings with less near-term margin expansion, while Lam Research, with more concentrated exposure to the memory space, sells at about 23x. Applied’s blended exposure to logic and DRAM, as well as its differentiated services flywheel and architecture leverage, justify a rerating in the 24x–26x level under a positive case. The latter would translate to a share price of more than $240 if macro conditions continue to be constructive and AI-driven fab demand accelerates in the back half of 2025.

Steering Through the Risk Matrix: Structural Shocks and Executional Clarity

The company is aided by secular growth in AI, advanced packaging, and semiconductor scaling. However, a number of risks can derail the trend.

Geopolitical risk is the most prominent. Even with decreasing China exposure from 43% to 25% of total revenue from year to year, Applied still experiences trade headwinds related to the control of exports and rising U.S.-China tensions. Limitations placed on DRAM and mature logic sales into China, particularly under revised licensing arrangements, may suppress growth in the Applied Global Services (AGS) division, which is reliant on monetization from the mature-node install base. In the worst-case scenario, additional export restraints can propagate to postponed orders or necessitate the speeding up of insourcing initiatives.

Another group of risks is customer concentration and CapEx cyclicality. With leading-edge investments led by leading foundries and memory suppliers, any reduction in hyperscaler or mobile SoC demand can cause delays in fab expansions. With GAA and BPD adoption still in the early innings, product development and adoption timing mismatches can affect the revenue recognition curve. While management's approach of coproducing solutions via the EPIC platform lowers the probability of this occurring, delays in execution are a danger.

On the financial side, gross margin robustness depends on a positive product mix. If the demand swings back in the direction of legacy ICAPS nodes (applied in automotive, Internet of Things, and power), margins can contract slightly. This is especially noteworthy considering the company's previous prominence in China, a targeted ICAPS customer base, which might not recover in the near future.

Technologically, Applied's heavy dependence on advanced logic and DRAM ensures its success is linked with the ramp of leading-edge products. Failure of defect metrology tools, delays in the adoption of Sym3 Magnum, or switching by customers to in-house or other solutions would damage competitive positions. Further, when cold field emission and AIx-driven diagnostics pick up traction, Applied needs to keep up with the competitors' innovation cycles. And then there is the latent danger of valuation complacency.

Should wider markets re-rate lower, or if sector-wide opinion moves against semiconductors, even Applied's structural strengths might not be immune from near-term drawdown. Still, with a strong balance sheet, good liquidity, and a capital return strategy based on long-cycle planning, Applied is in a stronger position than most to ride out transient turmoil.

Conclusion

Key Takeaway: Applied Materials is mispriced structurally for AI architecture inflections. With operating leverage, velocity of R&D, and compounding of services all converging, the stock is set for a multi-year re-rating. Target price: $209–$228. High-conviction buy on the decline.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.