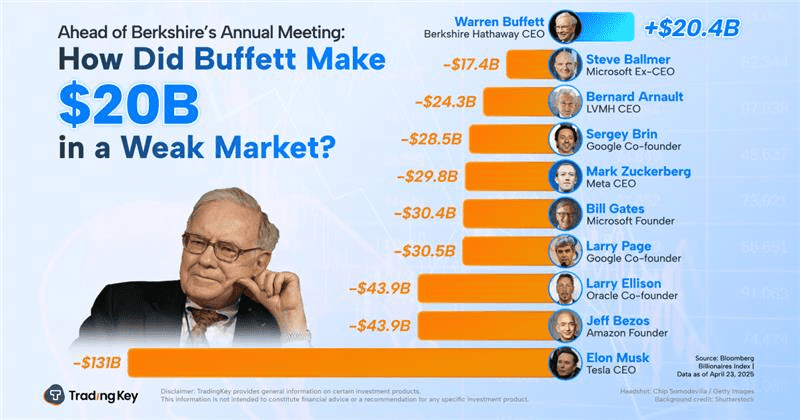

Ahead of Berkshire’s Annual Meeting: How Did Buffett Make $20B in a Weak Market?

Tradingkey - As of April 29, Berkshire Hathaway (BRK.A) shares have surged 17.4% year-to-date, beating the broader market by a wide margin. Meanwhile, the S&P 500 has fallen 5.2%, while the Nasdaq Composite saw a maximum drawdown of 9.4%.

Despite global uncertainty and turbulent equity markets, Warren Buffett’s Berkshire posted significantly positive returns, with Buffett himself gaining more than $20 billion in net worth.

Berkshire will hold its 2025 annual shareholder meeting in Omaha on May 3. The meeting comes at a time when investors around the world are grappling with escalating trade tensions, volatile markets, and clouds over the earnings outlook of U.S. firms and their global peers. This year, many billionaire investors suffer steep losses—Buffett, however, himself gains more than $20 billion in net worth.

Why has the Oracle of Omaha continued to outperform in the face of market headwinds?

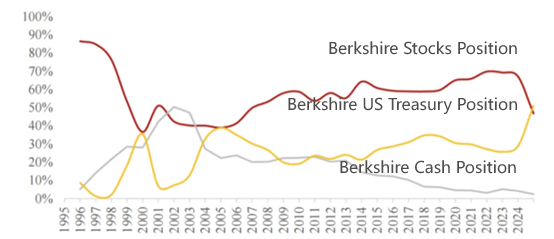

A key reason lies in Buffett’s view that the U.S. equity market has become overvalued, with few truly compelling opportunities. In response, he has steadily reduced his exposure to stocks since late 2021 and raised Berkshire’s cash holdings to historic highs.

Buffett's investment focus has shifted over the decades. In his earlier investing years, he focused on industries like consumer goods and financials—companies he grasped intuitively and that went on to deliver strong returns, such as See’s Candies, Coca-Cola, Bank of America, and Wells Fargo.

After 2016, Buffett took a sizable position in the fast-growing tech sector, driven by evolving consumer trends. Yet as of 2024, Buffett turned cautious again. Concerned about stretched valuations—especially in the AI sector—and the uncertainty surrounding U.S. tax policy amid the Trump administration, he drastically cut his Apple stake.

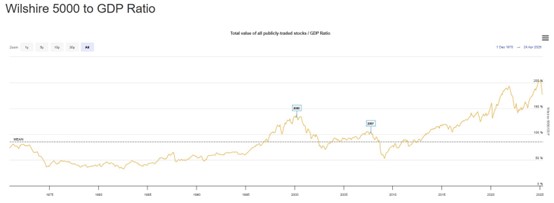

The “Buffett Indicator,” which tracks the ratio of the Wilshire 5000’s total market cap to the U.S. GDP, has stayed above 100% since 2013. Its recent surge past 200% has reinforced Buffett’s view that market valuations are overstretched.

Source: Barchart

As of 2024, Berkshire Hathaway's secondary market equity holdings are primarily allocated across four key sectors: financials, information technology, consumer staples, and energy. During the 2024 annual shareholder meeting, Warren Buffett emphasized that energy and infrastructure investments are typically capital-intensive and yield stable, moderate returns over a long time horizon—fitting well with Berkshire's investment goals.

Morningstar analysts noted that although Buffett’s continued trimming of equity positions may appear conservative, it in fact reflects a proactive approach to risk management. By offloading overvalued assets and raising cash, he effectively shortened the portfolio’s duration from 7.2 years to 5.8 years—positioning it for potential downside scenarios in the U.S. equity market.

Berkshire Hathaway’s massive cash pile serves as a buffer against near-term market volatility. As of the end of 2024, the firm was sitting on over 330 billion cash—its largest cash reserve in history.That's Adramatic jump from about 160 billion at the end of 2023.

the company’s more than 90% of its cash—roughly 300.9 billion—is parked in US.Treasury Bills.That's Nearly 195 billion. This also highlights Buffett’s cautious approach: in an increasingly uncertain global environment, he’s choosing to stay patient, wait for better valuations, and hold dry powder for future opportunities.

Source: Fangzheng Securities

While keeping most of his capital on the sidelines, Buffett has also been putting more focus overseas. On April 11, Berkshire issued six tranches of yen-denominated bonds totaling 90 billion yen (about $629 million). Markets took this as a strong signal that he's doubling down on investments in Japan.

In March, he also increased Berkshire’s stakes in Japan’s five largest trading companies—Itochu, Marubeni, Mitsubishi, Mitsui, and Sumitomo.

In his 2025 annual letter to shareholders, Buffett explained why he likes these firms: not only are they run well, but their business models resemble Berkshire’s in important ways. They’re disciplined with capital, raise dividends responsibly, buy back stock when it makes sense, and compensate their top executives far less aggressively than many U.S. companies.

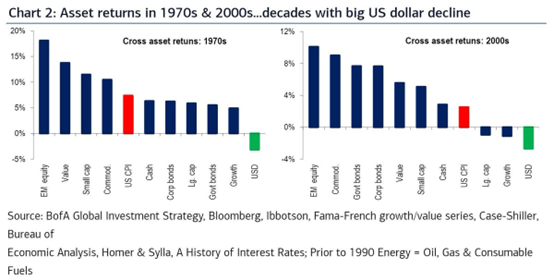

Taking a step back, Buffett's recent activity suggests he may be positioning for a 1970s-like macro environment. Bank of America research shows that in the '70s, emerging-market stocks performed best, followed by value stocks, small caps, and commodities—especially energy. That lines up with Buffett’s focus on oil and value-oriented plays.

Source: Bank of America

On the flip side, the worst performers were growth-oriented bonds and long-duration government debt. Buffett appears to be steering clear of this risk—he’s trimmed Berkshire’s Apple position and has avoided locking up capital in long-dated Treasuries.

The broader U.S. market may be entering a similar phase now: a period marked by elevated inflation and a weaker dollar—trends reminiscent of what investors faced back in the late ‘60s and throughout the ‘70s. And Buffett’s positioning clearly reflects that.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.