Musk’s Next Ambition: Building a Space-Based AI Data Center

AI Podcast

SpaceX is reportedly seeking a $1.5 trillion valuation in a new funding round to support Elon Musk's vision of orbital data centers for AI processing. This initiative, potentially linked to Project "Heart of the Galaxy," leverages Starlink's Gen-3 satellites, benefiting from space's continuous sunlight and natural cooling. Google, Amazon, and OpenAI are also investing in similar space-based AI infrastructure. While physically feasible with advantages in power and cooling, high launch costs and engineering challenges remain. SpaceX's strong cash flow from launch services and Starlink fuels these capital-intensive ambitions, aiming for faster expansion than internal funding allows.

TradingKey - Last week, Bloomberg reported that Elon Musk’s SpaceX may soon seek a new funding round based on a staggering $1.5 trillion valuation—potentially raising over $30 billion in fresh capital. The announcement reignited interest in the entire “new space” sector and raised a question: why now?

Musk has long resisted the idea of taking SpaceX public. After the Tesla take-private drama and the resulting SEC penalties (which cost him the chairmanship), he’s been wary of public market entanglements. But something’s changed—and fast.

According to Eric Berger, a senior space writer at Ars Technica, that “something” may be Musk’s vision of a space-based AI future. Berger summarized his thesis in an article and tweet on X—and an hour later, Musk replied directly: “As always, Eric is accurate.”

The Sky Isn’t the Limit—The Data Center Is Going Up

Musk now publicly says he plans to use SpaceX’s Gen-3 Starlink satellites to build orbital data centers—powered by solar energy and optimized for AI processing. This effort is reportedly tied to a new initiative called Project “Heart of the Galaxy,” intended to integrate the capabilities of SpaceX, Tesla, and xAI into a unified vision for deep-space infrastructure.

As Musk explained that as computing clusters scale further, the combined demands on electricity and cooling will soon outpace what Earth-based infrastructure can handle.

In space, these constraints change. He noted that sunlight is continuous, eliminating the need for batteries; solar panels can also be made more cheaply, since no glass or framing is required. Cooling, he added, comes naturally in the vacuum through radiative heat dissipation.

He’s not alone in this bet.

On November 4, Google (GOOG) announced Project Suncatcher—aimed at launching two prototype satellites in early 2027 that carry its in-house TPU AI chips, in partnership with satellite firm Planet Labs. CEO Sundar Pichai said initial tests show the chips can survive low-Earth orbit’s radiation.

Amazon founder Jeff Bezos has also predicted the arrival of gigawatt-scale data centers in space within a decade. Startups like Starcloud have already launched prototype Nvidia-GPU-equipped satellites.

Even OpenAI reportedly explored partnering with or acquiring a rocket company earlier this year. Sam Altman has long believed that AI’s boundless computational appetite will eventually require orbital infrastructure—especially as its environmental footprint on Earth grows.

Elon Musk’s stated ambition has brought new visibility—and credibility—to the niche but rapidly expanding field of orbital data infrastructure. Wall Street is now paying attention.

Morgan Stanley and Deutsche Bank have both published research this month on the feasibility of space-based AI clusters. Analysts point to several structural advantages:

1) Solar irradiance in orbit is ~40% higher than on Earth, allowing for continuous 24/7 generation; 2)Vacuum cooling enables passive radiative heat management (critical for AI workloads); 3) Optical laser interlinks could deliver speeds up to 40% faster than terrestrial fiber.

While the physics are favorable, the engineering remains brutal. Chips in orbit face radiation bombardment that shortens lifespan. Thermal dissipation is challenging in an enclosed space. Hardware must meet “space-grade” standards, adding cost and weight.

Launch costs remain painfully high. At current prices, orbital data centers are still economically unviable without subsidies or massive tech breakthroughs.

SpaceX’s Cash Flow Is Strong—So Why Raise Capital?

Estimates suggest SpaceX could generate $22–24 billion in revenue next year—roughly on par with NASA’s annual budget.

The company’s top-line is powered by two engines: Falcon-based launch services and the growing Starlink satellite broadband division.

While its reusable launch system lowers cost-per-launch, Musk has made clear: by 2026, less than 5% of revenue will come from NASA contracts. The future lies in Starlink.

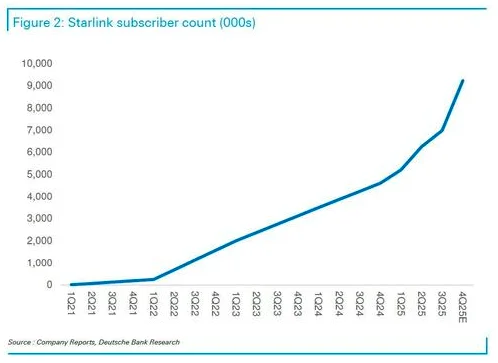

Starlink uses SpaceX rockets to deploy a low-Earth orbital constellation and deliver high-speed satellite internet. Deutsche Bank believes Starlink will cross 9 million users by the end of 2025—doubling year over year.

Even though SpaceX has consistently run positive free cash flow and boasts far higher capital efficiency than any public space agency, its ambitions require scale. Resources are being poured relentlessly into: acquiring spectrum EchoStar rights, scaling Starship for lower-cost launch, expanding global Starlink operations, and prototyping orbit-grade compute platforms. Each initiative is capital-intensive, and SpaceX wants to move faster than internal funding allows.

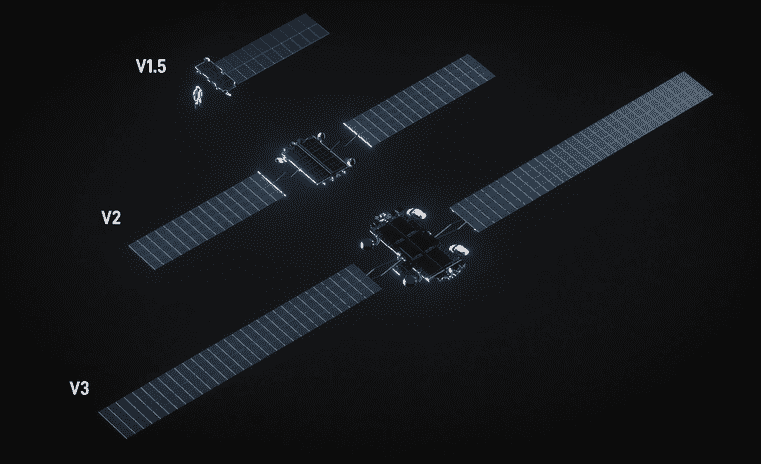

Loading the Next Stage: Starlink v3 Satellites

At the most tactical level, Musk’s next goal is upgrading the Starlink satellite fleet.

Today’s Starlink v2 “mini” satellites support maximum downlink speeds of ~100 Gbps. The upcoming v3 series is set to increase that tenfold—up to 1 Tbps—equipped with high-speed optical laser links.

The leap isn’t unprecedented in capacity—but on a mass-deployment scale, it is unmatched.

SpaceX plans to launch 60 v3 satellites at a time aboard its Starship system as early as 2026, with testing of satellite separation hardware already underway.

Unlike prior generations optimized for communications alone, the new v3 units are being engineered as compute-capable infrastructure—fitted with larger solar arrays, edge inferencing modules, enhanced thermal controls, and modular “drop-in” GPU/ASIC housings.

Alphabet’s Stake Rises with the Rocket

SpaceX’s rise doesn’t just benefit Musk. It significantly boosts Alphabet too.

Google isn’t just an AI company—it’s also SpaceX’s second-largest equity holder. This year, Alphabet disclosed over $10 billion in “unlisted equity gains,” most of which the market believes came from SpaceX revaluation.

Meanwhile, Google Cloud has signed contracts to provide computing, networking, and ground infrastructure for Starlink’s enterprise products.

Google is doubling down on space—both as a compute frontier and an imagery/data business. Project Suncatcher builds on this thesis. So does its continued collaboration with Planet Labs and its reliance on SpaceX to deploy proprietary satellites.

Alphabet’s strategy hedges competition. Whether SpaceX dominates or the broader space ecosystem expands, Google wins either way.

The Ripple Effects Are Already Here

News of a potential SpaceX IPO has lifted the entire space equity complex—but it’s not just that.

Investors are waking up to the broader monetization roadmap of commercial aerospace. SpaceX has reached scale and is proving margin viability in both launch and telecom. Now smaller firms in the ecosystem are being bid up as “underpriced beneficiaries” of the same demand curve—including satellite manufacturers and niche ground services.

Meanwhile, big tech’s real commitment to orbital AI—backed by concrete satellite deployments from Google, and reusable rocket platforms like Stoke Space’s Nova (set for 2026)—has shifted the imagination frontier again.

This is no longer just about optics. It’s about architecture economics. Laser interconnects, zero-latency cooling, orbital energy.

SpaceX is also on pace for over 100 U.S. rocket launches in 2025. Falcon 9 reuse is nearing 100%. Starship test cadence is accelerating. Collectively, this is crushing the cost floor—and validating the case for reusable launch as an industrial standard.

The policy backdrop adds fuel. A second Trump administration would likely favor expanded defense spending and space infrastructure procurement—where SpaceX and Rocket Lab (RKLB) are already active bidders for direct space-to-space freight contracts under DOD partnerships.

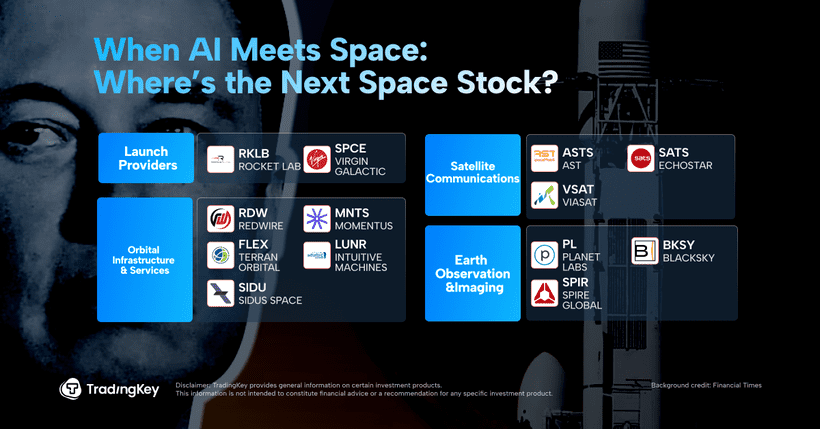

How the Market Is Segmenting the Opportunity

“New Space” is no longer a concept—it’s a cross-sector thematic with real equity candidates. Here are a few:

Launch providers

• Rocket Lab (RKLB): The world’s busiest small sat launcher, 18 successful launches in 2025

• Virgin Galactic (SPCE): Commercial space tourism leader, Delta-class ship re-launching 2026

Orbital infrastructure & services

• Redwire (RDW): Supplies solar panels and robotic limbs for SpaceX and Blue Origin

• Momentus (MNTS): “Space tug” systems moving satellites into position

• Terran Orbital: Frequent contractor to U.S. defense for smallsat production

• Intuitive Machines (LUNR): First private entrant into lunar south pole missions

• Sidus Space (SIDU): Edge-AI hardware and lunar infrastructure tooling

Satellite communications

• AST SpaceMobile (ASTS): Direct-to-smartphone satellite network, in deals with AT&T and Vodafone

• EchoStar (SATS): Traditional satellite internet firm

• Iridium (IRDM): Global satellite phone + IoT coverage network

• Viasat (VSAT): Leading aviation WiFi and defense-link provider

Earth observation & imaging

• Planet Labs (PL): Daily Earth imaging partner, ~10% owned by Alphabet

• BlackSky (BKSY): Real-time geospatial intelligence with high revisit rate

• Spire Global (SPIR): Space-based weather, ocean, and climate platform

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.