Enphase's Rebound Starts in Silence

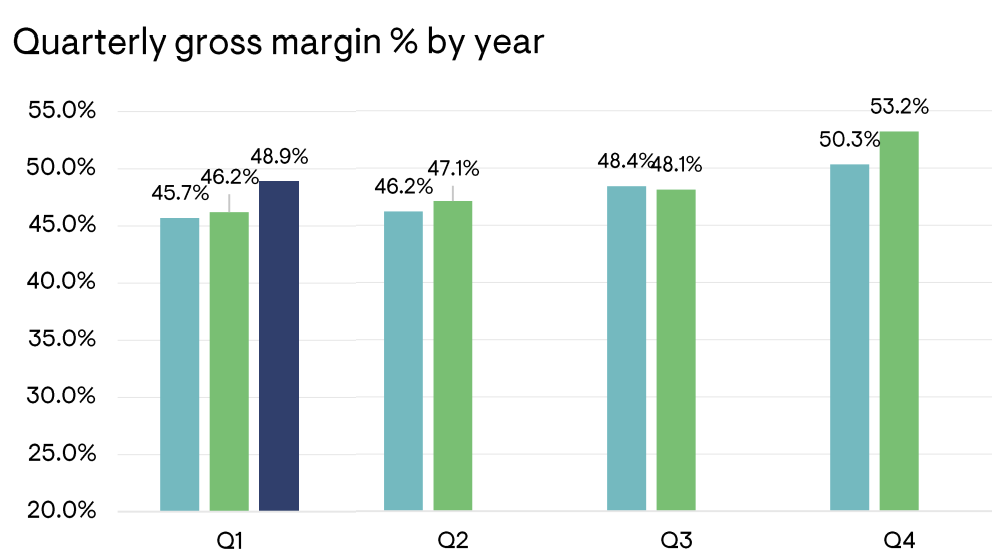

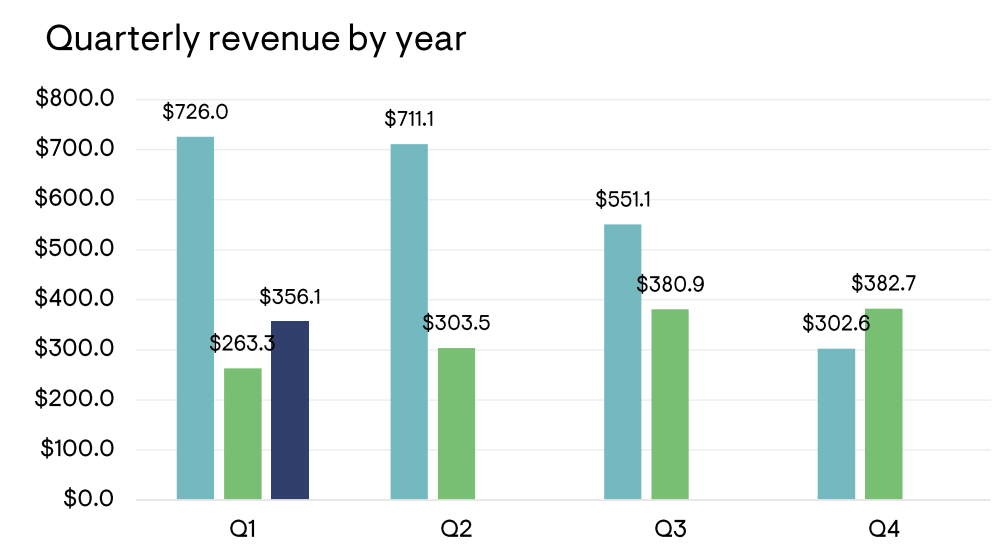

- Revenue dropped 72% YoY to $1.33 billion, but gross margins held firm at 47.3% GAAP and 48.9% non-GAAP with IRA credits.

- Generated $480 million in free cash flow and ended 2024 with $1.72 billion in cash, highlighting capital discipline amid contraction.

- Product upgrades (IQ9, Battery 10C) and new markets (Balcony Solar) support future ASP growth and platform stickiness.

- Valuation reset with P/E 19.7x, EV/EBITDA 14.3x, with a PEG of 0.97 and bull case upside to $100–$120 per share.

TradingKey - Enphase Energy (ENPH) kicked off 2025 with a battered stock price and an overextended storyline. What ensued was not a meltdown, but a measured, strategic pullback. While the residential solar market was undergoing a ruthless decline, Enphase saw revenues decline 72% YoY to $1.33 billion. That steep decline was not a consequence of market-share erosion or business misexecution. It was a strategic pullback to align with softened demand and eliminate inflated channel balances.

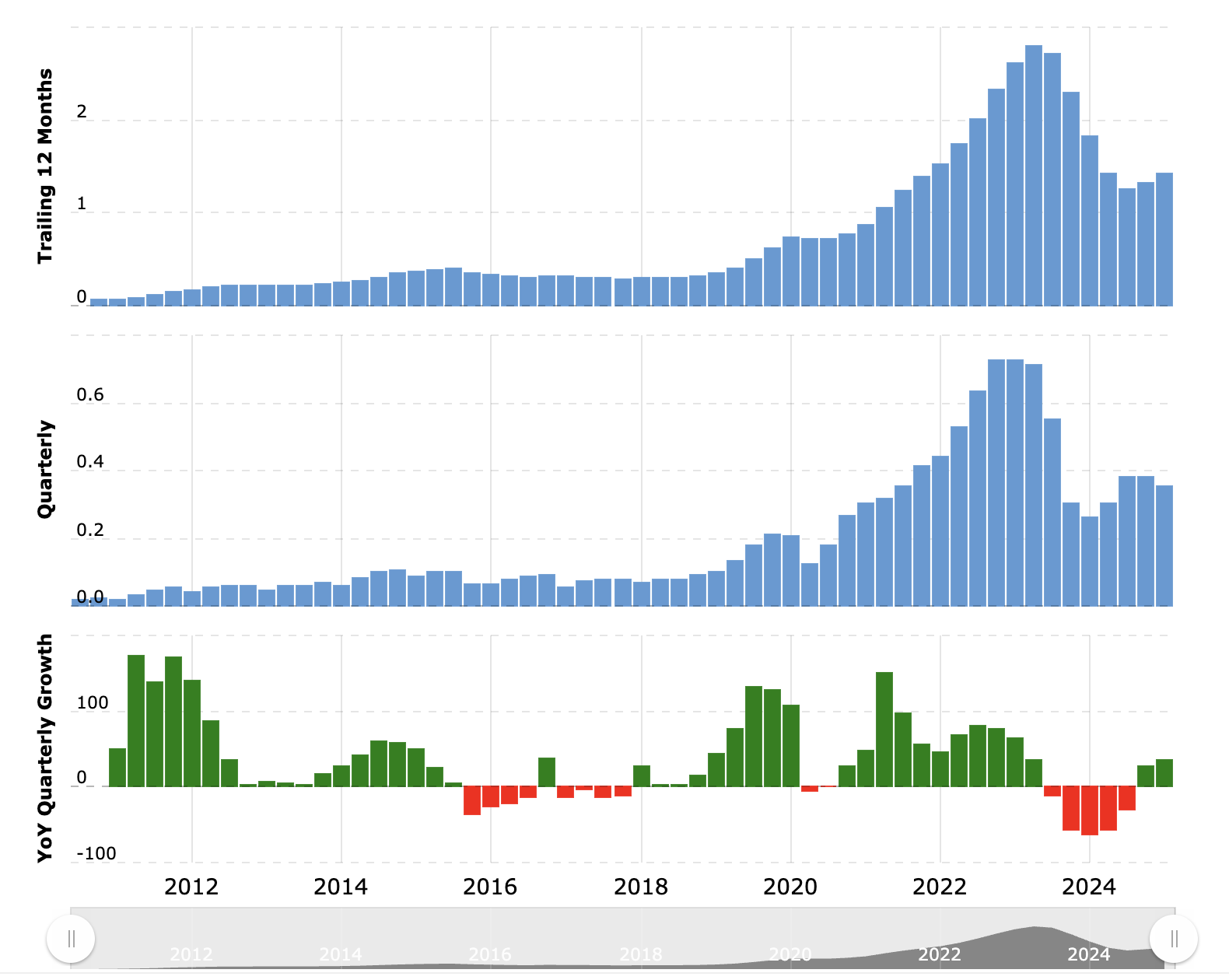

Source: Macrotrends, Annual Revenue Trends

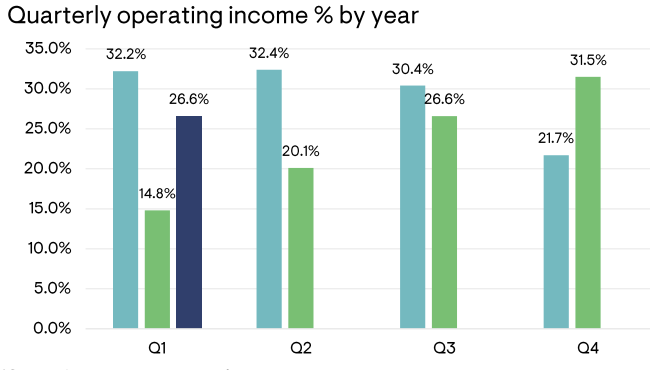

California’s transition to NEM 3.0, rising interest rates, and Europe’s declining utility rates pummeled solar payback economics. But Enphase avoided the temptation to discount or overship. Rather, it maintained gross margins (47.3% GAAP, 48.9% non-GAAP with IRA credits), produced $480 million in free cash, and finished the year with $1.72 billion in cash. For a business that is contracting at the top line, that sort of capital discipline and financial resilience is impressive.

Source: Enphase Investor Presentation, April 2025

The response of the management wasn't merely about preserving profitability. It was about preparing the business for the next solar upcycle, smarter products, more efficient supply chains, and more robust dealer contacts. With survival the minimum in a market this unforgiving, Enphase is continuing to play offense.

Source: Enphase Investor Presentation, April 2025

IQ8 to IQ9: Platform Expansion as a Strategic Hedge

Enphase’s fundamental advantage has always been the architecture. Its microinverters, unlike conventional DC-string inverters, operate at the module level, providing granular control, enhanced fire safety, and plug-and-play scalability. The platform is now moving beyond power conversion to home energy orchestration.

Its IQ8 microinverters, delivered to more than 50 countries, are being replaced by the IQ9 series due in 2025. The next generation model has enhanced support for greater DC input currents up to 18 amps, for three-phase designs, and utilizes gallium nitride transistors for enhanced thermal efficiency at less cost. It has outputs ranging from 427W to 548W AC, well-suited for high-wattage modules.

On the storage side, the IQ Battery 10C introduces 30% greater energy density using 60% less space, made possible through new architecture and U.S.-manufactured batteries. These seamlessly integrate with Enphase’s Ensemble software for intelligent management of solar, storage, and EV charging power flows.

And then there is IQ Balcony Solar, a plug-and-play package for European renters and apartment residents. With the panels plugged directly in to wall receptacles, no permit or installer is needed. That alone has the potential to create a new addressable market across high-density urban areas.

Simply put, Enphase is not only delivering hardware, its creating an adaptive energy operating system that evolves along with the grid, the home, and the customer.

Running Ahead of the Pack: Competitiveness During Industry Consolidation

Its peers, including SolarEdge and Tesla Energy, have struggled to reconcile growth with profitability. SolarEdge experienced severe European inventory overhang along with margin compression. Solar deployments at Tesla lagged due to internal prioritization. Competition is instead offered by the Chinese players on costs but lacks in integration, software, and customer service, spaces where Enphase excels.

What differentiates Enphase isn't the quality of the products, system ease and ecosystem stickiness. Its Solargraf platform automates design, permitting, and quoting for installers. Its 10,300+ certified installers worldwide represent a sticky moat. Its AC architecture provides greater flexibility to accommodate residential systems and commercial systems.

Also paramount is Enphase’s North American scale of manufacturing. The firm has the capacity to produce more than 20 million microinverters per year, of which 5 million are produced in the U.S., enabling IRA qualification and greater resistance to global supply chains disruption. This U.S. bias is not just patriotic, it’s profitability-boosting and policy-friendly.

Relative to peers, Enphase continues to show stronger capital efficiency and operating leverage even in macro stress. Very few can show free cash flow margins greater than 35% in a downcycle.

Source: Enphase Investor Presentation, April 2025

Valuation: Cyclical Overreaction or Repricing

As of May 13th, 2025, Enphase is trading at around $50, with valuation multiples that are strongly pessimistic. Its forward non-GAAP P/E is at 20.6X, a 63% discount to the five-year average at 55x and a 7.5% discount to the sector median. GAAP P/E (FWD) TTM is a bloated 42.25x due to stock compensation and restructuring expenses, far from reflective of underlying cash generation.

The price-to-book is a different tale. At 8.16x, Enphase is 144% above sector median, indicating that investors continue to place a premium on IP, brand, and platform economics. That being said, the firm’s PEG ratio (Non-GAAP FWD) stands at 0.71, which implies underestimated earnings growth, assuming that demand does stabilize and that the upgrades in products drive ASPs higher.

Enterprise multiples point to a potentially undervalued stock with strong upside. The company is trading at a forward EV/EBITDA of 16x, roughly in line with industry norms but a steep 65% discount to its five-year average. Its forward EV/Sales stands at 4.4x, which is 51% above peers yet still significantly below its historical average of 12x, suggesting room for re-rating if revenue momentum continues.

.png)

Source: FinanceCharts

With a conservative estimate of 2026 consensus EPS forecast at $1.8 and a modest multiple of 20, shares could re-rate to $80. With a premium multiple of 25–30x supported by resumed growth, completed IQ9+10C rollout, and monetized VPP expansion, the bull case is $100–$120. That is more than 2x above where the stock is trading.

Key Risks: Volatility, Policy, and Patience

In spite of the underpinnings, Enphase has genuine risks. U.S. and European macro sluggishness has the potential to postpone channel restocking and crimp installer momentum. Changes in policy, most notably around the IRA or EU renewables rules, pose headline risk. And while the IQ9 and IQ Battery 10C introduction are critical, execution has to be perfect, any delay could injure market confidence.

Investor sentiment is also weak. The stock has fallen more than 70% from 2021 highs and is still subject to downward pressure from short-sellers anticipating further decline. It may prove challenging to time the bottom, at least in the event that 2025 is a transition year.

But for long-term investors, the critical question is: is Enphase a structural leader in distributed energy anymore? If so, then the valuation today is a mispricing, not a judgment.

Conclusion

Marcel Enphase’s valuation has been unraveled, but not its narrative. Under the volatility is a business that is still making significant cash, holding the line on margins, and deploying next-gen infrastructure for a distributed, intelligent energy future. This is no longer a growth stock, now it’s a durable platform that is going to enjoy policy tailwinds, product cycles, and global electrification. Enphase at $45 doesn't require perfection to double, merely normalization.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.