Sequoia Fund Inc: Quiet Conviction in a Noisy Market

TradingKey - Few mutual funds have a following as cultlike as that of the Sequoia Fund (SEQUX). Once synonymous with legendary manager Bill Ruane, and thereafter with Robert Goldfarb, Sequoia became known for not playing Wall Street's short game.

These days, as Goldfarb has slipped out of public view, the philosophy remains: buy a narrowly focused basket of rugged businesses, be patient, and let quality compound over time. It’s a formula growing increasingly rare in a world where hot takes and fast money are so front and center in public discourse.

Sequoia's holdings under management as of March 31, 2025, were approximately $3.31 billion in 24 holdings. Turnover in the Fund is 1%, highlighting its "buy right, sit tight" discipline. To a new generation of investors, that number alone is almost defiant.

How is the Portfolio Positioned?

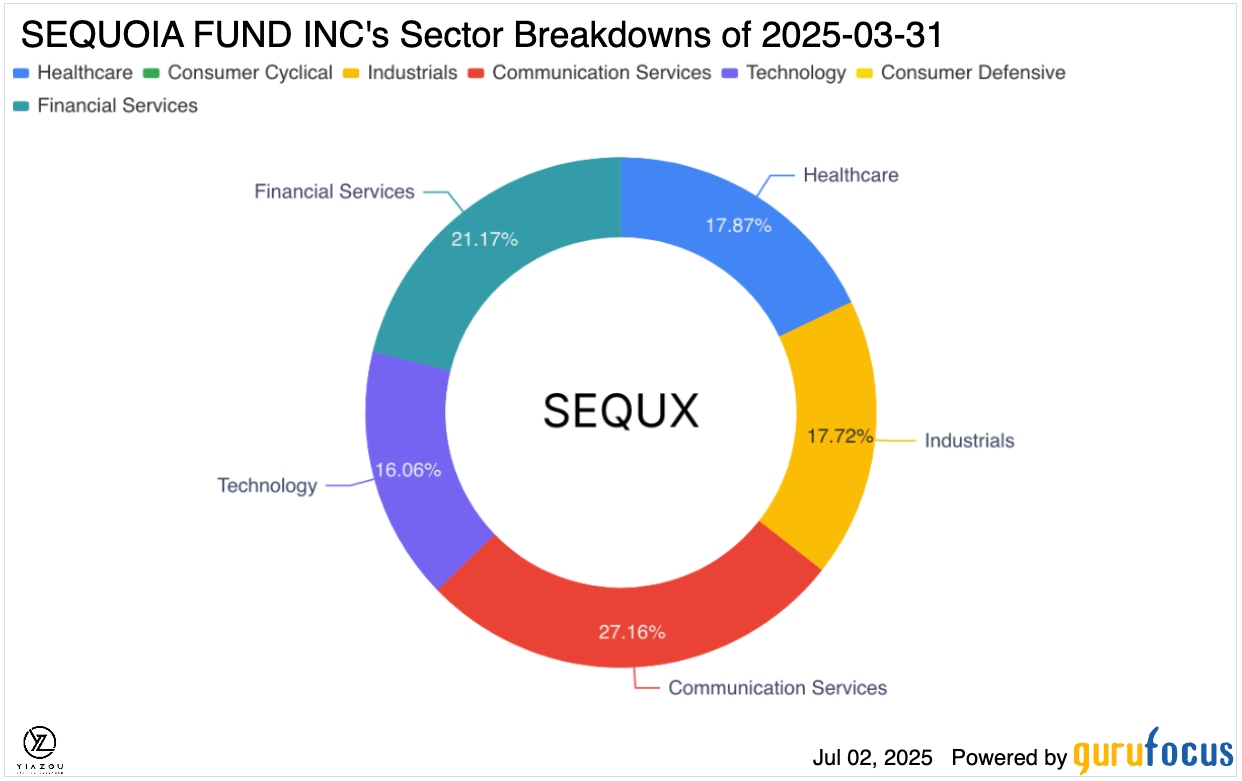

What is a fortress portfolio then in 2025? Sequoia's recent portfolio is a judicious blend, but with clear leans by sector. Communication Services dominates the breakdown at 27.16%, a slice that reveals a lot about where the team thinks there are sustainable moats. Alphabet (GOOGL), a tech titan, and Liberty Media anchor that risk. These are sectors that command eyeballs and ad dollars, good economy or bad.

Next: Financial Services at 21.17%. It’s a category Sequoia knows a lot about, with names like Charles Schwab and Intercontinental Exchange as reliable ballast. Even in a world of rising rates and regulation talk, these businesses generate predictable free cash flow. The kind that lets Sequoia weather drawdowns when things go sour in the market.

Health care is not a slacker, either, accounting for 17.87% of the slice. Elevance Health and UnitedHealth Group are just a few examples of how the portfolio wagers on healthcare's secular tailwinds without going for moonshots. With an aging world, that's a reasonable allocation. Industrials (17.72%) and Technology (16.06%) round out heavyweight sectors, contributing just enough cyclical push and innovative oomph to propel the ship forward.

What isn't there is telling too. Sequoia won't go anywhere near meme stocks or speculative small caps. Nowhere in this portfolio is there a crypto play. This is a mutual fund that knows its bread and butter: big companies with pricing power and established market share.

The Big Bets, The Names that Define the Fund

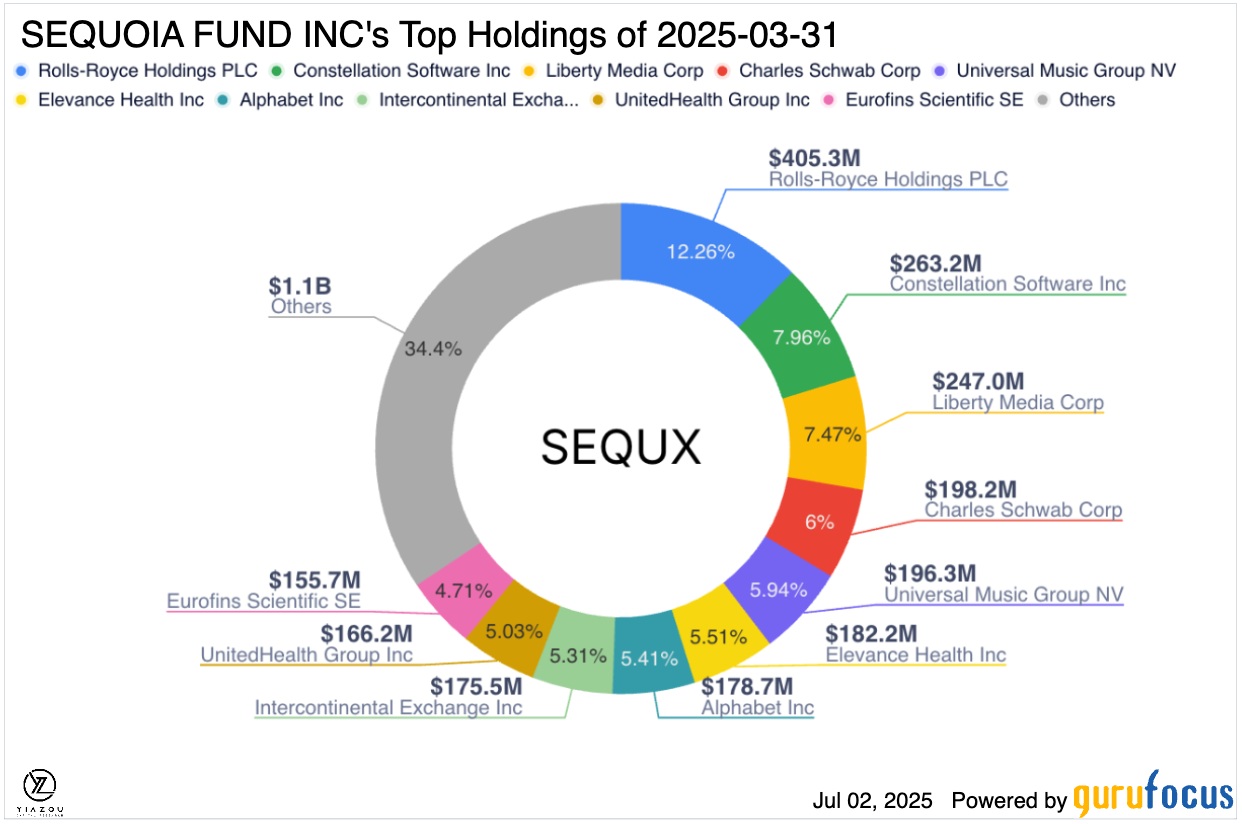

The firm's leading holdings make its high-conviction approach more than apparent. Rolls-Royce Holdings PLC occupies the top spot, owning 12.26% of assets, a surprising leaning towards aerospace. This is a position that has increased significantly since the pandemic, and it is based on a thesis that worldwide air travel and defense expenditures still have years of growth in front of them. Long-duration contracts and non-replication tech are a moat-hungry investor’s ultimate checklist, and Rolls-Royce meets it in spades.

Constellation Software Inc. comes next at around 8%. This is a Canadian gemstone that is a vertical market software bet, zestless on the surface but a cash flow machine beneath. Liberty Media, with 7.47%, gives a slice of a stake in media and live shows. Schwab and ICE feature again too, supporting Sequoia's penchant for scalable financial platforms.

Notably, it is also a healthy shareholder of Alphabet (5.5%) and Elevance Health (5%), alongside UnitedHealth and Eurofins Scientific. The diversification is a sign of Sequoia’s balancing portfolio: growth engines and defense earners intertwined. You won’t see Sequoia investing 20% behind a single moonshot.

Heat Map, Winners, Losers, and Moves

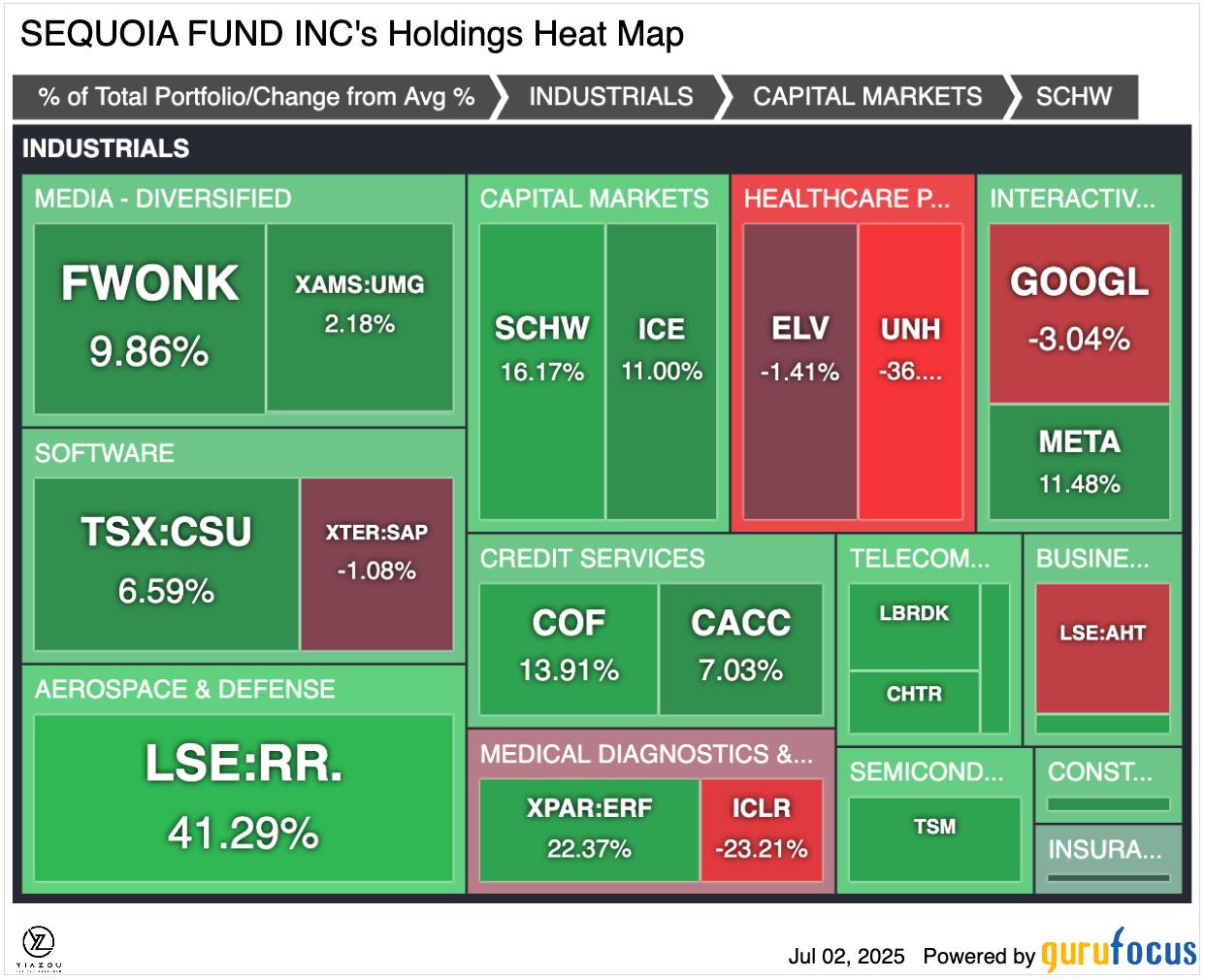

A glance at the fund’s holdings heat map adds further detail. The Rolls-Royce stake is enormous at 41%, but remember that's a part of its industrial sleeve. It's a vote of confidence in aviation's survival. The Schwab 16.17% stake in capital markets shows just how much confidence the managers have in the brokerage sector despite a jump in zero-fee competitors.

Healthcare holdings are more problematic. UnitedHealth and Elevance have both been reduced or hedged, a sign that the team is cautious around margin squeeze or political risk in managed care. The fund's stake in aerospace and selects in diversified media has held up, meanwhile.

Significantly, busy new names have not been added by managers. Neither were any new purchases made last quarter; only allocations were made in position trimming. The massive trimming of Intercontinental Exchange ((-42%) represents the largest change and is perhaps a sign that valuations are not as good there anymore. That is pure Sequoia: when in doubt, prune leaders to keep things in check rather than go searching for additional returns.

Keeping Up with the Index, but on Its Own Terms

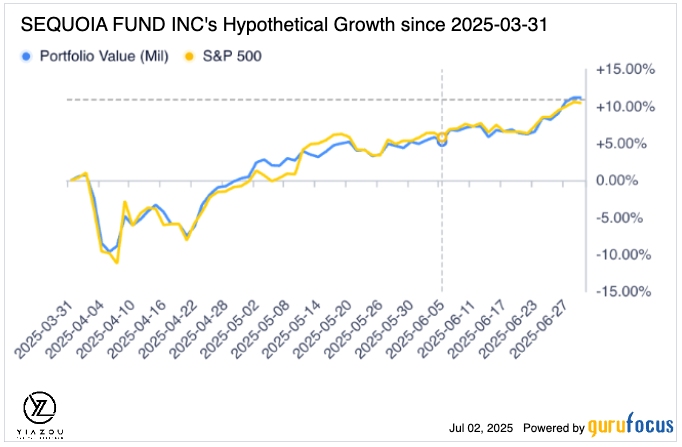

Sequoia’s theoretical growth chart took a course very similar to that of the S&P 500 in recent months. The Fund rode out the ups and downs and returned with the market overall following the early April shakeout. This very close indexing of the index, but with a low-turnover, streamlined roster, highlights what is unique about Sequoia.

The Fund's approach has been successful over decades, though not every year. Longholders know when it won overwhelmingly during that 2010s post-crisis bull run and again in 2020’s market rebound. The flip side is clear, too: with big, concentrated bets, the Fund loses when dramatically different market turns happen or when its anchor sectors fall out of favor. For most shareholders, however, that’s part of the package, they’d rather have a high-conviction basket than a diluted index hugger.

Lessons from Goldfarb's Legacy

If there's been a constant, it's Sequoia's observance of Robert Goldfarb's tried-and-true template. While his longtime stock-picking partner stepped back years ago, his signature remains. The team isn't susceptible to that next-shiny-thing syndrome. They still run a tight ship with turnover over 5% only occasionally. You label that old-school discipline; it's a scarce commodity these days even among “value” funds. Indeed, no fund is perfect.

Some critics argue that Sequoia is too small today to move mountains with massive investors. Some assert that it's out of its prime, eclipsed by a flood of low-fee indexing funds. However, to those who consider investing as owning pieces of durable businesses, not transitory ticker symbols, Sequoia is a refuge from the fray.

A Fund For The Patient Few

In a world addicted to quarter-to-quarter runs and day-to-day changes, Sequoia takes a timely reminder to shareholders that conviction, rather than churn, generates wealth over decades. The message is more timely than ever. This is a Fund that flies under the radar but more than deserves its presence in hundreds of thousands of old 401(k) plans and trust accounts. Whether you're a newcomer looking to learn from old hands or a seasoned allocator looking for predictability, Sequoia's recent snapshot shows that the old saying is still true: when you have a good business at a fair valuation, sometimes the best move… is doing nothing at all.

.png)

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.