[IN-DEPTH ANALYSIS] U.S. Treasury Turmoil: If It Happens Again, What Would Be the Impact on U.S. Stocks and the Dollar?

Executive Summary

TradingKey - The "One Big Beautiful Bill", Moody's downgrade of the U.S. sovereign credit rating, underwhelming U.S. Treasury auction results, and fading expectations for Federal Reserve rate cuts collectively triggered the U.S. Treasury turmoil on 21 May 2025. Looking ahead, while we consider the probability of it happening to be low, if the Treasury turmoil happens again, U.S. Treasury yields and U.S. stocks could revert to an inverse relationship, leading to a "stock-bond" double sell-off. However, our baseline forecast is that accommodative monetary policy combined with supportive fiscal measures will outweigh economic slowdown concerns, supporting a medium-term bullish outlook on U.S. stocks. This suggests that any short-term market dips present entering opportunities. Regarding the U.S. dollar, if rising Treasury yields are driven by uncertainties in Trump’s foreign policy, concerns over U.S. debt credibility, and the Federal Reserve’s policy dilemma—prompting global capital to shift toward non-dollar assets—the inverse relationship between Treasury yields and the dollar index will persist, leading to a sustained decline in the dollar.

Source: Mitrade

Source: Mitrade

* Investors can directly or indirectly invest in the stock market and foreign exchange market through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Background

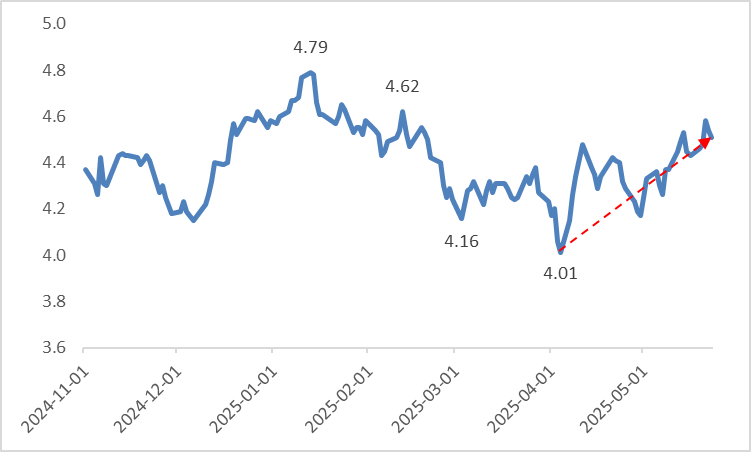

On 21 May 2025, U.S. Treasury yields surged significantly, with the 10-year yield breaking above 4.6% and the 30-year yield exceeding 5%. Treasury yields had already begun rebounding after hitting a low of 4.01% on 4 April 2025 (Figure 1.1). The introduction of tariffs disrupted dollar-based assets, and this, combined with escalating fiscal debt concerns, drove the rise in Treasury yields in April. The sustained increase in yields through May was driven by more specific factors:

- The U.S. House Committee on Ways and Means passed the "One Big Beautiful Bill" aiming at domestic tax cuts. If this legislation is enacted, it will reduce U.S. tax revenue and exacerbate the national debt. Consequently, the U.S. government will need to issue more bonds to finance its operations, increasing Treasury supply and driving up yields.

- Due to deteriorating U.S. fiscal prospects, Moody’s, one of the three major global rating agencies, downgraded the U.S. sovereign credit rating from Aaa to Aa1 (Figure 1.2). This triggered market volatility, leading to a sell-off of U.S. Treasuries and a rise in yields.

- Poor U.S. Treasury auction results catalysed the yield surge on 21 May 2025. Due to weak demand, the 20-year Treasury yield breached 5% for the first time since November 2023, with the final auction yield reaching 5.05%. This was 20 basis points higher than in April.

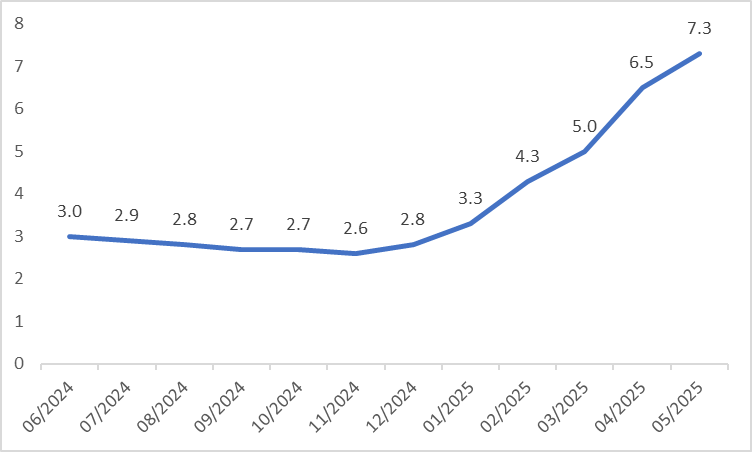

In addition to the three direct factors mentioned above, an indirect driver of rising U.S. Treasury yields is the recent resilience of the U.S. economy. High-frequency data shows significant improvements on the demand side, with Retail Sales and New Home Sales growth accelerating notably in recent months (Figures 1.3 and 1.4). On the production side, Industrial Production has turned positive since late last year (Figure 1.5). Manufacturing and services PMIs rose from 50.2 and 50.8 in April to 52.3 in May, respectively. This robust economic performance, combined with tariff measures, has heightened investor expectations for U.S. inflation. The Michigan 1-Year Inflation Expectations have been rising for several months, with the latest May data indicating a 1-year inflation expectation of 7.3% (Figure 1.6). Economic resilience paired with elevated inflation expectations suggests the Federal Reserve may delay rate cuts and reduce their magnitude, further driving up Treasury yields.

Figure 1.1: 10-Year Treasury Yields (%)

Source: Refinitiv, TradingKey

Figure 1.2: Rating Agency Downgrades

Source: Refinitiv, TradingKey

Figure 1.3: Retail Sales (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 1.4: New Home Sales (%, m-o-m)

Source: Refinitiv, TradingKey

Figure 1.5: Industrial Production (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 1.6: Michigan 1-Year Inflation Expectations (%)

Source: Refinitiv, TradingKey

2. Risk Warning: What If the U.S. Treasury Turmoil Happens Again?

Looking ahead, our baseline view is that as the impact of tariffs gradually emerges, the U.S. economy will slow. This will curb significant inflationary rebounds from the demand side. Under the combined effect of low growth and low inflation, the Federal Reserve is expected to resume its rate-cutting cycle in July 2025. However, as the primary purpose of this article is to provide a risk warning, we focus on an alternative scenario—stagflation—despite its low probability. Historically, during stagflation periods, such as the 1970s and late 2007 to early 2008, the Federal Reserve often tightened monetary policy to prioritize combating inflation. If this scenario reoccurs in the second half of 2025, U.S. Treasury yields will continue to rise, with profound implications for U.S. stocks and the dollar.

3. Impact on U.S. Stocks

If U.S. Treasury yields continue to rise, three key drivers will affect U.S. stocks. First (negative effect), Treasury yields serve as a benchmark for many loan rates. Higher yields increase borrowing costs for listed companies, squeezing their profit margins and reducing stock prices through the numerator in valuation models. Second (negative), stock valuations depend on the discounting of future cash flows. Rising yields lower the present value of these cash flows, driving stock prices down through the denominator. Third (positive), if Treasury prices fall, capital exiting Treasuries may flow into U.S. stocks, creating a "seesaw effect" that supports equity markets.

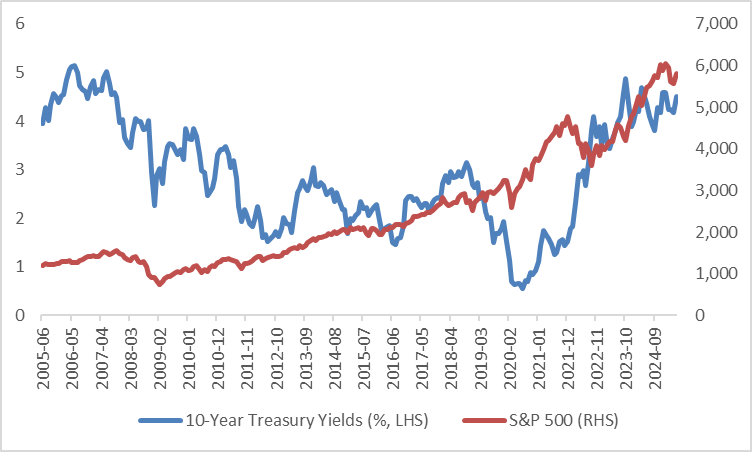

Historically, the relationship between U.S. Treasury yields and U.S. stocks has alternated between positive and negative correlations. Broadly, before 2020, Treasury yields and stock prices were inversely correlated, while post-2020, they exhibited a strong positive correlation (Figure 3). Looking ahead, if the U.S. Treasury turmoil happens again, driven by tariff uncertainties and a weakening safe-haven status of U.S. debt, we expect the trend since 2020 to reverse. Treasury yields and U.S. stocks are likely to shift to an inverse relationship, resulting in a "stock-bond" double sell-off.

We reiterate our baseline forecast of "low growth + low inflation", prompting the Federal Reserve to resume its rate-cutting cycle in July 2025. This accommodative monetary policy, combined with supportive fiscal measures such as domestic tax cuts, will outweigh the impact of an economic slowdown, supporting our medium-term bullish outlook on U.S. stocks. Consequently, if the U.S. Treasury turmoil happens again and triggers a short-term decline in U.S. stocks, it presents an entering opportunity.

Figure 3: Relationship Between Treasury Yields and Stocks Over the Past 20 Years

Source: Refinitiv, TradingKey

4. Impact on the U.S. Dollar

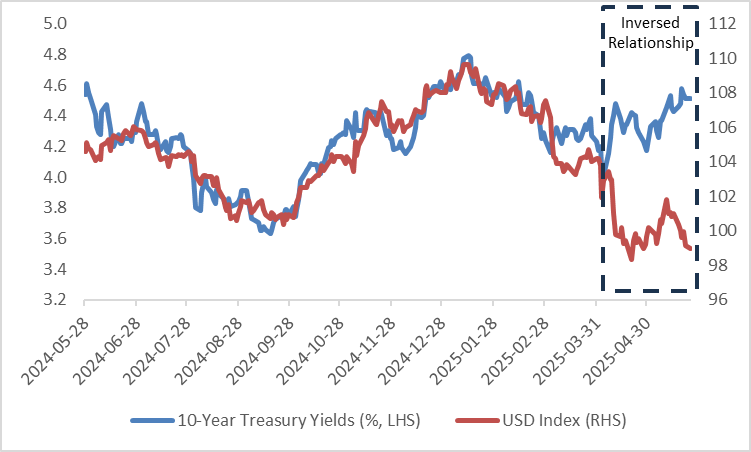

Economic principles suggest a strong positive correlation between U.S. Treasury yields and the U.S. dollar index (Figure 4). This is driven by two main factors. First, rising Treasury yields make U.S. debt more attractive, prompting foreign investors to purchase Treasuries for higher returns. Since Treasuries are dollar-denominated, increased demand for them boosts dollar demand, supporting the dollar index. Second, rising Treasury yields typically reflect investor expectations of Federal Reserve rate hikes, which further enhance the dollar’s appeal.

Recently, U.S. Treasury yields and the U.S. dollar index have exhibited an inverse relationship. This is primarily driven by uncertainties in Trump’s foreign policy, concerns over U.S. debt credibility, and the Federal Reserve’s policy dilemma, which have prompted global capital to shift toward non-dollar assets. These factors have reduced demand for the dollar, weighing on the dollar index. Looking ahead, if the U.S. Treasury turmoil happens again and continues to be driven by these factors, the inverse relationship between Treasury yields and the dollar index is likely to endure, leading to a sustained decline in the dollar.

Figure 4: Relationship Between Treasury Yields and USD Index

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.