Behind Nvidia’s $44B Q1 Quarter

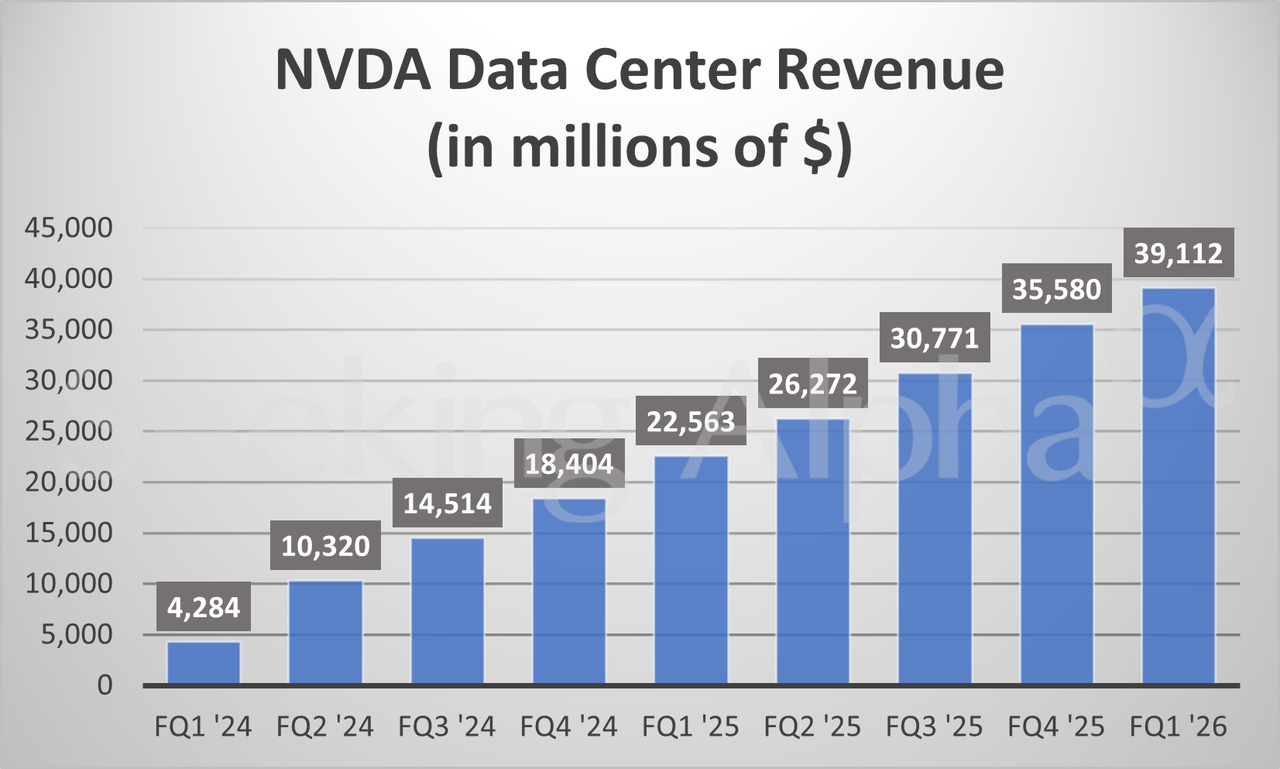

- NVIDIA reported $44.1 billion in Q1 FY2026 revenue, with Data Center contributing $39.1 billion, up 73% year-over-year.

- Gross margin declined to 60.5% GAAP and 71.3% adjusted, impacted by a $4.5 billion H20 inventory write-down.

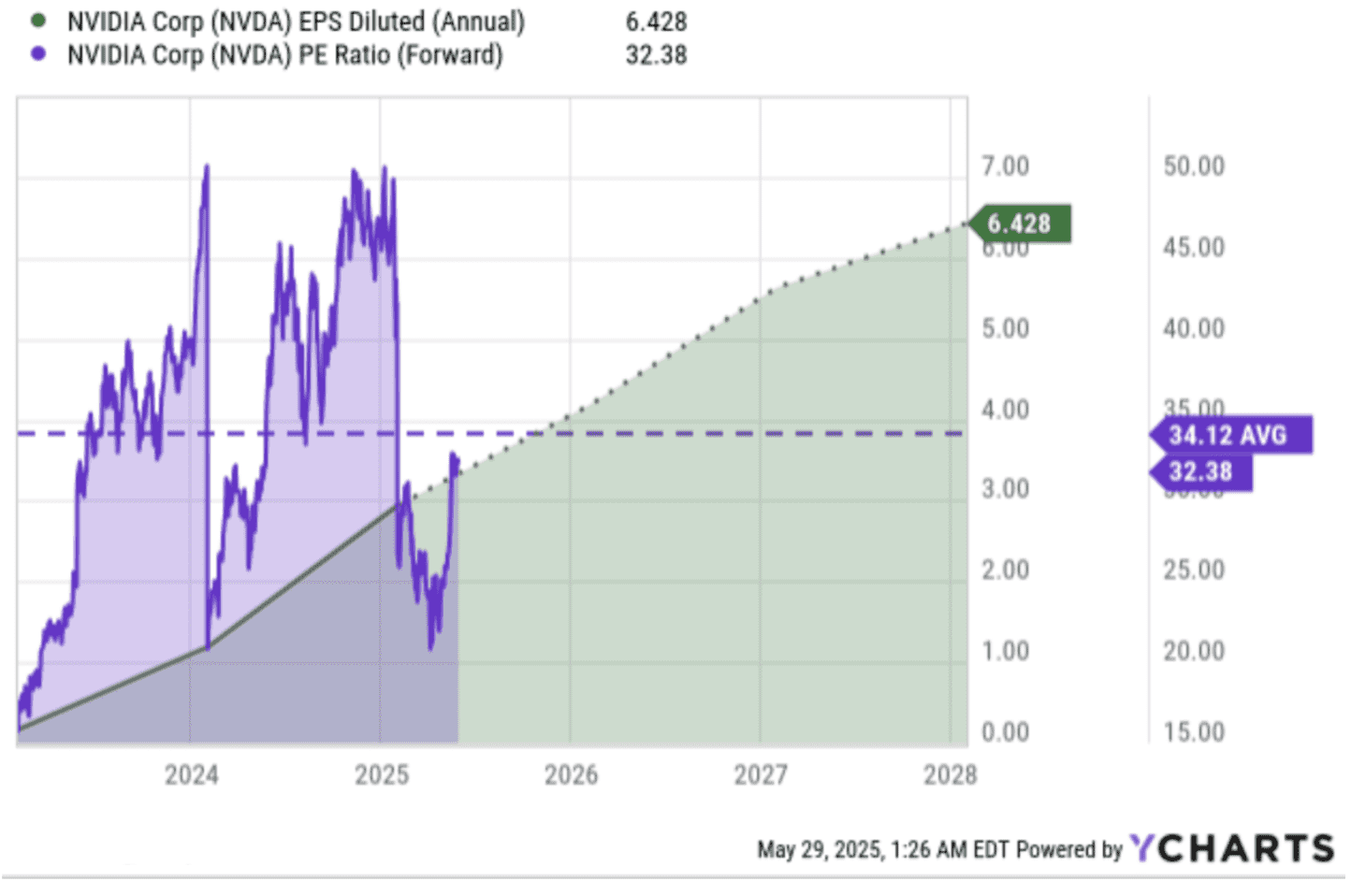

- Forward estimates show EPS rising from $4.16 in FY2026 to $5.63 in FY2027, a 35% year-over-year growth.

- Revenue is projected to grow from $199.37 billion in FY2026 to $247.03 billion in FY2027, a 24% increase.

- NVIDIA’s EV/FCF is 51.56, P/S 25.07, and P/B 41.81, indicating valuation risk despite PEG below 1.0.

TradingeKey - Nvidia (NVDA) just posted a jaw-dropping $44.1 billion in Q1 FY2026 revenue, driven by a 73% YoY surge in its Data Center segment. But beneath the surface of this AI-fueled momentum lies a more complex reality: margin erosion, geopolitical overhangs, and valuation multiples that defy gravity.

A $4.5 billion inventory write-down and an $8 billion China export loss expose cracks in the growth narrative. With forward EPS projected to grow 35% and revenue 24% by FY2027, NVIDIA’s fundamentals remain compelling, but investors must now weigh platform strength against capital intensity and the unrelenting expectations embedded in its trillion-dollar valuation.

Blackwell Blitz: The Hardware Supercycle Exists, But It's Mispriced

The company’s rapid growth is fueled by a cascade of AI demand unlike anything in the history of computing. The Blackwell architecture ramp added almost 70% of the $39.1 billion in Q1’s Data Center revenue. As the company is shipping its flagship NVL72 racks to hyperscale (i.e., the ramping by Microsoft to hundreds of thousands of GB200s), the company is shipping compute infrastructure more rapidly than it can manufacture. Jensen Huang’s comments emphasized that every GB200 rack, which is packed with 72 GPUs and weighs almost 2 tons, is essentially a mobile AI factory.

Source: Seeking Alpha

Yet the trend in this hardware explosion's margin profile is unfavorable. Even with the revenue of $44.1 billion, GAAP gross margin declined to 60.5% from 78.4% last year. Even normalizing for the one-time charge of H20 of $4.5 billion, the 71.3% gross margin was still meaningfully lower than in the past. It is not fully explained by China-related headwinds but also includes the increase in complexity and cost of rack-scale installations and the NVLink architecture.

In addition, as inference demand booms, especially thanks to reasoning agents such as DeepSeek-R1, there is more capital intensity. Nvidia’s cash inventories exploded to $11.3 billion with $29.8 billion in forward purchase commitments. CapEx light days are no more. This change undermines the tale of capital efficiency that has for so long supported Nvidia’s premium multiple.

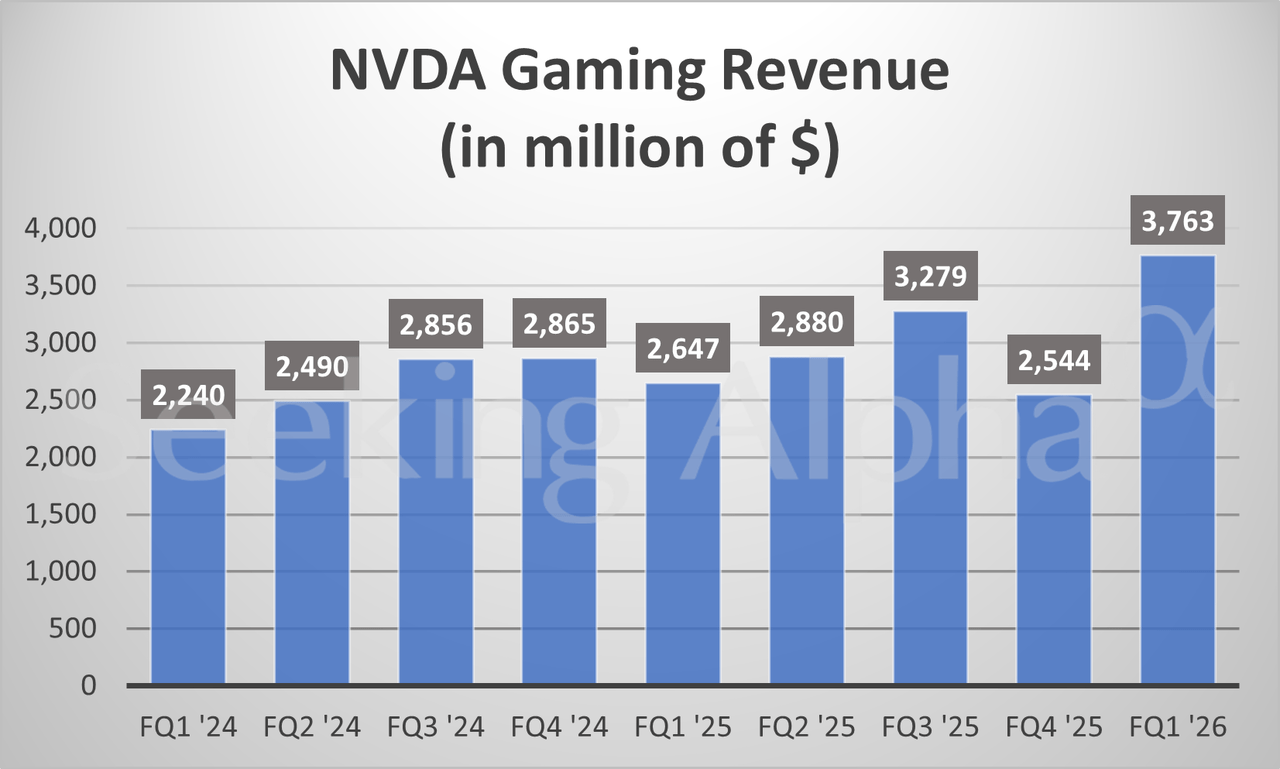

Gaming and Other Segments: Strength Beyond the Data Center

While Nvidia's Data Center segment gets the lion's share of the limelight, its Gaming and other segments achieved quietly impressive growth in Q1 FY2026, reaffirming the company's multi-pronged AI-driven monetization strategy. Gaming revenue hit an all-time high of $3.76 billion, up 48% from last quarter and 42% from the corresponding quarter last year, driven by widespread adoption of the new GeForce RTX 5060 and 5060 Ti GPUs, powered by the Blackwell architecture. Equipped with AI technologies such as DLSS 4 and frame generation, these GPUs not only enrich gaming experiences but also broaden Nvidia's reach in AI-powered PCs.

Source: Seeking Alpha

Professional Visualization revenue remained at $509 million, growing 19% from the same quarter last year, as the demand for AI workstations and Omniverse-enabled industrial simulation continued to increase in markets such as manufacturing and robotics. Automotive revenue was up 72% from last year at $567 million, driven by the global rollout of Nvidia DRIVE and partnerships with original equipment manufacturers such as Mercedes-Benz and GM. Omniverse and Isaac platforms are also driving innovation in humanoid robots and synthetic data generation.

These segments confirm Nvidia's expansion outside of silicon, making vertical-specific software, simulation, and edge-AI compounding drivers of revenue. As AI infuses itself throughout gaming, autonomous robotics, and more, Nvidia's non-Data Center segments offer important diversification and optionality, solidifying its position as a full-stack AI platform company.

Export Shock: The Unseen Consequences of China’s $50B Wall

Perhaps the least appreciated structural risk is the geopolitical drag from the effective prohibition of Nvidia’s H20 chips in China. It was responsible for suppressing the bottom line in Q1 by $4.5 billion in charges and $2.5 billion in lost shipments. Management portrayed this as a one-timer, but the Q2 guidance already suggests another $8 billion hit in revenue from continued restrictions.

It is not merely a revenue issue, but a sign that US platforms can expect to face more AI decoupling. Jensen Huang conceded that additional SKU compliance reductions are almost impossible to achieve, and Nvidia is left with "limited options" in China. The lost TAM of ~$50 billion is also unlikely to be recaptured, with China ramping up the development of its home-grown accelerators and migrating to Huawei Ascend and Biren platforms.

At the same time, this decoupling creates downstream risk to Nvidia's scale advantage in its supply chain. In the absence of China's volume foundation, the cost economics of NVLink72 and Spectrum-X infrastructure would collapse over time, diminishing unit cost efficiencies and hindering more extensive deployment in cost-conscious geographies.

Source: Gurufocus

Outlook and Future Direction: Sovereign AI, Agentic Workflows, and the Blackwell Horizon

In the future, Nvidia's strategic trajectory is increasingly divided between global growth in AI infrastructure and mounting pressure to demonstrate operating leverage from a wider product pipeline. At face value, the company's Q2 FY26 guide of $45 billion in revenue (+2% quarter-over-quarter) signals on-going strength, but with obvious headwinds: specifically, the full exclusion of H20-related China revenue (~$8 billion impact), gross margin pressure from ramping up Blackwell shipping, and a growing R&D cost associated with next-gen systems such as GB300 and GR00T humanoid AI designs.

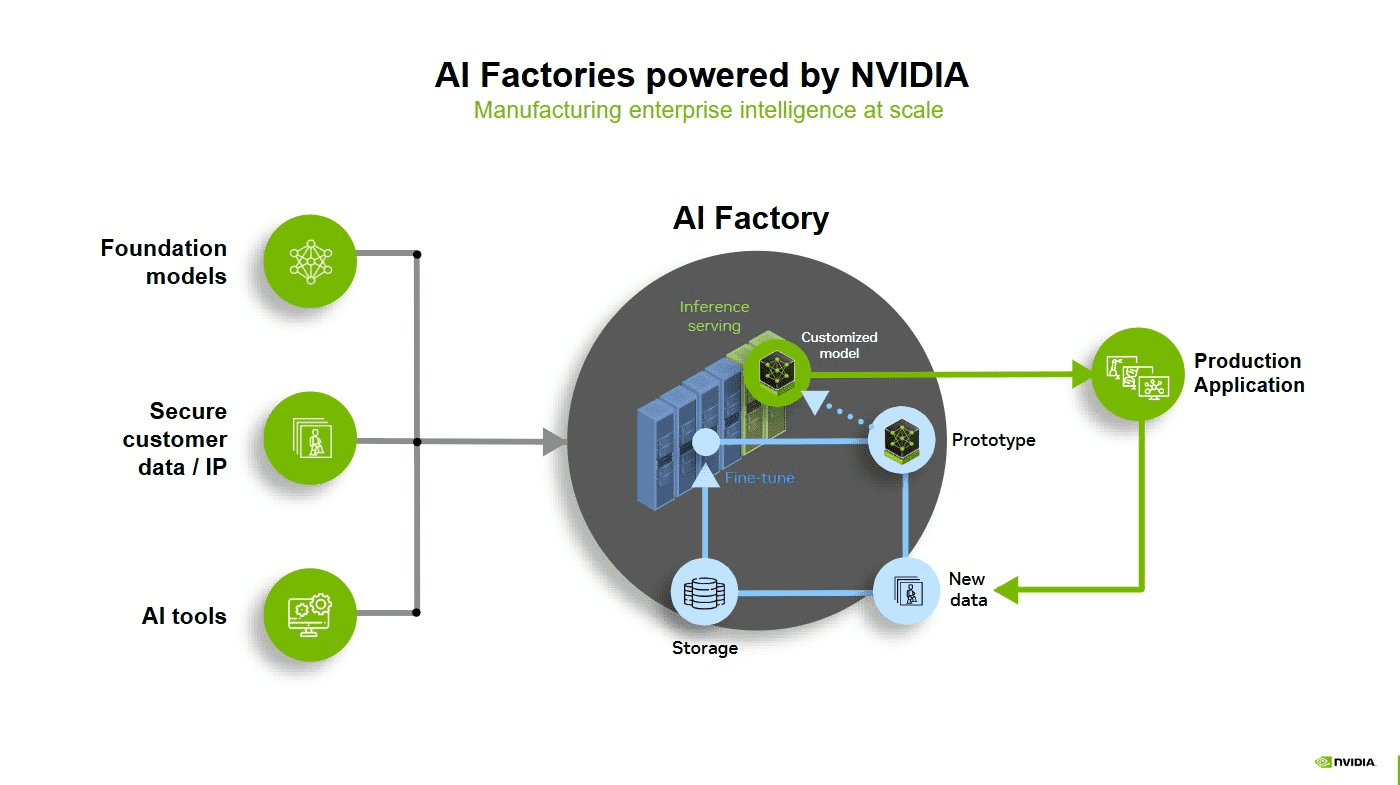

What is different this time for Nvidia's growth trajectory is not only the cadence of the products with GB300 sampling already in the works but also the infrastructure of global AI demand. Jensen Huang confirmed that more than 100 AI factories are in the air, and the company is building out infrastructure to enable sovereign deployments in Taiwan, Sweden, Saudi Arabia, and the UAE. It is not a one-off series of isolated bursts of CapEx, but a multi-year, border-crossing AI reindustrialization effort, akin to the construction of electricity and the internet, as Huang describes.

Source: Nvidia

Source: Nvidia

But these sovereign initiatives have a different financial profile. In contrast to hyperscaler expansions that seed compute against recurring SaaS revenue streams, sovereign and industrial deployments of AI can be discrete and cash-starved. For instance, Nvidia may enjoy good visibility of GB200 and GB300 rack sales, but the conversion of these block deals to recurring software revenue, through channels such as NeMo, Omniverse, and DGX Cloud, is still in its infancy. If Nvidia fails to integrate its software stack into these infrastructures, it risks becoming commoditized off of open models and local software ecosystems.

The other growth driver, enterprise AI, is still in its infancy but full of potential. Its RTX Pro AI Servers and DGX Spark/Station offerings are pushing Nvidia's stack out to on-prem, an important market as data localisation and compliance issues spread. But this strategy puts Nvidia in direct conflict with the established enterprise IT players (Dell, HPE, Lenovo), requiring not only technological supremacy but also distribution partnerships and services integration as well. Success in this segment will ride on Nvidia being able to extend its hyperscaler success to a channel-enabled enterprise market.

Margin recovery from a capital markets point of view will also be important to follow. Management projects to achieve mid-70% gross margins in the fiscal-year end, driven by essentially ramp efficiency in Blackwell. This would involve closer management of inventory (~$11.3B as of Q1) and better yield curves in NVLink-enabled systems. But the mix-shift to full-stack deployments, though strategic, can push this trend, particularly if input prices and geopolitical sourcing concerns (e.g., Taiwan, Arizona plant dependencies) continue. In the background, macro and regulatory risks overhang. US policy changes, notably the re-imposition of new or continued tightening of AI diffusion regulations, potentially disrupt the Nvidia roadmap.

The revoking of the AI diffusion rule has also paved the way to more extensive US-Middle Eastern and European AI alignment, as a tailwind but one that hinges on unstable diplomacy and economic partnerships. In short, Nvidia’s prospects are still essentially robust but structurally complicated. It is not only shipping GPUs anymore but is defining the AI operating system of the global economy. But with that comes exposure: sovereign dependence, geopolitical uncertainty, and the unrelenting demands of a trillion-dollar valuation club.

Valuation: Discounted by Misunderstanding, Not by Reality

Nvidia’s valuation sits at the crossroads of extraordinary platform dominance and increasingly strained traditional metrics. While PEG ratios (GAAP forward at 0.31 and Non-GAAP forward at 0.94) suggest undervaluation relative to earnings growth, nearly every other multiple, EV/Sales (25.07), EV/EBITDA (39.27), P/Book (41.81), and P/FCF (32.93), reflects a premium rarely sustained in the semiconductor industry.

This divergence stems from the market pricing Nvidia not as a cyclical hardware vendor but as a sovereign-grade AI infrastructure platform. Yet that assumption embeds significant duration and terminal value risk. Unlike software peers with sticky recurring revenue, Nvidia’s hardware revenue remains tied to CapEx cycles and competitive innovation curves. Its valuation premium implies that Blackwell, GB300, and AI factory deployments must not only scale but achieve superior operating leverage amidst intensifying geopolitical and cost pressures.

Critically, the company’s vertical integration, from CUDA software to DGX systems, does warrant a premium, but not without limits. Investors betting on Nvidia as the “AI utility layer” are effectively underwriting a structural transformation: from chipmaker to orchestrator of global AI compute.

That thesis, however, is under pressure. The $8 billion H20 export hit, ballooning purchase obligations ($29.8 billion), and rising inventory levels ($11.3 billion) underscore the fragility of the current demand-supply equilibrium. Free cash flow growth is impressive, but with trailing EV/CF at 51.56, the market is already pricing in near-flawless execution. Valuation resilience now hinges on Nvidia successfully monetizing its platform layers, NeMo, Omniverse, Spectrum-X, into durable, software-like revenue. Without that shift, the current multiple stack reflects risk, not redundancy.

Nvidia’s forward valuation, while optically rich, becomes more grounded when contextualized by its hypergrowth trajectory. For FY2026 (ending January 2026), consensus estimates project EPS of $4.16 and revenue of $199.37 billion, translating to a forward P/E of 32.55 and a forward P/S of 16.57. These figures tighten significantly into FY2027, with EPS forecast to rise 35% to $5.63 and revenue up 24% to $247.03 billion, reducing the P/E to 24.07 and P/S to 13.38. This steep earnings ramp, supported by inference-driven AI demand and sovereign infrastructure expansion, validates a forward PEG ratio below 1.0, typically considered undervalued for hyper-growth tech.

Critically, Nvidia’s earnings CAGR from FY2026 to FY2027 sits above 30%, while revenue CAGR is ~22%, suggesting margin expansion via scale and higher software monetization. This justifies a P/E in the high-30s range, especially given Nvidia’s free cash flow dominance and unmatched positioning across the AI infrastructure stack.

Source: Ycharts

Conclusion

Nvidia's FY26 Q1 results reaffirmed its leadership in AI infrastructure, with revenue of $44.1B and inference demand exploding. Margin pressures, geopolitical uncertainties, and valuation extremes however point to increasing fragility in the background. So while sovereign AI and enterprise adoption create long-term potential, the China ban and the surge in inventories indicate near-term threats. Investors have to balance platform strength with the pull of financial gravity as expectations of infinite perfection tighten across the company.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.