[HOTSPOT ANALYSIS] ECB June Policy Rate Commentary: Euro Dynamics Driven by the Fed, Not the ECB

TradingKey - On 5 June 2025, the European Central Bank (ECB) met market expectations by reducing interest rates by 25 basis points, bringing the deposit facility rate to 2%. This decision was driven by two key factors: first, the sustained decline in Eurozone inflationary pressures; second, the persistently weak economic recovery. Moving forward, heightened uncertainties stemming from Trump’s tariff policies and potential EU retaliatory measures are likely to prompt the ECB to adopt a more cautious monetary policy stance. We anticipate that the ECB may halt its rate-cutting cycle in the near term. Conversely, in the United States, subdued economic growth is expected to limit inflationary pressures, leading the Federal Reserve to restart its rate-cutting cycle. This convergence of US and Eurozone interest rates is poised to support a stronger EUR/USD exchange rate.

Source: TradingKey

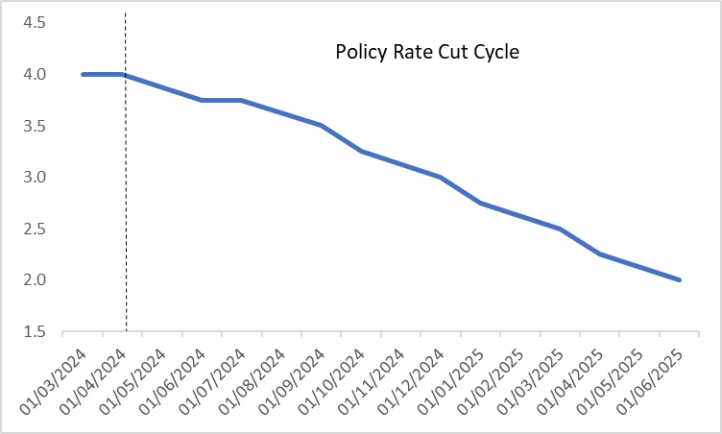

On 5 June 2025, the European Central Bank (ECB) released its latest monetary policy decision. In line with market expectations, the ECB reduced interest rates by 25 basis points, setting the deposit facility rate at 2%, the main refinancing operations rate at 2.15%, and the marginal lending facility rate at 2.4% (Figure 1). This represents the eighth rate cut in the current cycle (Figure 2). Furthermore, since March, the ECB has halted reinvestment of principal from maturing assets under the Asset Purchase Programme (APP) and the Pandemic Emergency Purchase Programme (PEPP), leading to a steady and planned reduction in its balance sheet, signalling ongoing balance sheet reduction.

Figure 1: ECB Policy Rate

Source: Refinitiv, TradingKey

Figure 2: ECB Deposit Facility Rate (%)

Source: Refinitiv, TradingKey

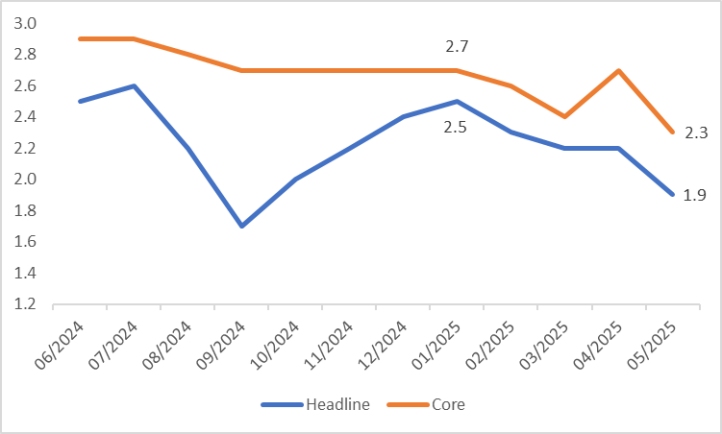

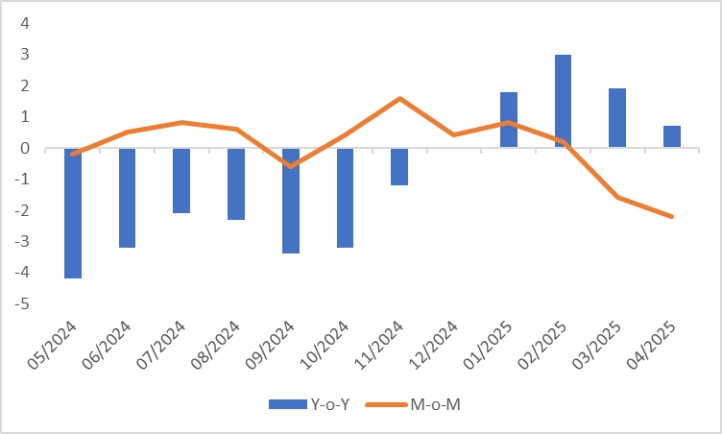

The decision to cut rates is driven by two key factors. First, inflationary pressures in the Eurozone have been steadily subsiding. Since early 2025, the Consumer Price Index (CPI) has fallen from a high of 2.5% to 1.9% in May (Figure 3). Furthermore, over the past year, the Producer Price Index (PPI) has hovered around zero month-on-month, with year-on-year figures declining for two consecutive months (Figure 4). Should this PPI trend continue to influence the CPI, the Eurozone is likely to experience a sustained period of moderate inflation. In light of current economic conditions, the ECB recently revised its inflation projections downward, forecasting 2% for 2025 and 1.6% for 2026 (Figure 5).

Figure 3: Eurozone CPI (%, y-o-y)

Source: Refinitiv, TradingKey

Figure 4: Eurozone PPI (%)

Source: Refinitiv, TradingKey

Figure 5: ECB CPI Forecasts

Source: Refinitiv, TradingKey

Second, the Eurozone's economic recovery remains weak. Real GDP growth in the first quarter of 2025 reached 1.5% year-on-year, an improvement from 1.2% in the fourth quarter of 2024, largely driven by European firms accelerating exports in response to U.S. tariff pressures. However, high-frequency indicators, particularly in production, reveal ongoing economic weakness. May 2025 data showed Manufacturing, Construction, and Services PMIs at 49.4, 45.6, and 49.7, respectively, all remaining below the 50 expansion-contraction threshold. The combination of low inflation and a sluggish recovery justifies the ECB's decision to cut rates.

Looking forward, on the growth front, Trump’s tariff policies toward the EU are fraught with uncertainty. On the inflation front, the EU’s retaliatory measures against the US remain unpredictable due to their dependence on evolving US foreign policy. Consequently, the ECB is likely to adopt a cautious, incremental approach to monetary policy, often described as “one step at a time”. This prudence leads us to anticipate that the ECB may halt its rate-cutting cycle in the near term. Conversely, in the US, the tariff-driven economic slowdown is expected to persist. While tariffs could elevate supply-side costs, a weakening economy and subdued domestic demand are likely to prevent a strong inflationary resurgence. Against this backdrop of moderate inflation, the Federal Reserve is projected to restart its rate-cutting cycle. As a result, the interest rate differential between the US and the Eurozone is expected to narrow, supporting a stronger EUR/USD exchange rate.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.