U.S. Q2 GDP Commentary: Unsustainable Growth Rebound, What’s Next for the Stock Market?

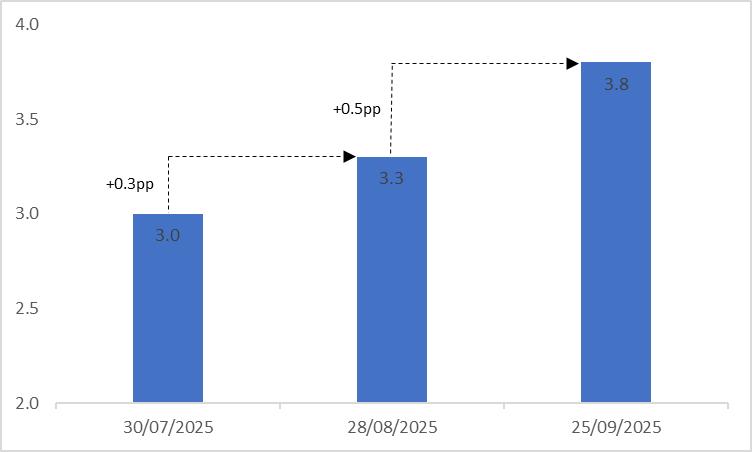

TradingKey - On 25 September 2025, the U.S. released the final Q2 GDP data. The data showed that the annualised quarter-on-quarter real GDP growth rate was 3.8%, surpassing the preliminary estimates of 3% in July and 3.3% in August. The upward revision was primarily driven by stronger-than-expected consumer spending and an increase in net exports due to the fading impact of the import rush.

Looking ahead, given the mixed signals from current high-frequency data, we expect the robust economic growth rebound in Q2 to be unsustainable. However, the likelihood of the economy slipping into a recession remains very low. Therefore, we anticipate a gradual slowdown in U.S. economic growth. On the stock market front, the current rate-cutting cycle is characterised as a preventive measure. Historical data show that preventive interest rate cuts have a relatively high probability of driving the U.S. stock market higher. Combined with supportive fiscal policies centred on tax cuts, we believe the U.S. stock market is likely to maintain an upward trend over the next 12 months.

Source: Mitrade

Main Body

On 25 September 2025, the U.S. released the final Q2 GDP data. The figure indicates that the annualised quarter-on-quarter real GDP growth rate reached 3.8%, exceeding the preliminary estimates of 3% in July and 3.3% in August (Figure 1). This upward revision was mainly attributed to consumer spending surpassing expectations with a 2.5% increase, driven particularly by a 2.6% rise in services expenditure.

Figure 1: U.S. Initial and Final Estimates of Q2 Real Annualised GDP (%, q-o-q)

Source: Refinitiv, TradingKey

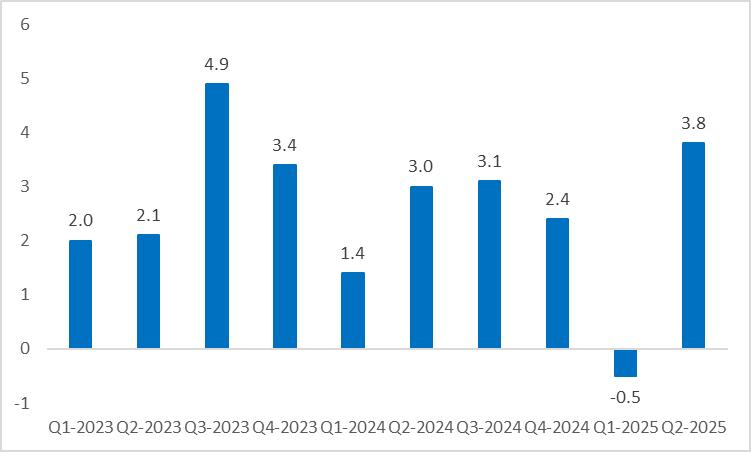

In Q1, real GDP recorded a contraction of -0.5%, largely due to an import rush by U.S. businesses in response to tariff policies following Trump's election. As the import rush effect subsided, net exports increased, leading to a significant rebound in Q2 GDP growth (Figure 2).

Figure 2: U.S. Real Annualised GDP (%, q-o-q)

Source: Refinitiv, TradingKey

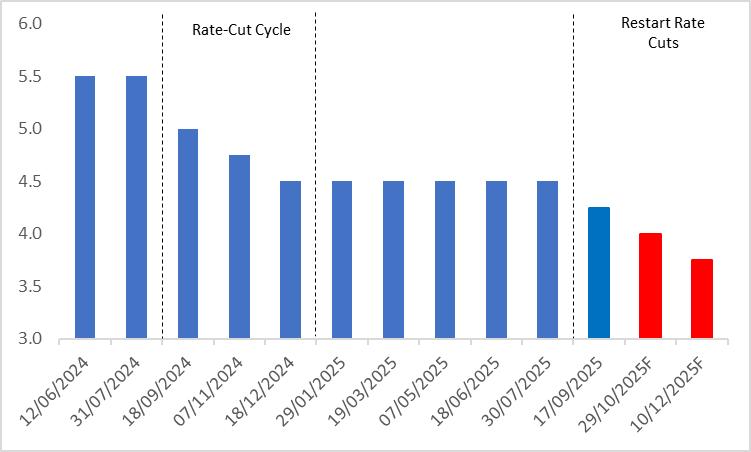

Looking ahead, the U.S. economy will encounter both supportive and challenging factors. On the positive side, while inflation has shown signs of rising, it remains within a manageable range, allowing the Federal Reserve to maintain an accommodative monetary policy. Following the initial rate cut on 17 September, we anticipate two additional rate cuts of 25 basis points each within this year (Figure 3). This accommodative policy is expected to continue injecting liquidity into U.S. markets, supporting economic growth.

Figure 3: Fed Policy Rate (%)

Source: Refinitiv, TradingKey

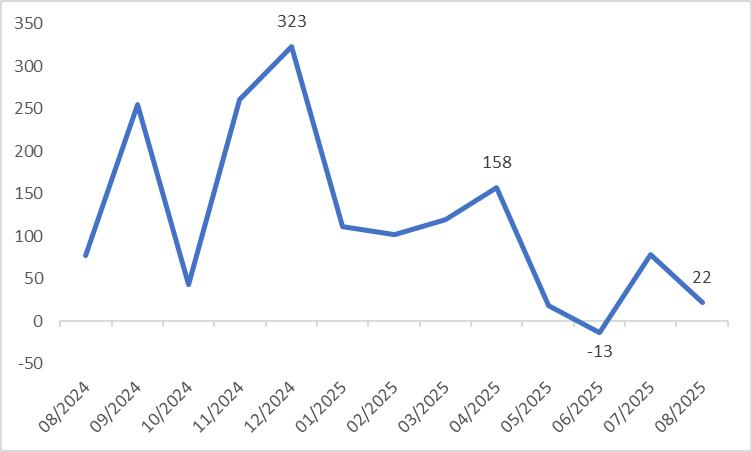

On the negative side, persistent weakness in the U.S. labour market casts a shadow over the economy. Since the end of last year, non-farm payrolls have been consistently declining, with multiple months of downward revisions, including negative job growth in June (Figure 4). Concurrently, the latest PMI data for both manufacturing and services sectors show a downward trend, signalling ongoing weakness in the supply side.

Figure 4: U.S. Nonfarm Payrolls (000)

Source: Refinitiv, TradingKey

Given the mixed signals from high-frequency data, we expect the strong Q2 economic growth rebound to be unsustainable. However, the likelihood of a recession remains very low. Therefore, we anticipate a gradual slowdown in U.S. economic growth. From a stock market perspective, the current rate-cutting cycle is preventive in nature, and historical data indicate a high probability of U.S. stock market gains during such cycles. Combined with supportive fiscal policies centred on tax cuts, we project that the U.S. stock market is likely to maintain an upward trajectory over the next 12 months.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.