U.S. July PCE and Q2 GDP Commentary: Core Inflation Remains the Key Focus for the U.S. Stock Market Outlook

TradingKey - On 28–29 August 2025, the U.S. released inflation and growth data. The July headline PCE rose by 0.2% month-over-month and 2.6% year-over-year, while core PCE increased by 0.3% month-over-month and 2.9% year-over-year, both aligning with market expectations. On the growth front, the second-quarter annualised real GDP growth rate was revised upward from an initial 3% to 3.3%.

For the U.S. stock market outlook, we believe that core inflation data will be the primary focus in the short term (0–6 months). With the Federal Reserve's interest rate currently at a high of 4.5%, even if the U.S. economy continues to slow, this elevated rate level provides the Fed with ample monetary policy tools to stabilise markets. Assuming the U.S. economy avoids a recession, the positive impact of the Fed’s potential monetary easing on U.S. stocks is expected to outweigh the negative effects of an economic slowdown, thereby driving continued upward momentum in the stock market.

However, the primary factor that could prevent the Federal Reserve from cutting interest rates is persistent high inflation. If core PCE increases exceed expectations in the coming months, limiting the Fed's ability to ease monetary policy, the U.S. stock market could face downside risks. But based on current conditions, with smooth progress in trade negotiations between the U.S. and its partners, the impact of tariff policies on PCE is expected to remain limited. As a result, reflationary pressures after August are likely to be relatively mild.

Looking ahead, with limited reflationary pressures in the U.S., the Fed is almost certain to resume its rate-cutting cycle in September. From a stock market perspective, the combination of accommodative monetary policy (rate cuts), supportive fiscal measures (tax reductions), and continued economic resilience underpins our bullish outlook for the U.S. stock market in the short term.

Source: Mitrade

Main Body

On 28–29 August 2025, the U.S. released July PCE data and revised second-quarter GDP figures. The data showed that July headline PCE rose by 0.2% month-over-month and 2.6% year-over-year, while core PCE increased by 0.3% month-over-month and 2.9% year-over-year, both in line with market expectations. On the growth front, the second-quarter annualised real GDP growth rate was revised upward from an initial 3% to 3.3%, surpassing the expected 3.1% (Figure 1).

Figure 1: Market Consensus Forecasts vs. Actual Data

Source: Refinitiv, TradingKey

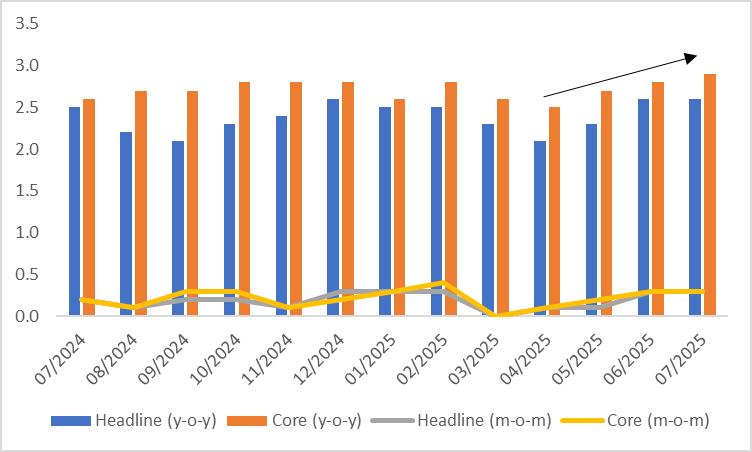

The July core PCE year-over-year increase rose slightly by 0.1 percentage points compared to June, indicating that tariffs have begun to exert some influence on U.S. price levels (Figure 2). For the U.S. stock market outlook, we believe that core inflation data will remain the primary focus in the short term (0–6 months). With the Federal Reserve's interest rate currently at a high of 4.5%, even if the U.S. economy continues to slow, this elevated rate level provides the Fed with ample monetary policy tools to support markets. Assuming the U.S. economy avoids a recession (a most likely scenario), the positive impact of the Fed’s potential monetary easing on U.S. stocks is expected to outweigh the negative effects of an economic slowdown, thereby driving continued upward momentum in the stock market.

The primary factor that could delay Federal Reserve rate cuts is persistent high inflation. If inflation, particularly core PCE, exceeds expectations in the coming months, thereby constraining the Fed's ability to lower rates, the U.S. stock market may face downward pressure. However, based on current developments, with trade negotiations between the U.S. and its partners progressing smoothly, the impact of tariff policies on PCE is expected to remain limited. Consequently, reflationary pressures after August are likely to be relatively subdued.

Figure 2: U.S. PCE (%)

Source: Refinitiv, TradingKey

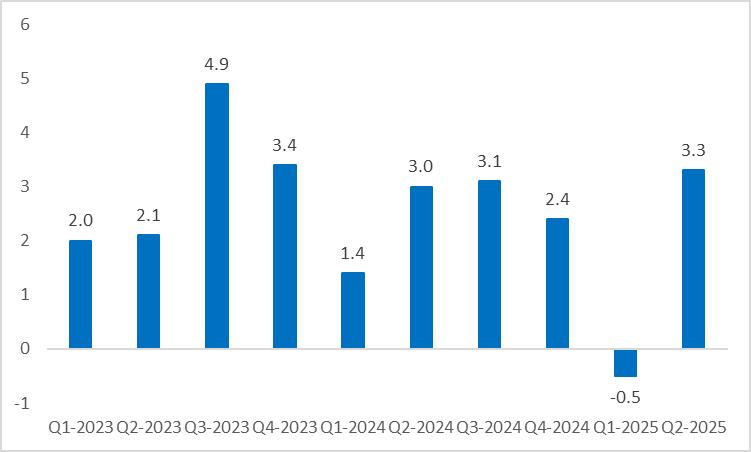

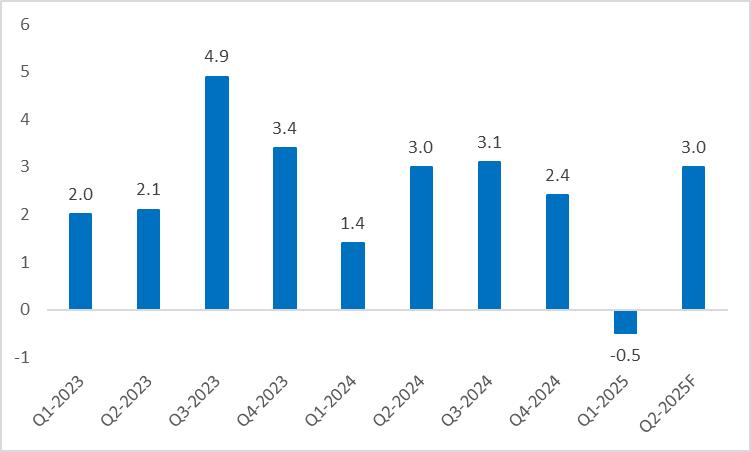

The upward revision of GDP by 0.3 percentage points was driven by two key factors. First, robust business investment significantly boosted investment growth from an initial 1.9% to 5.7%. Second, following the dissipation of the first-quarter "import rush" effect, net exports in the second quarter contributed approximately 5% to GDP, marking a historical high. However, consumer spending, a core driver of the economy, grew at a modest rate of 1.6%. Despite this, the U.S. economy continues to demonstrate resilience, and the slowdown in real GDP growth for the second half of the year is expected to be less pronounced than anticipated.

Figure 3: U.S. Real Annualised GDP (%, q-o-q)

Source: Refinitiv, TradingKey

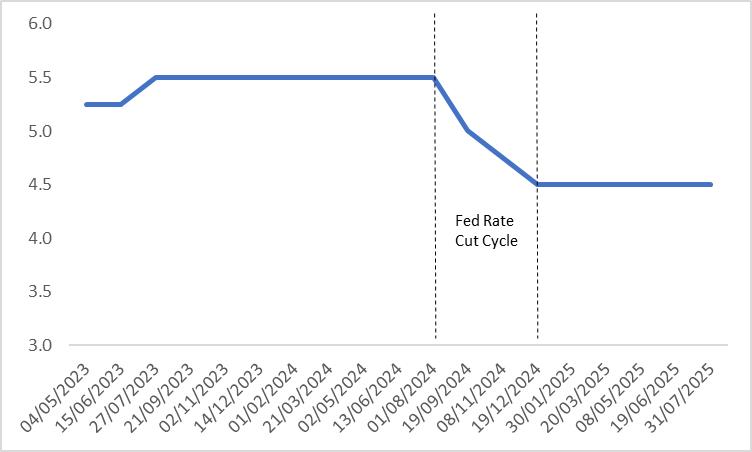

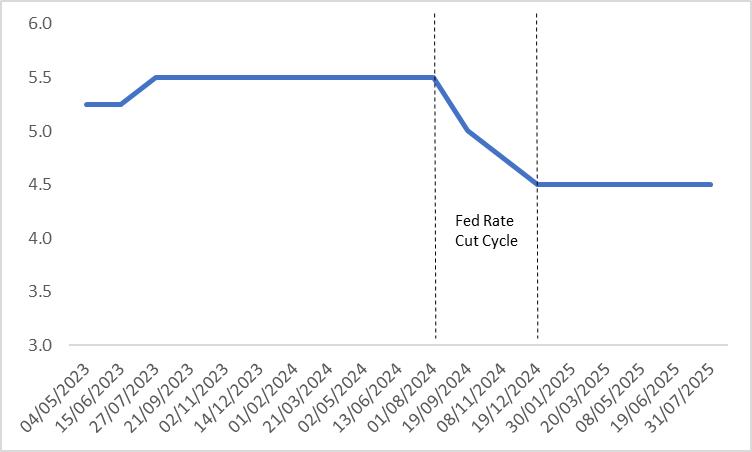

Looking ahead, with limited reflationary pressures in the U.S., the Fed is almost certain to resume its rate-cutting cycle in September (Figure 4). From a stock market perspective, the combination of accommodative monetary policy (rate cuts), supportive fiscal measures (tax reductions), and sustained economic resilience underpins our continued bullish outlook for the U.S. stock market.

Figure 4: Fed Policy Rate (%)

Source: Refinitiv, TradingKey

U.S. July PCE and Q2 GDP Preview: With Rate Cuts Looming, Will U.S. Stocks Continue to Rise?

TradingKey - On 28-29 August 2025, the U.S. will release July PCE and Q2 GDP data. Market expectations suggest both headline and core PCE will rise 0.3% month-over-month, consistent with June figures. For growth, in line with the preliminary estimate on 30 July, the revised Q2 annualised real GDP growth rate is expected to remain at 3%.

Although July PCE is expected to remain elevated, looking ahead, the impact of tariff policies on PCE is likely to be less severe than market expectations, given smooth negotiation progress. While Q2 GDP is projected to show a significant rebound, this is largely due to a recovery in net exports driven by the reduced import rush in Q1. Given the unsustainability of this phenomenon, the broader trend of a slowing U.S. economy is expected to persist unchanged.

Looking forward, with limited reflation in the U.S. and ongoing economic slowdown, the Federal Reserve is highly likely to resume its rate-cutting cycle in September. Regarding the stock market, supported by accommodative monetary policy and reinforcing fiscal measures—such as rate cuts and tax reductions—we maintain a bullish outlook on U.S. equities.

Source: Mitrade

Main Body

On 28-29 August 2025, the U.S. will release July PCE and Q2 GDP data. Market consensus anticipates both headline and core PCE to increase by 0.3% month-over-month, unchanged from June. On the growth front, consistent with the preliminary estimate on 30 July, the revised Q2 annualised real GDP growth rate is expected to remain at 3% (Figure 1).

Figure 1: Market Consensus Forecasts

Source: Refinitiv, TradingKey

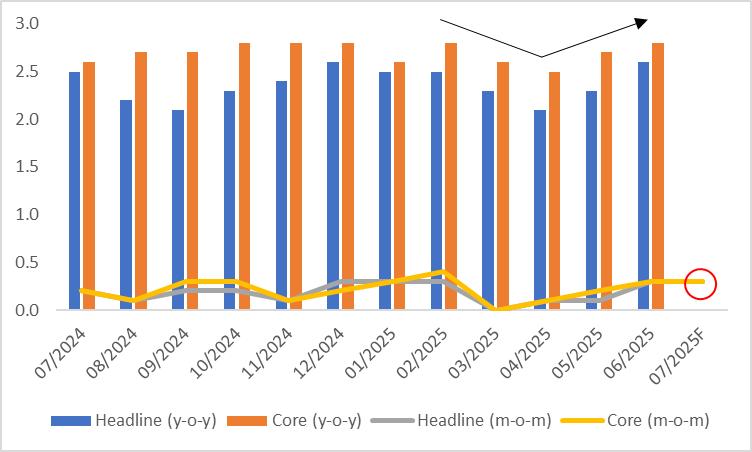

U.S. PCE data, after bottoming out in March, began to rebound starting in April (Figure 2). Specifically, both headline and core PCE rose from zero growth in March to 0.3% in June. July PCE is expected to remain elevated, primarily due to persistent inflationary pressures from tariffs, despite progress in related negotiations. Looking ahead, we believe that with ongoing successful negotiations, the impact of tariff policies on PCE will be less severe than market expectations, and reflationary pressures are likely to moderate after August.

Figure 2: U.S. PCE (%)

Source: Refinitiv, TradingKey

Both the initial estimate on 30 July and the projected revision on 28 August indicate that Q2 GDP will shift from negative to positive, reflecting a significant rebound (Figure 3). The primary driver of this change is a notable recovery in net exports. Specifically, during Q1, a large-scale import rush led to a substantial trade deficit, which was the main cause of negative GDP growth. In Q2, smoother progress in tariff negotiations reduced import rush activities, resulting in a significant increase in real GDP growth. However, this rebound does not signify an improvement in the intrinsic growth momentum of the U.S. economy. Looking ahead, we believe the broader trend of a slowing U.S. economy remains unchanged.

Figure 3: U.S. Real Annualised GDP (%, q-o-q)

Source: Refinitiv, TradingKey

Looking ahead, given the limited scope of U.S. reflation and ongoing economic slowdown, the Federal Reserve is highly likely to resume its rate-cutting cycle in September (Figure 4). In the stock market, supported by accommodative monetary policy combined with reinforcing fiscal measures—such as interest rate cuts and tax reductions—we maintain a bullish outlook on U.S. equities.

Figure 4: Fed Policy Rate (%)

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.