Investment Plays to Watch as ‘The One, Big, Beautiful Bill’ Clears Congress

TradingKey - President Trump formally signed the “One Big Beautiful Bill Act” (OBBBA) into law on July 4, following narrow passage in both chambers of Congress. The law codifies Trump's core campaign pledge — "external tariffs and internal tax cuts".

The legislation extends far more than tax cuts, spanning a sweeping array of political issues across core sectors including healthcare and social security, education, energy, technology, and finance. While the media fixates on the scornful Wall Street meme "TACO" (Trump Always Chickens Out), the administration has steadfastly advanced its agenda. Despite occasional compromises, the OBBBA's scope underscores strategic discipline.

A Structural Realignment in Economic Drivers

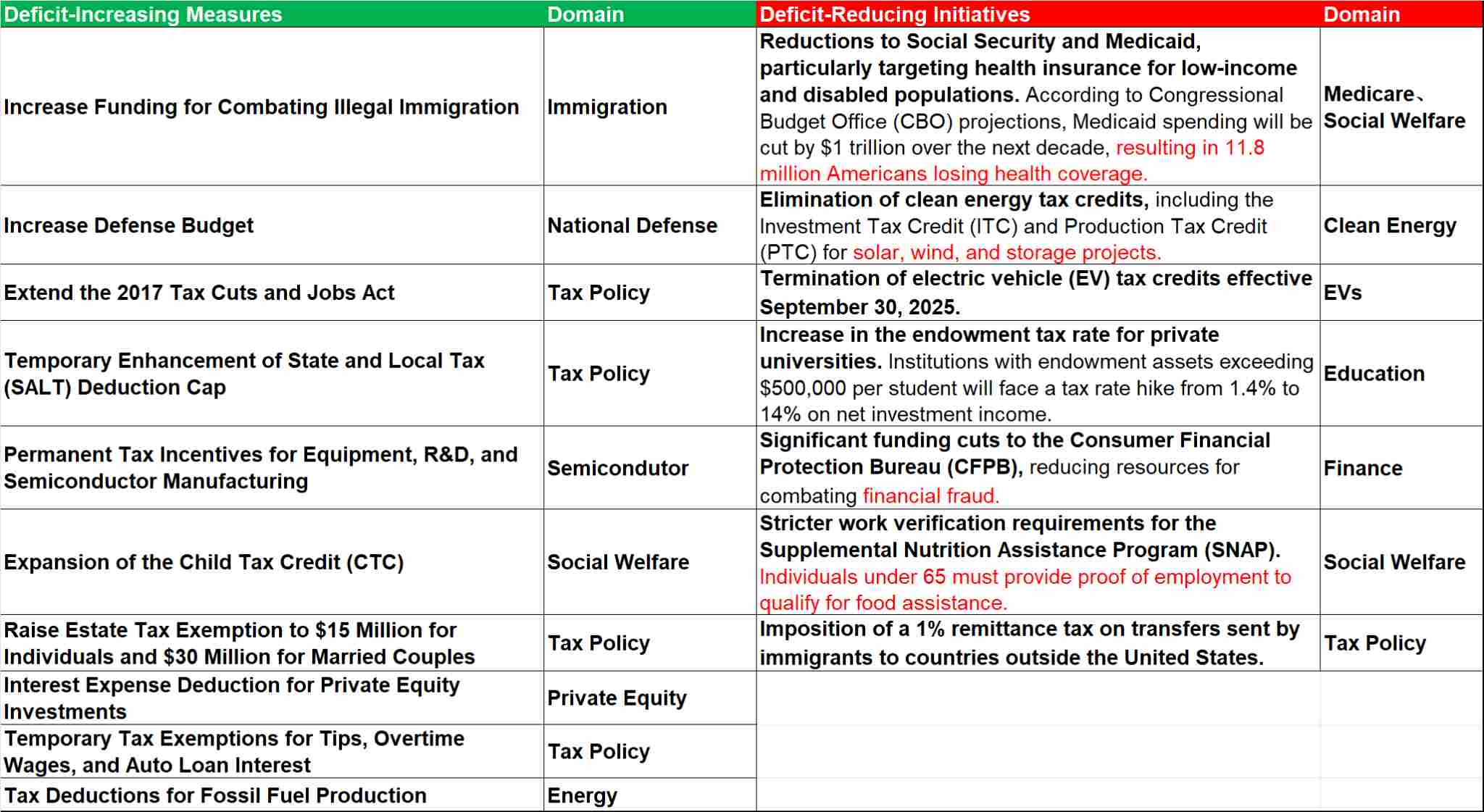

The proposed legislation delineates a bifurcated framework for deficit management, comprising:

Data Sources: TradingKey As of: July, 2025

This legislative architecture signals a paradigm shift in U.S. economic governance — a deliberate transition from state-driven stimulus toward private sector-led growth. In essence, the Trump administration seeks to pivot America from a "big government, small business" model toward a "small government, big business" ecosystem, transferring growth leverage from public balance sheets to households and corporations.

During the pandemic, the U.S. government deployed aggressive fiscal stimulus — including direct payments and expanded safety nets — to stabilize the economy and support vulnerable households. This fueled a surge in the federal deficit, which reached 6.4% of GDP in FY2024, and necessitated massive Treasury issuance to fund expenditures. Concurrently, households saw an unprecedented accumulation of savings.

Looking ahead, reining in the deficit hinges critically on curbing spending on Medicare and Social Security. These twin entitlements, historically the budget’s largest outlays, are projected to exceed $1.7 trillion in FY2025. With pandemic-era support expired, households now bear the full brunt of essential costs: Medical coverage, food security, and other necessities must be funded primarily through wages and employer-sponsored benefits.

.jpg)

Data Sources: Treasury Government, TradingKey As of: May, 2025

From an economic standpoint, GDP equals consumption plus investment plus government spending plus net exports (C + I + G + NX). The One Big Beautiful Bill Act (OBBB) aims to marginally boost personal consumption (C) by slashing taxes on tips and overtime pay, while spurring corporate investment (I) through tax cuts and incentives for plant construction. Concurrently, it hikes tariffs to expand exports of goods and services, thereby swelling the trade surplus (NX). Meanwhile, the legislation scales back the government expenditure (G) that has historically shouldered the burden of economic growth.

The far-reaching implications of this legislation are vastly underappreciated. While many focus solely on its immediate self-interest implications, we contend it will reshape America's trajectory for at least the next four years — and likely well beyond. This pivotal shift demands a critical question for investors: How to navigate this transformation and position capital wisely? Below, we outline key investment areas and related ETFs poised to benefit (We exclude leveraged and inverse ETFs).

- National Defense Theme ETF

Over three years since the Russia-Ukraine conflict erupted and nearly two years into the Israel-Hamas war, both conflicts persist with no resolution in sight. Meanwhile, new flashpoints — notably India-Pakistan tensions and U.S.-Israel-Iran confrontations — have erupted with startling rapidity. Although involved parties claim victory, the world has undeniably reached an inflection point where the erstwhile paradigm of "peace, development, and cooperation" has given way to "confrontation, competition, and challenge."

This shift stems not merely from heightened security concerns amid geopolitical strife, but also from diminished international deterrence against aggressors. The cost of initiating conflicts has plummeted as global enforcement mechanisms weaken — exemplified by Russia's adaptation to sanctions through academic isolationism and domestic supply-chain realignment.

Fundamentally, this turmoil is driven by the post-Kondratiev wave economic reality. With the last long-wave economic cycle having crested, nascent technologies like artificial intelligence (AI) and robotics have yet to fully ignite new productivity growth. Consequently, slumping global demand has intensified zero-sum competition for finite resources.

With the world's hegemon stepping back from underwriting global stability — retreating from multilateral trade pacts, weaponizing tariffs to boost its surplus, and trimming military footprints in secondary theaters — the international order is reverting to raw power politics. In “the law of the jungle”, comprehensive national power (military, technological, economic) becomes the ultimate arbiter of "justice" and survival.

The implications are stark: NATO now demands members hike defense spending to 5% of GDP — a threshold signaling combat readiness — as Washington ends its subsidy of European security. Japan’s March activation of a Joint Operations Command and America’s formal embrace of trillion-dollar defense budgets underscore a tectonic pivot from growth to security. Survival, not expansion, is the new imperative.

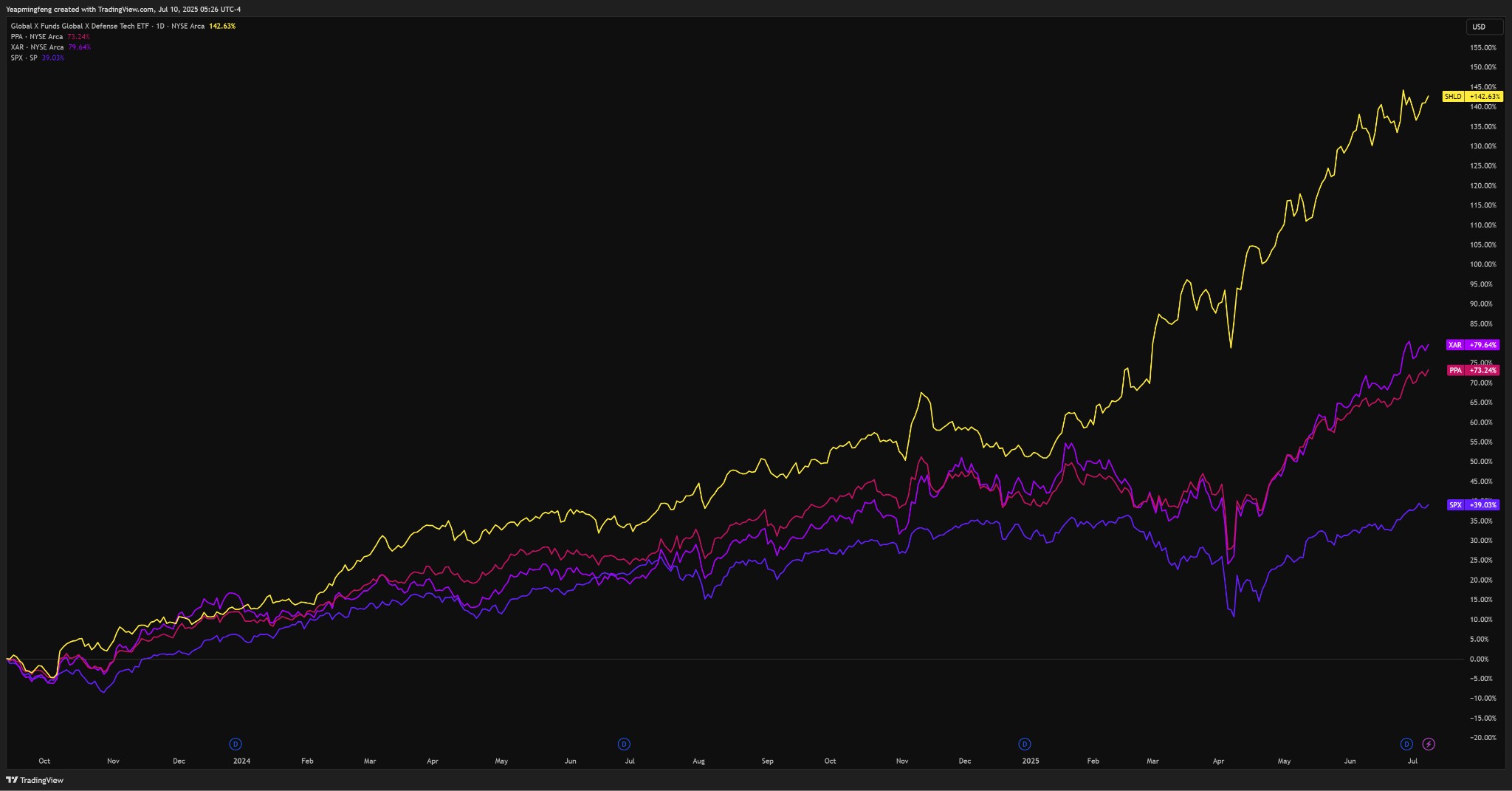

In this climate of escalating geopolitical friction, allocating to aerospace & defense ETFs (exchange-traded funds) emerges as a strategic imperative — both as a hedge against black-swan events and a fundamental play. Defense equities boast a recession-resistant "to-government" (To-G) business model; when global growth stutters, their revenue streams remain fortified by swelling military budgets.

Moreover, during acute crises — sudden conflicts, kinetic escalations — investor capital predictably flees to havens like gold and defense assets.

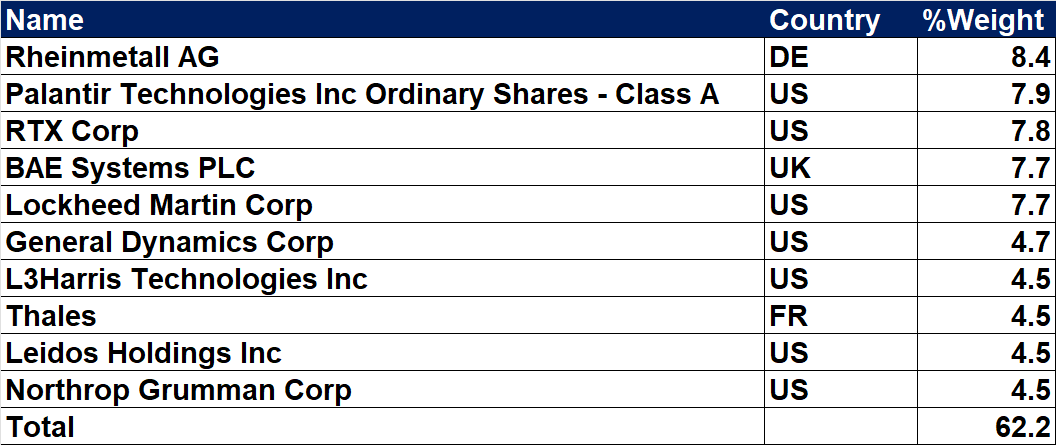

Investors seeking thematic exposure to defense and aerospace may consider three U.S.-listed ETFs: the Global X Defense Tech ETF (SHLD), the Invesco Aerospace & Defense ETF (PPA), and the SPDR S&P Aerospace & Defense ETF (XAR).

SHLD provides targeted access to the next-generation defense technology ecosystem, tracking companies at the forefront of AI, cybersecurity, and advanced military systems. Many holdings trace their industrial legacy to World War II or earlier, reflecting deep-rooted sector expertise. For U.S.-based investors, SHLD offers a cost-efficient path (expense ratio: 0.50%) to global defense innovators. Its globally diversified portfolio spans 45 holdings, with top 10 allocations are bellow:

Unlike SHLD, both PPA and XAR focus exclusively on U.S.-listed defense equities. Their divergent performance trajectories stem from structural distinctions: PPA uses a modified market-cap weighting with single-stock caps, but XAR employs equal weighting. This methodological gap explains XAR’s recent outperformance amid small-cap rallies, while PPA’s tilt toward megacaps provides stability during volatility.

Data Sources: Reuters,TradingView, TradingKey As of: July 10, 2025

- Technology and Semiconductor Theme ETF

China has achieved overtaking on the curve in multiple sectors amid U.S.-China rivalry, dominating fields like energy vehicles (EVs), photovoltaics, and rare earths. Yet semiconductors and artificial intelligence (AI) remain the few critical domains where the U.S. maintains a decisive "chokehold" — enabling effective containment efforts.

Despite early-year concerns over potential overinvestment in AI — triggered by Chinese firm DeepSeek’s breakthrough large-scale model — Nvidia’s unassailable GPU supremacy, TSMC’s foundry dominance, and ASML’s monopoly on EUV lithography make near-term Chinese parity in tech and semiconductors a distant prospect.

The semiconductor supremacy agenda has become a cross-administration imperative in Washington. From the Trump era to the Biden administration, escalating export controls and sanctions against China’s chip industry have intensified, culminating in the One Big Beautiful Bill Act (OBBBA).This landmark legislation entrenches America’s dual strategy of technological containment and capital repatriation through three pivotal mechanisms:

- Permanent Tax Breaks & Manufacturing Incentives

- Deregulation of AI Development

- Fortifying Capital and Technology Moats

For exposure to U.S. tech hegemony beneficiaries, consider these ETFs:

ETF Ticker | Full Name & Focus | Key Holdings & Differentiation | Expense Ratio |

SOXX | iShares Semiconductor ETF | Broadcom (9.4%), NVIDIA (8.4%), AMD (7.6%). 35 stocks, diversified across fabless designers & equipment makers . | 0.35% |

SMH | VanEck Semiconductor ETF | NVIDIA (19.5%), TSMC (12.8%). Concentrated 25-stock portfolio—leveraged to AI chip dominance . | 0.35% |

VGT | Vanguard Information Tech ETF | Apple (20%), Microsoft (15%). 300+ stocks spanning AI software, payment systems (Visa/Mastercard), and hardware . | 0.10% |

Data Sources: Reuters, TradingView, TradingKey As of: July 10, 2025

- Energy Theme ETF

A stark policy pivot under the incoming Trump administration is poised to reshape America's energy landscape, driven by deep partisan divides and contrasting industry backers. While clean energy faces significant headwinds, traditional fuels — particularly nuclear — stand to gain substantial government support.

The anticipated rollback of crucial tax credits for wind, solar, and electric vehicles (EVs) threatens to dampen domestic growth trajectories in these sectors significantly. Conversely, the administration's agenda prioritizes revitalizing coal, oil, and natural gas through targeted tax relief. Most notably, it champions a nuclear renaissance, offering robust investment incentives and favorable tax treatment aimed at deploying advanced reactor technologies. The strategic goal is clear: securing a massive, reliable power base critical for burgeoning energy-intensive technologies like artificial intelligence (AI) and advanced military systems.

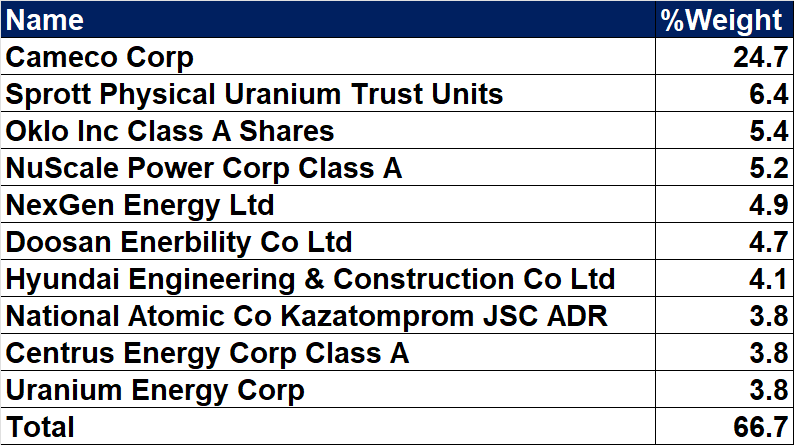

For investors seeking exposure to this nuclear-focused policy tailwind, the Global X Uranium ETF (URA) warrants close attention. This ETF provides diversified access to the global uranium supply chain, holding 51 companies involved in uranium mining, exploration, refinement, nuclear component manufacturing, and related services.Its largest holding, commanding nearly 25% of assets, is Cameco Corp. (CCJ), the world's second-largest uranium fuel producer. Cameco's strategic position is further bolstered by its significant 49% ownership stake in Westinghouse Electric Corp., a leading global nuclear reactor designer and builder.

Data Sources: Reuters, TradingKey As of: July 10, 2025

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.