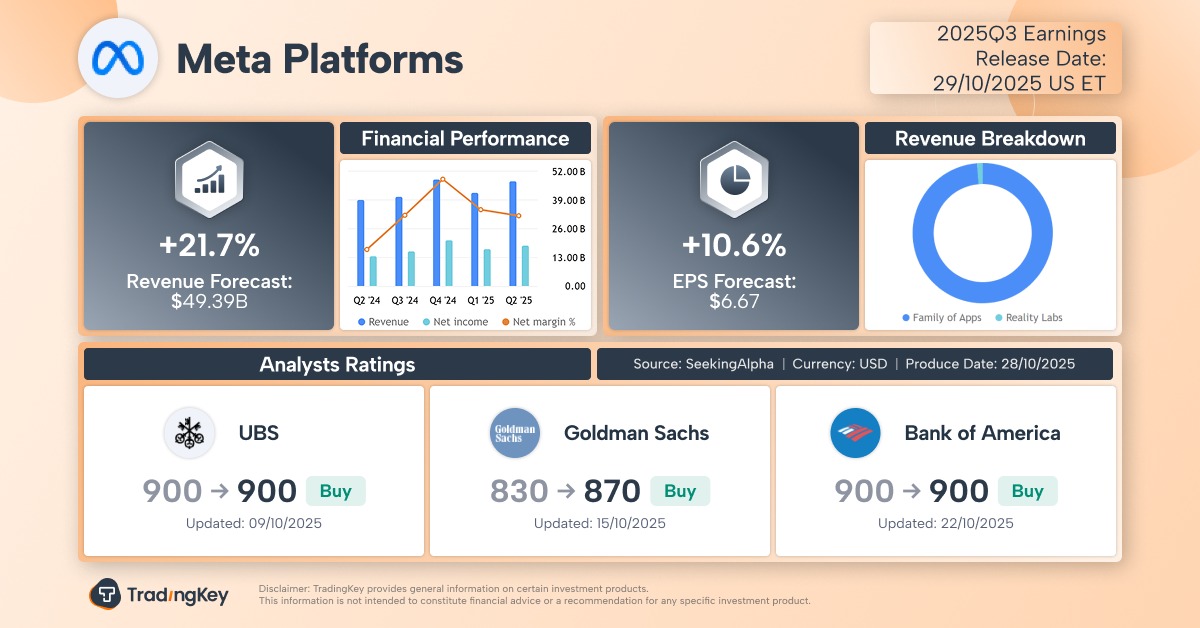

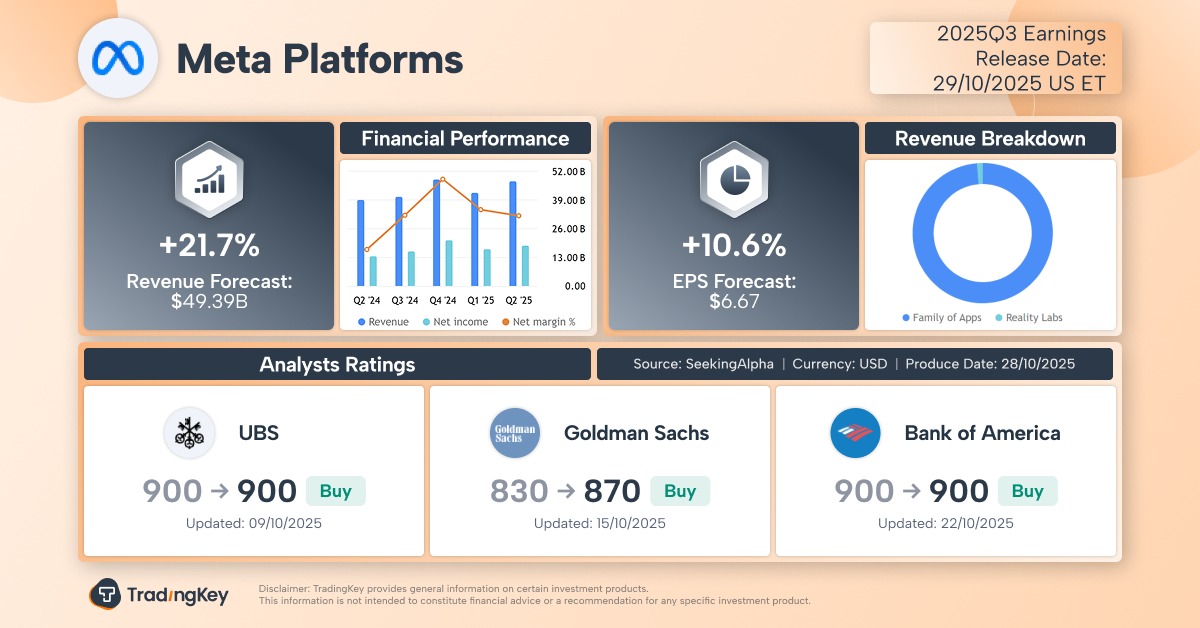

Meta Q3 Earnings Preview: The AI Advertising Boom vs. The Capex Surge

TradingKey - Meta (META), the parent company of Facebook, will report its Q3 2025 earnings after market close on Wednesday, October 29. Investors are focused on whether AI-driven advertising continues to deliver strong growth, if the company will raise capital expenditure (capex) guidance again, and whether it can validate its AI monetization strategy. A key concern: Has Meta’s aggressive “all-in” approach to AI — in data centers and talent — crossed into overinvestment?

According to Seeking Alpha, Wall Street analysts expect:

- Revenue: $49.39 billion, up 21.7% YoY from $40.59B

- EPS: $6.67, up 10.6% YoY from $6.03

Meta’s business is split into two segments:

- Family of Apps (FoA) – Includes Facebook, Instagram, Messenger, WhatsApp, and Threads; Contributed ~98% of total revenue last quarter

- Reality Labs – Develops Quest headsets, smart glasses, and metaverse tech; Still losing billions annually

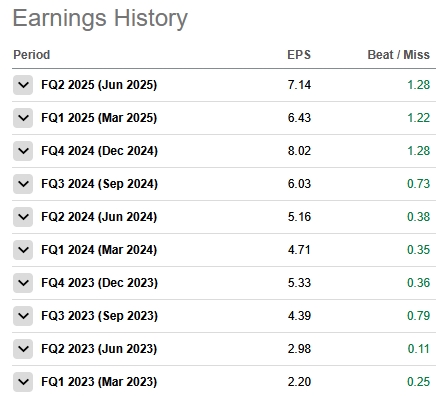

Today, Meta is deploying its entire corporate machine to win in AI. After two capex hikes in the first half of 2025, the company has delivered strong results — with EPS beating consensus for 10 consecutive quarters.

Meta EPS History, Source: SeekingAlpha

Analyst expectations sit at the upper end of Meta’s own guidance range of $47.5–50.5 billion, and the projected 21.7% growth exceeds pre-earnings forecasts of 13% (Q1) and 14% (Q2).

AI Powers Ad Revenue Growth

Unlike cloud giants Google, Microsoft, and Amazon, Meta lacks a cloud infrastructure business. Instead, it monetizes AI through advertising efficiency — using AI to improve ad targeting, creative generation, budget allocation, and conversion optimization — boosting advertiser ROI and driving higher ad spend.

AI is now a core driver of revenue growth, enabling more personalized, automated, and effective ad delivery.

In May, CEO Mark Zuckerberg said that businesses used to make their own ads and define their audience. Now, AI can often target better than they can — and it keeps getting better.

He predicts AI-driven productivity gains will increase advertising’s share of global GDP over the next several years.

In Q2, Meta posted revenue of $47.52 billion (+21.6%), with ad revenue hitting $46.5 billion, exceeding expectations.

Zuckerberg noted that AI is lifting our ad business — and will power every part of our company.

Key AI impacts in Q2:

- New AI ad recommendation models drove ~5% more conversions on Instagram and +3% on Facebook

- Improved content relevance led to +5% time spent on Facebook, +6% on Instagram

Per Zacks Investment, analysts project Q3 ad revenue of $48.5 billion, up 21.6% YoY. Bank of America expects +23% growth, potentially surpassing $50 billion — a new record.

Justin Post, BofA analyst with a $900 price target, said that AI-driven demand for ads across Facebook, Instagram, Threads, and WhatsApp could be strong in Q3.

He highlighted key growth drivers:

- AI-powered targeting optimization

- Deeper CRM integration

- Unified video modeling

- Growing adoption of generative AI creative tools by advertisers

Doug Anmuth, JPMorgan analyst, called Meta his top pick for Q3 earnings season, citing AI ad improvements, Reels, and video momentum. He praised Meta’s execution on AI and focus on “personal superintelligence,” with emphasis on ads, engagement, business messaging, MetaAI, and AI devices.

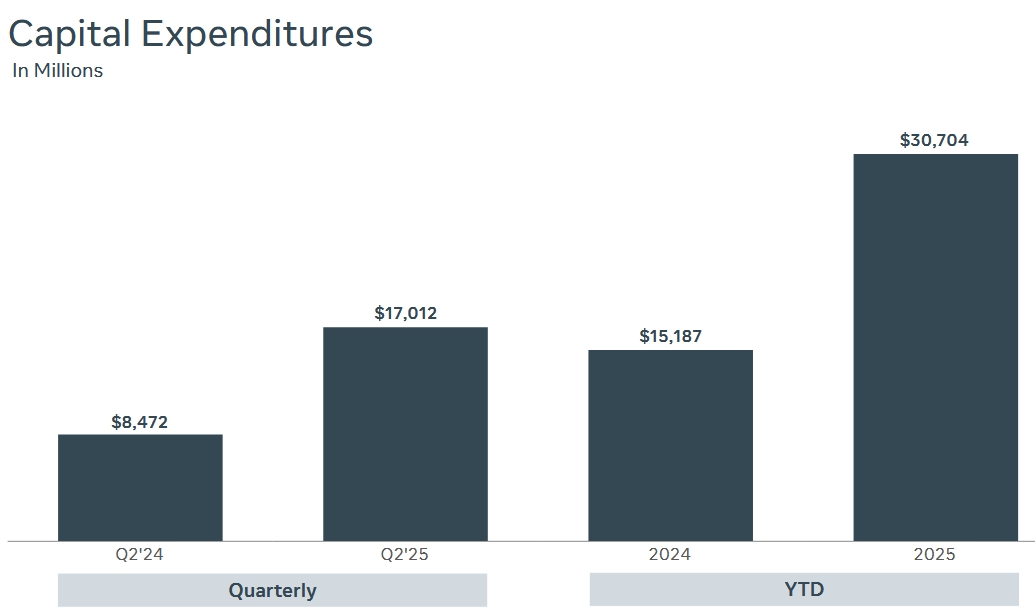

Capex Hikes Continue Unabated

After raising capex guidance twice in the first half, analysts expect Meta to raise it again during the Q3 call to support its ambitious AI strategy.

In Q2, Meta increased its 2025 capex forecast from $64–72B to $66–72B, and signaled that 2026 spending will remain significantly elevated.

First-half capex reached $30.7 billion — more than double the same period in 2024. Wall Street projects 2026 capex at $96.97 billion, up 41% from current 2025 estimates.

Meta Capital Expenditures, Source: Q2 2025 Earnings Report

With continued heavy investment in AI infrastructure, Bank of America expects Meta to raise the 2025 capex floor by $20 billion, bringing the range to $68–72 billion.

Zuckerberg has said he’d rather “overspend than underinvest” in AI, stating that some companies may be overbuilding — but all investors are making rational choices. The cost of falling behind is missing the most important tech wave in 10–15 years.

Recent moves underscore this commitment:

- Announced a $30 billion private financing deal — the largest in history — to fund a new data center in Louisiana

- Committed over $1.5 billion to build a 1GW data center in Texas

Company-Wide Shift to AI

Meta has been aggressively hiring top AI talent, poaching executives from OpenAI and even Apple.

This month, Bloomberg reported that a senior Apple executive leading AI search development will join Meta. There are also reports that metaverse leaders are being reassigned to AI teams.

While these shifts won’t appear directly in Q3 financials, they shape investor sentiment around Meta’s strategic direction.

BofA’s Post said that updates on Meta’s AI outlook will be central to the earnings call — and critical for investor sentiment.

Can Meta Return to All-Time Highs?

Meta stock hit an all-time high after its Q2 earnings, but has since pulled back about 2% — while the S&P 500, Nasdaq, and Dow have all set new highs. Year-to-date, Meta shares are up 28%.

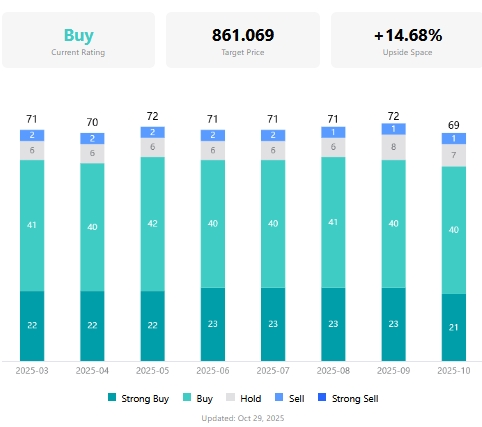

Per TradingKey, the average analyst target price is $861.07, implying about 15% upside. Among 69 analysts, only one rates “Sell”, and over 88% recommend “Buy.”

Meta Price Targets & Ratings, Source: TradingKey

Ahead of earnings:

- Evercore maintains a $930 target

- Bank of America and Seaport Global: $900

- Highest target: $1,086

In the past four quarters, Meta’s stock rose three times after earnings — including a +11% surge after Q2’s beat.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.