U.S. Manufacturing Revival and a Softening Dollar: Why Commodity ETFs Could Be the Next Investment Frontier

1. Background Overview

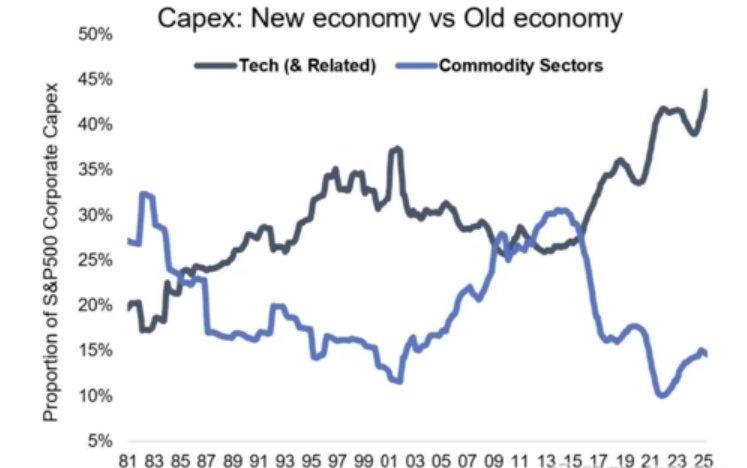

TradingKey - Contrasting sharply with the current surge in US AI&technology investments, traditional manufacturing is languishing, accompanied by widespread avoidance of commodities. Over the past 45 years, capital expenditure has consistently surged in technology-driven new economy sectors, while spending on traditional commodity-based industries has remained subdued. Within the S&P 500, capital investment in commodity sectors has fallen below 15%, marking a 45-year low, especially since 2013.

Data Sources: LSEG, TradingKey As of: August 21, 2025

This paradigm shift stems fundamentally from globalization and the international division of labor over recent decades. The US has evolved into the world’s largest consumer market, while manufacturing hubs have shifted largely to Asian countries such as China, Vietnam, and India. China, in particular, has become a dominant consumer of raw materials like iron ore, crude oil, and copper.

However, the one constant is change. Multiple signals now indicate this global trend is reversing. Rising geopolitical tensions, breakdowns in trade systems, and a surge in nationalism all point to the advent of deglobalization. Whether acknowledged or not, this shift signals a new era where “competition and security” supplant “peace and development” as prevailing themes. As countries decouple from global supply chains for security and stability, they are striving to build autonomous supply networks. This transition forecasts rising commodity volumes and inflation, challenging sovereign credit and monetary systems—particularly in the context of mounting debt and growing fiscal deficits.

2. Investment Value Analysis

2.1 Macro Drivers

The probability of a pivot in monetary policy this year has surged, especially amid distortions in the labor market, reinforcing market expectations. Interest rate futures now price in over a 90% chance of a 25 basis point cut in September, with some possibility of an immediate 50 basis point cut. Although Fed Chair Jerome Powell might continue to resist easing on the grounds of persistent inflation risks, the upcoming appointment of a new Fed Chair—heavily influenced by President Trump—could decisively shift market sentiment.

From a longer-term perspective, this suggests a sustained depreciation of the US dollar, with the year-to-date decline merely a “warm-up.” Consequently, dollar-denominated commodities are positioned to gain from this trend, underpinning expectations of prolonged price appreciation.

2.2 Policy Support

Unlike the Democratic Party and President Biden’s administration, Trump is not a proponent of technology and new energy sectors. Regardless of motives, he has consistently championed reshoring US manufacturing and bolstering traditional energy industries. Since taking office, Trump repealed the “Clean Energy Act" and vigorously pushed for the passage of the “OBBB” Act (details can be found in related analyses — “Investment Plays to Watch as ‘The One, Big, Beautiful Bill’ Clears Congress”).

Under this legislation, the Trump administration plans to phase out tax credits for new energy, while aggressively reviving traditional energy production. Beyond tax breaks for coal, oil, and natural gas, substantial support and preferential tax treatment have been extended to nuclear power investments and infrastructure projects. Large-scale infrastructure spending and investment plans are set to create significant incremental demand for traditional energy and industrial metals.

2.3 Geopolitical Dynamics

Amid the broader trend of deglobalization, economies are motivated by security and stability concerns to develop controllable, localized supply chains. Trade tensions ignited by the Trump administration have elevated resource competition to a core national strategic priority. For instance, China’s dominance over rare earth elements constrains industrial production in Western economies. Moving forward, raw materials such as copper, iron ore, lithium, and rare earth metals will receive heightened strategic focus, marking a new phase in sovereign competition for mineral resources.

3. Classification of Commodities and Corresponding ETFs

The third part of this article is mainly to help investors sort out how to invest in the sub-categories of commodities and the corresponding specific product ETFs.

Commodities are generally categorized based on their use and characteristics into the following major groups:

- Energy: Core to energy supply, serving as the fundamental driver of industrial production and economic activity. Key commodities include crude oil (WTI, Brent), natural gas, coal, gasoline, and diesel.

- Industrial Metals: Widely used in manufacturing, construction, and new energy sectors, with demand highly sensitive to economic cycles. Primary metals include copper , aluminum, zinc, lead, nickel, tin, and iron ore.

- Precious Metals: Possessing monetary, safe-haven, and industrial attributes, precious metals exhibit clear inflation-hedging traits. The main metals are gold, silver, platinum, and palladium.

- Agricultural Products: Used primarily in food processing and animal feed, agricultural commodities are highly influenced by natural conditions, with relatively inelastic demand. Key products include grains, oilseeds, and soft commodities.

Given the diversity of subcategories and their variegated supply-demand dynamics, commodity prices outside of gold have performed poorly over the past three years. Such steep cyclical divergences are typically corrected over time. The following highlights the three principal commodity groups alongside their most relevant ETFs, which stand to benefit directly from the recent downward shift in nominal interest rates and show potential for entering an upward price trajectory.

.jpg)

Data Sources: LSEG, TradingKey As of: August 21, 2025

3.1 Rare Metals

SPDR® Gold Shares ETF (GLD)

Launched on November 18, 2004, and managed by the World Gold Trust, GLD is the largest physically-backed gold ETF globally. The fund invests exclusively in physical gold, aiming to track the price of gold closely. With total assets exceeding 35billion, daily trading volume frequently surpasses 1 billion. Although GLD’s expense ratio is slightly higher than some gold trust ETFs, its liquidity and scale make it a preferred choice for most investors.

Investment Rationale: Gold prices have performed strongly over the past two years amid geopolitical conflicts and debt and credit risks. With interest rates poised to fall and a persistently weakening US dollar compounded by rising federal debt, demand for gold as a portfolio hedge is unlikely to wane—on the contrary, it is expected to increase.

iShares Silver Trust ETF (SLV)

Introduced by BlackRock’s iShares on April 21, 2006, SLV is the world’s largest silver ETF. It holds physical silver, tracking the London Bullion Market Association (LBMA) silver price, providing full transparency of its underlying assets. The fund manages approximately $17.5 billion in assets with an expense ratio of 0.5%. While SLV’s fees are somewhat higher than competitors like SIVR (0.3%), its significant scale and liquidity leadership outweigh this drawback.

Investment Rationale: Despite silver’s industrial usage and close ties to the US manufacturing sector—currently weakened by sluggish new energy production—the gap between gold and silver prices has widened considerably. As the Fed eases monetary policy, silver’s risk mitigation and inflation-hedging properties should strengthen, suggesting considerable recovery potential relative to gold.

3.2 Traditional Energy

Energy Select Sector SPDR® Fund ETF (XLE)

Managed by State Street Global Advisors and launched on December 16, 1998, XLE tracks the energy sector in the S&P 500. It encompasses oil, natural gas, consumable fuels, and energy equipment and services companies. As of December 31, 2024, XLE’s assets under management (AUM) stood at $33.5 billion with a low expense ratio of 0.09%.

The ETF boasts high market liquidity, offering convenient trading conditions for investors. Its top five holdings are ExxonMobil, Chevron, ConocoPhillips, EOG Resources, and Williams Companies—America’s leading integrated energy firms operating across exploration, production, refining, and sales. These companies benefit directly from rising crude oil and natural gas prices.

Investment Rationale: Traditional energies like oil and gas remain foundational to the global economy, with prices influenced by geopolitical developments, global growth trajectories, and supply-demand shifts. Current international oil prices hover near US shale producers’ breakeven levels. Against the backdrop of easing monetary policies and anticipated inflation rebound, commodity prices face upward pressure, making sustained price declines unlikely.

3.3 Industrial Metals

SPDR® S&P Metals and Mining ETF (XME)

Also managed by State Street Global Advisors, XME invests in companies listed in the S&P Metals and Mining Select Industry Index. Its holdings cover businesses involved in metal and mineral extraction and production, including aluminum, coal, copper, diversified metals and mining, gold, precious metals and minerals, silver, and steel.

As of August 20, 2025, XME had a market capitalization of $2.14 billion, charging a 0.35% management fee. The ETF holds 32 stocks, with top positions in MP Materials, Uranium Energy, Cleveland-Cliffs, Warrior Met Coal, and Coeur Mining. Its portfolio spans rare earth elements to uranium and a broad range of industrial metals, positioning it to benefit significantly from rising commodity prices in a rate-cutting environment.

Investment Rationale: Industrial metals demand correlates closely with economic activity. Amid the ongoing US-China strategic competition, resources like rare earths and lithium have become critical. Fed rate cuts reduce financing costs and stimulate credit growth, while infrastructure spending under the “Build Back Better” framework supports corporate investment and consumption—factors likely to boost demand for industrial metals such as copper and aluminum.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.