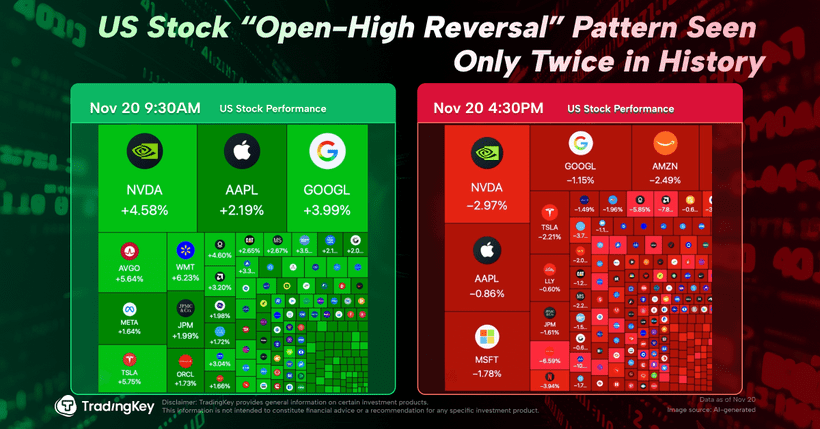

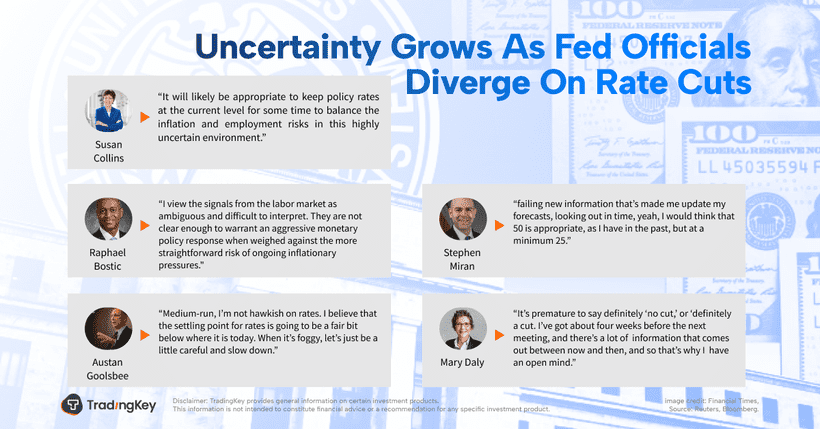

BoE August Rate Decision Commentary: Where Next for the Pound?

TradingKey - On 7 August 2025, the Bank of England (BoE) lowered its benchmark interest rate from 4.25% to 4%, aligning with broad market expectations. Notably, the decision sparked significant division within the committee, requiring two rounds of voting to pass. Influenced by this internal discord and investor expectations of a slower pace of future rate cuts, the pound surged against the dollar within an hour following the announcement.

The core of the disagreement in this rate cut decision lies in the tension between a weakening labour market and rising inflation. On the labour market front, a downward consumption-hiring spiral has driven unemployment steadily higher since March. On the inflation side, headline and core CPI have climbed to 3.6% and 3.7%, respectively, with the BoE forecasting inflation to peak at 4% by September this year.

Given the UK’s challenging mix of a weakening labour market and elevated inflation, the BoE will likely adopt a more cautious approach to rate cuts in the months ahead. Conversely, with the US labour market softening and reflation signals still subdued, the Federal Reserve is poised to restart rate reductions in September. Taking these dynamics into account, the pound’s recent decline against the dollar is expected to stabilise, shifting to a period of range-bound movement.

Source: TradingKey

Main Body

On 7 August 2025, the Bank of England (BoE) announced its policy rate decision. The benchmark interest rate was reduced from 4.25% to 4%, in line with widespread market expectations (Figure 1). Notably, the decision to cut rates sparked considerable division within the Monetary Policy Committee. Specifically, five members, led by Governor Bailey, supported a 25-basis-point cut, while four members, including Deputy Governor Lombardo and Chief Economist Hugh Pill, opposed the move, arguing against any rate reduction. Due to the significant disagreement, the decision required two rounds of voting to pass. Influenced by this internal discord and market expectations of a slower pace of future rate cuts, the pound experienced a notable rise against the dollar within an hour after the announcement.

Figure 1: BoE Policy Rate (%)

(1).jpg)

Source: Refinitiv, TradingKey

The division over this rate cut decision stems from the conflicting pressures of a weakening labour market and rising inflation, raising investor concerns about the UK potentially heading toward stagflation. Regarding the labour market, after a period of stability from November 2024 to February 2025, unemployment has been steadily increasing since March (Figure 2). The BoE noted that subdued potential GDP growth and downward pressure on consumption are key factors driving the labour market's weakness. This consumption-hiring downward spiral is the root cause of the labour market's sluggishness, providing a rationale for the BoE’s rate cut.

Figure 2: UK Unemployment Rate (%)

(1).jpg)

Source: Refinitiv, TradingKey

On the other hand, both headline and core CPI have been on an upward trajectory since September 2024, currently reaching 3.6% and 3.7%, respectively, well above the BoE’s 2% target (Figure 3). According to the latest official projections, inflation is expected to peak at 4% in September this year. While the baseline forecast suggests inflation will gradually ease after peaking, the committee warned that short-term inflationary pressures could further drive up wages and pricing mechanisms. This dynamic reduces the likelihood of the BoE continuing with sustained rate cuts in the near future.

Figure 3: UK CPI (%)

(1).jpg)

Source: Refinitiv, TradingKey

In forex markets, the GBP/USD exchange rate has been steadily declining since its peak in early July, pressured by sluggish UK economic growth, rising inflation, and the BoE’s continued interest rate reductions. Looking forward, given the UK’s challenging mix of a weakening labour market and elevated inflation, the BoE will likely adopt a more cautious approach to rate cuts in the months ahead. Conversely, with the US labour market softening and reflation signals still subdued, the Federal Reserve is poised to restart rate reductions in September. Taking these dynamics into account, the pound’s recent decline against the dollar is expected to stabilise, shifting to a period of range-bound movement.

TradingKey - On 7 August 2025, the Bank of England (BoE) will announce its policy interest rate decision. The prevailing market view suggests a high likelihood of a 25-basis-point rate cut, lowering the benchmark rate from the current 4.25% to 4%. Our assessment aligns with this expectation. The BoE currently faces a challenging dilemma: on one hand, slowing economic growth and a weakening labour market strengthen the case for further rate cuts this month; on the other hand, persistently high inflation constrains the scope for significant rate reductions. In this context, the BoE’s policymakers are likely to prioritise supporting economic growth over curbing inflation, ultimately opting for a 25-basis-point cut. However, significant disagreements among committee members are expected to emerge.

In the foreign exchange market, given the coexistence of low growth and high inflation in the UK economy, the Bank of England is expected to slow its pace of rate cuts after August. In contrast, with a weakening US labour market and no significant signs of reflation, the Federal Reserve is likely to resume its rate-cutting cycle in September. Overall, the current downward trend in the GBP/USD exchange rate is expected to stabilise, transitioning into a phase of relatively modest fluctuations.

.jpg)

Source: TradingKey

Main Body

On 7 August 2025, the Bank of England (BoE) will announce its policy interest rate decision. The market widely anticipates a 25-basis-point rate cut, reducing the benchmark rate from the current 4.25% to 4%, continuing the BoE's pattern of quarterly rate reductions (Figure 1). Our view aligns with this market expectation.

Figure 1: BoE Policy Rate (%)

.jpg)

Source: Refinitiv, TradingKey

The BoE currently faces a challenging dilemma. On one hand, the UK’s real GDP has contracted for two consecutive quarters, compounded by tax hikes that have dampened consumer confidence and slowed corporate hiring. The unemployment rate, after stabilising from November 2024 to February 2025, has been steadily rising since March (Figure 2). This situation provides the BoE with impetus to continue its rate-cutting policy. On the other hand, both headline and core CPI have been on an upward trajectory since September 2024, currently standing at 3.6% and 3.7%, respectively, well above the BoE’s 2% target (Figure 3). This inflationary pressure limits the BoE’s ability to implement significant rate cuts this month.

Figure 2: UK Unemployment Rate (%)

.jpg)

Source: Refinitiv, TradingKey

Figure 3: UK CPI (%)

.jpg)

Source: Refinitiv, TradingKey

This dilemma was already evident during the previous rate cut decisions. In May, when the Bank of England (BoE) lowered the benchmark interest rate by 25 basis points, the Monetary Policy Committee’s vote revealed a three-way split: the majority supported a further 25-basis-point cut, some members advocated for a 50-basis-point reduction, while others favoured maintaining the rate unchanged. For this month’s interest rate decision, we anticipate that the BoE’s policymakers may face similar divisions. Given the current challenges, they are likely to prioritise supporting economic growth over curbing inflation, ultimately implementing a 25-basis-point rate cut, though disagreements among members will likely remain pronounced.

In the foreign exchange market, the GBP/USD exchange rate has been steadily declining since its early July peak, driven by the UK’s weak economic performance, resurgent inflation, and the BoE’s ongoing rate cuts. Looking ahead, given the UK’s challenges of low growth coupled with high inflation, the BoE is expected to slow its pace of rate reductions. In contrast, with a softening US labour market and no clear signs of reflation, the Federal Reserve is likely to resume its rate-cutting cycle in September. Overall, the current downward trend in GBP/USD is expected to stabilise, transitioning into a phase of relatively modest fluctuations.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.