Powell’s Hill Testimony Preview: Patience First, Divergence to Be Addressed – Why a More Hawkish Stance?

TradingKey - After the Federal Reserve’s June policy meeting, which signaled a more hawkish rate outlook and rising stagflation risks, market attention now turns to Chair Jerome Powell’s two-day testimony on Capitol Hill, where he will defend the Fed’s reluctance to cut rates soon and its view that inflation could rise significantly in the coming months.

As scheduled, Powell will present the Federal Reserve’s semiannual monetary policy report and testify before the House Committee on Financial Services on Tuesday (June 24) and the Senate Committee on Banking, Housing, and Urban Affairs on Wednesday. He is expected to face tough questions from lawmakers regarding the rationale behind current monetary policy.

According to Bloomberg, Powell may emphasize that while rate cuts are still possible this year, policymakers want more clarity on how trade policies from the White House — particularly Trump tariffs — will impact the economy before taking action.

Inflation Signals Are Mixed – Tariffs Not Just a One-Time Shock

Following last week’s FOMC meeting, members of the Federal Open Market Committee (FOMC) took a more cautious stance toward further rate cuts. Although the dot plot maintained the expectation for 50 basis points of rate cuts in 2025, the number of officials expecting two cuts decreased, while those anticipating no cuts at all increased from 4 to 7.

The updated Summary of Economic Projections (SEP) showed:

- 2025 GDP growth forecast downgraded by 0.3 percentage points to 1.4%

- Unemployment rate revised upward by 0.1 percentage point to 4.5%

- PCE inflation projection raised by 0.3 percentage points to 3.0%

According to the semiannual monetary policy report submitted to Congress last Friday, policymakers believe U.S. inflation has edged higher. While short-term inflation expectations have risen sharply this year — reflecting concerns over tariffs — most long-term inflation indicators remain within pre-pandemic ranges, broadly consistent with the FOMC’s long-term goals.

However, the report also noted that due to evolving trade policies, the impact of higher import tariffs on consumer prices remains highly uncertain, and it's too early to assess how households and businesses will respond.

It added that while official price data does not directly reflect tariff effects, recent patterns across goods categories suggest that tariffs are likely contributing to the recent rise in goods inflation.

At his post-meeting press conference, Powell emphasized that inflation is expected to rise meaningfully in the coming months, as some initial impacts have already been observed. However, he said it remains unclear whether these increases represent only one-time shocks.

Labor Market Moving Toward Balance

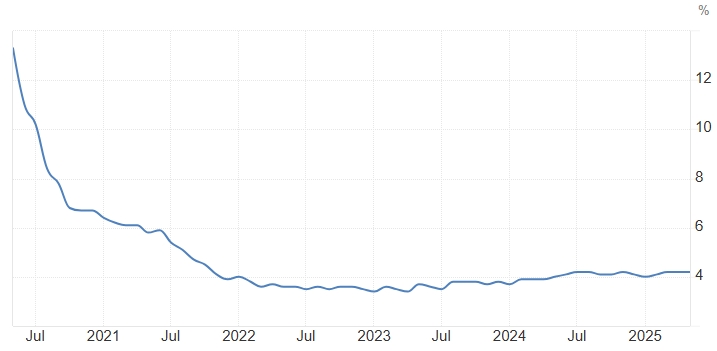

The semiannual report described the U.S. labor market as healthy and balanced. The unemployment rate remained at 4.2% in May, holding relatively steady since mid-2024 — a historically low level.

United States Unemployment Rate, Source: Trading Economics

The report also pointed out that labor supply growth has slowed compared to previous years, partly due to a notable decline in immigration since mid-2024 and a slight drop in labor force participation. As demand for labor has weakened gradually in recent years, multiple indicators suggest that the job market has moved toward balance and is currently less tight than before the pandemic.

In a recent statement, Powell said that key labor market indicators — including participation, wage growth, and job creation — remain solid, with no clear signs of distress. In his view, the labor market does not yet call for rate cuts.

Growing Policy Divergence Within the Fed

There is increasing public divergence among Fed officials over whether to continue focusing on inflation risks or accelerate rate cuts.

Fed Governor Christopher Waller argued that the inflationary impact of tariffs might be temporary, and that there were some worrying signs in the labor market, supporting the case for a potential July rate cut to prevent a sharper downturn.

Tom Barkin, President of the Richmond Fed, countered that inflation remains above the 2% target, trade policy debates are ongoing, and the unemployment rate remains low at 4.2%, suggesting there is "no urgency to act."

Jerome Powell last week said that given the uncertainty surrounding trade policy and the fact that many key decisions are still pending, no single view should be overemphasized at this stage.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.