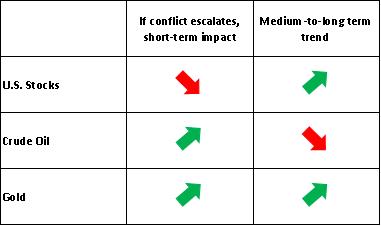

[IN-DEPTH ANALYSIS] Iran–Israel Conflict: Investment Opportunities in U.S. Stocks, Crude Oil, and Gold if Tensions Escalate

Executive Summary

TradingKey - On 13 June, Israel launched large-scale airstrikes on Iran, prompting swift retaliatory actions from Iran. Should the Iran-Israel conflict escalate further, potentially leading to extreme scenarios like the closure of the Strait of Hormuz, U.S. stocks are expected to decline in the short term, while crude oil and gold prices are likely to surge. However, mid-to-long-term price movements in these assets may present profitable opportunities for investors. For U.S. equities, the Federal Reserve is projected to resume interest rate cuts in July or September, complemented by expansionary fiscal policies such as domestic tax cuts. These measures are expected to outweigh the impact of the economic slowdown, reinforcing our bullish outlook for U.S. stocks in the medium term. Thus, a short-term pullback triggered by an escalating conflict could offer investors an attractive entry point. In the crude oil market, OPEC+ retains significant spare production capacity, and potential energy policies under the Trump administration could exert considerable downward pressure on oil prices. If the conflict drives a short-term spike in oil prices, increased supply-side responses could lead to a price retreat in the medium term. Investors should therefore exercise caution when chasing oil price rallies. For gold, factors such as high tariffs, substantial U.S. debt levels, and increased gold reserve accumulation by global central banks support a continued upward trajectory in prices over the medium term. Even without conflict escalation, gold prices are poised to rise due to these fundamental drivers. Should the conflict intensify, it would serve as an additional catalyst for significant gold price gains.

Source: TradingKey

* Investors can directly or indirectly invest in the stock indices, oil and gold through passive funds (such as ETFs), active funds, financial derivatives (like futures, options and swaps), CFDs and spread betting.

1. Background

Israel launched pre-emptive strikes against Iran to prevent the development of nuclear weapons. On 13 June, Israel conducted large-scale airstrikes targeting dozens of Iranian facilities linked to its nuclear program. Iran’s Supreme Leader Ayatollah Khamenei vowed a “severe response”, retaliating by launching hundreds of ballistic missiles and drones at Israeli cities, including Jerusalem, Tel Aviv, and Haifa. This black swan event triggered a sharp sell-off in risk assets, such as U.S. equities, on the same day, while crude oil and safe-haven gold prices surged significantly.

Given the unpredictability of future developments, we cannot rule out the possibility of further escalation in the Iran-Israel conflict. If Iran persists in advancing its nuclear program and both sides engage in an escalating cycle of retaliation, heightened conflict may become increasingly likely. In extreme scenarios, escalation could lead to the closure of the Strait of Hormuz and the disruption of GPS systems across the Persian Gulf, effectively halting this critical oil transportation chokepoint. As the purpose of this analysis is to highlight risks, we examine how asset prices across multiple classes would respond under a conflict escalation scenario and identify potential investment opportunities within these dynamics.

2. Impact on U.S. Equities

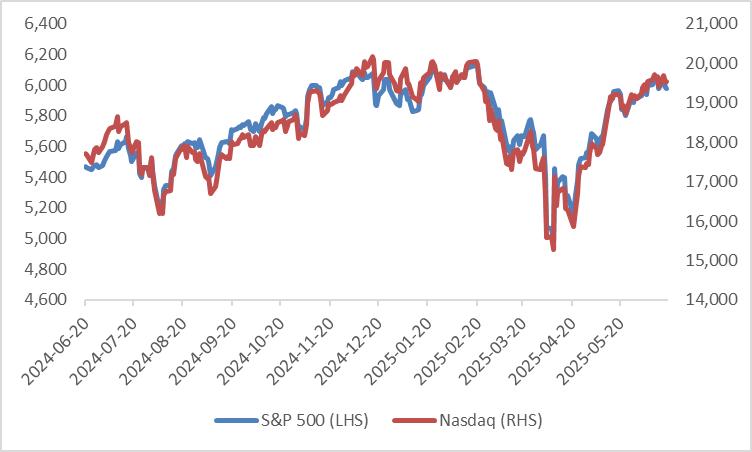

Recently, stronger-than-expected economic data, subdued signs of reflation, heightened expectations for Federal Reserve rate cuts, and easing U.S.-China trade tensions have collectively driven U.S. stock market gains. As of now, the S&P 500 and Nasdaq indices have nearly recovered all losses from the sharp decline between late February and early April (Figure 2.1). However, the Iran-Israel conflict has temporarily capped further upside in U.S. equities. Should the conflict escalate, U.S. stocks are expected to face short-term downward pressure through two primary channels: First, a conflict-driven spike in oil prices (see “Impact on Crude Oil” section below for details) could elevate U.S. inflation expectations, potentially reducing investor confidence in the extent of Federal Reserve rate cuts, which would weigh on equities. Second, sustained conflict is likely to shift investor risk preferences, prompting capital flows into safe-haven assets like gold (see “Impact on Gold” section below). This outflow of funds from equities, coupled with rising risk premiums, would constrain further market gains. Notably, while the broader U.S. stock market may face short-term declines, the energy sector could buck the trend and rise due to higher oil prices.

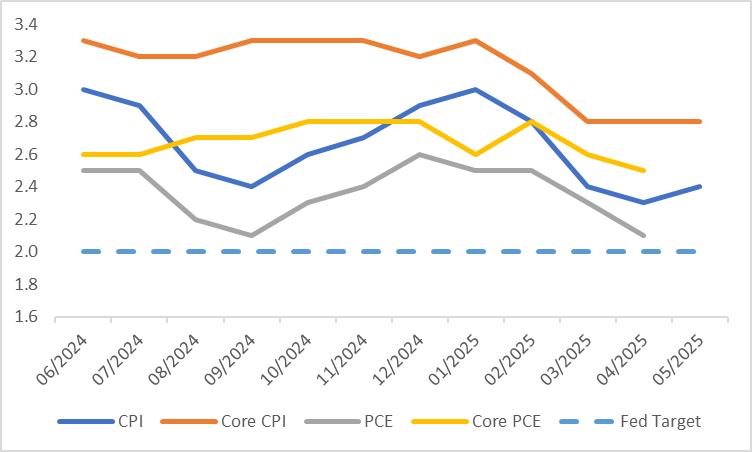

In the medium to long term, U.S. economic growth is expected to slow due to the impact of tariffs. If demand-side weakness offsets the inflationary pressures from tariffs, maintaining the downward trend in CPI and PCE (Figure 2.2), the Federal Reserve is likely to resume its rate-cutting cycle in July or September. This accommodative monetary policy, combined with expansionary fiscal measures such as domestic tax cuts, is expected to outweigh the effects of economic slowdown, reinforcing our bullish outlook for U.S. equities in the medium term. Consequently, if an escalation in the Iran-Israel conflict triggers a short-term pullback in U.S. stocks, it could present an attractive opportunity for investors to position for future gains.

Figure 2.1: U.S. Stock Indices

Source: Refinitiv, TradingKey

Figure 2.2: U.S. Inflation (%, y-o-y)

Source: Refinitiv, TradingKey

3. Impact on Crude Oil

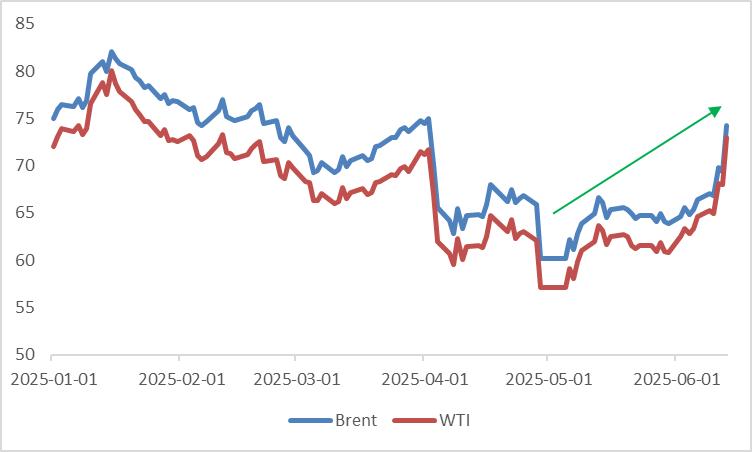

Even before the Iran-Israel conflict, crude oil prices had been trending upward since early May (Figure 3.1). This was primarily driven by the easing of U.S.-China trade tensions on 12 May and pre-emptive export activities ahead of reciprocal tariffs, which spurred a phase of oil inventory restocking. These factors increased demand for crude oil, pushing prices higher.

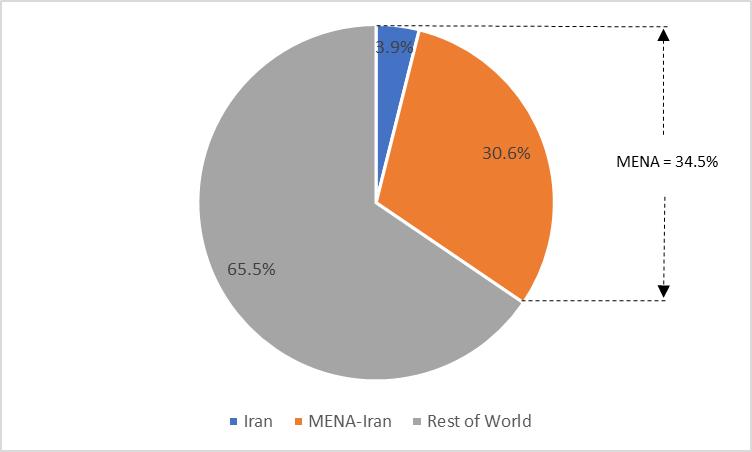

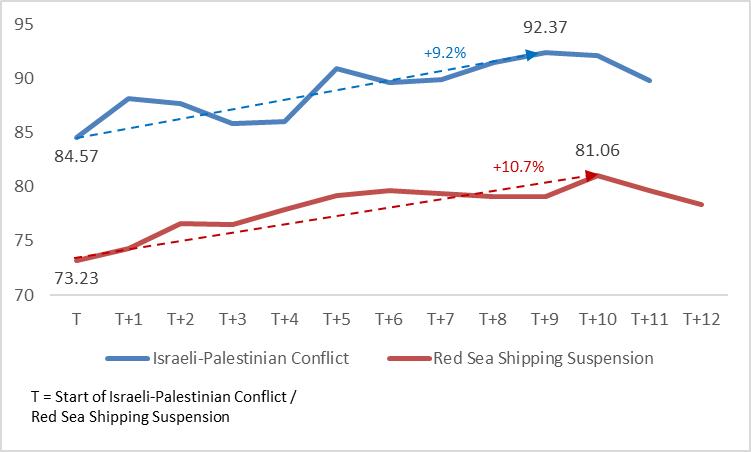

Should the Iran-Israel conflict escalate further, potentially leading to the extreme scenario of a Strait of Hormuz closure, oil prices are expected to surge significantly in the short term. Three key points merit attention: First, while Iran’s oil supply accounts for only 3.9% of global production, the Middle East and North Africa region collectively contributes 34.5% (Figure 3.2). If escalation disrupts other Gulf countries, a substantial portion of global crude supply could be constrained, driving oil prices sharply higher. Second, the likelihood of such an extreme scenario is not negligible. Prolonged international sanctions have strained Iran’s economy, undermining political stability. If the conflict worsens, the Khamenei regime’s stability could deteriorate rapidly, potentially prompting Iran to take extreme actions. Third, historically, the October 2023 Israel-Palestinian conflict pushed oil prices up by 9.2%, while the mid-December 2023 Red Sea shipping suspension caused a 10.7% increase (Figure 3.3). Should extreme circumstances arise, a closure of the Strait of Hormuz could severely disrupt oil shipments. This would likely result in an oil price increase surpassing the magnitude of prior geopolitical conflicts.

In the medium to long term, crude oil prices are expected to gradually decline due to supply-side factors. OPEC+ retains significant spare production capacity, and potential energy policies under the Trump administration could further exert downward pressure on oil prices. If the Iran-Israel conflict escalation drives a short-term spike in oil prices, increased supply-side responses are likely to contribute to a price retreat in the medium term. Therefore, investors should remain cautious when chasing oil price rallies.

Figure 3.1: Oil Prices (USD/bbl)

Source: Refinitiv, TradingKey

Figure 3.2: Oil Supply (% of global)

Source: Refinitiv, TradingKey

Figure 3.3: Oil Prices During Israeli-Palestinian Conflict and Red Sea Shipping Suspension (USD/bbl)

Source: Refinitiv, TradingKey

4. Impact on Gold

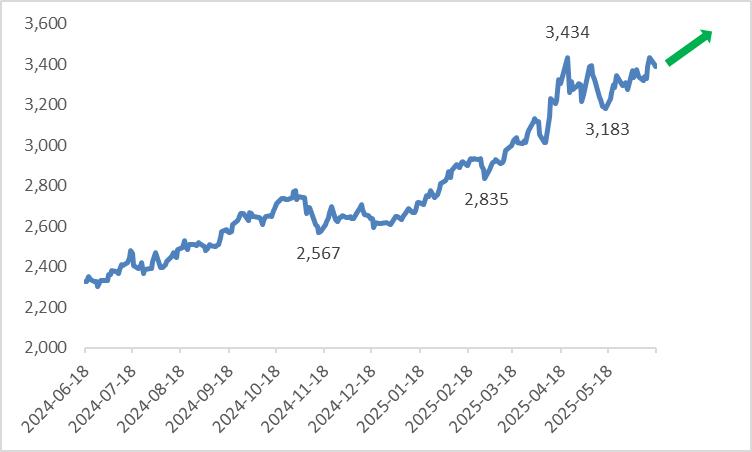

Following Israel’s airstrikes on Iran on 13 June, heightened market risk aversion drove investors to seek safe-haven assets, significantly boosting gold prices. On that day, spot gold surged above $3,400 per ounce, gaining $44 in the single day. Should the Iran-Israel conflict escalate further, gold prices are highly likely to continue rising in the short term.

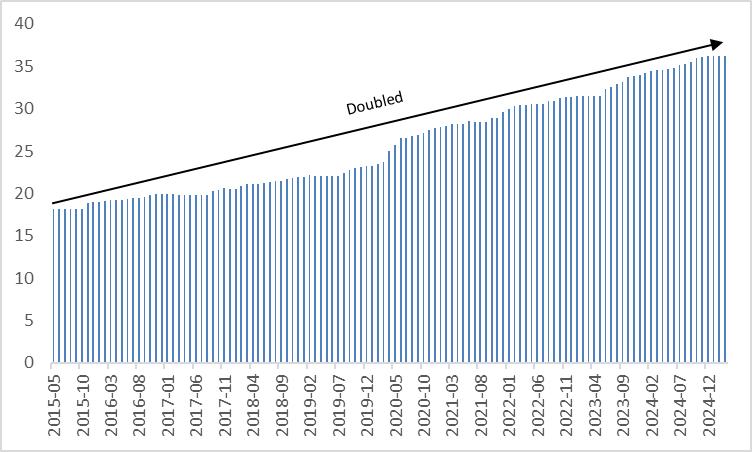

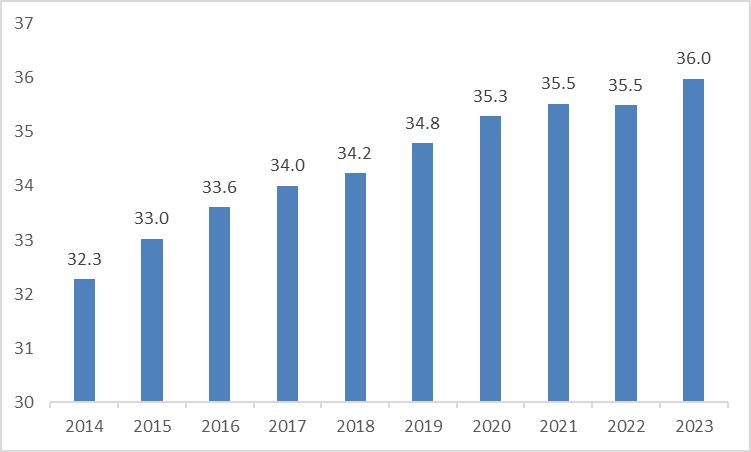

In the medium to long term, gold prices are poised for further upside (Figure 4.1), primarily driven by the sustained impact of U.S. tariffs. Tariffs are expected to dampen economic growth, highlighting gold’s safe-haven appeal during periods of economic weakness. Should high tariffs also trigger reflation, elevated inflation would reinforce gold’s role as an inflation hedge. Moreover, tariffs increase the cost of imported goods, encouraging consumers to purchase U.S.-made products. From an economic perspective, this effectively reduces the purchasing power of the U.S. dollar relative to goods. As gold is priced in dollars, a weaker dollar purchasing power would drive gold prices higher. Additionally, retaliatory measures by trading partners could indirectly devalue other global fiat currencies, further bolstering gold’s value. Beyond tariffs, other factors support our bullish outlook for gold, including the substantial U.S. debt levels (Figure 4.2) and the ongoing accumulation of gold reserves by global central banks (Figure 4.3). In summary, even absent an escalation in the Iran-Israel conflict, fundamental factors are set to propel gold prices upward. However, if the conflict intensifies, it would serve as an additional catalyst for significant gold price gains.

Figure 4.1: Gold Prices (USD/oz)

Source: Refinitiv, TradingKey

Figure 4.2: Total U.S. National Debt (trillion USD)

Source: Refinitiv, TradingKey

Figure 4.3: Global Central Bank Gold Reserves (thousand tonnes)

Source: Refinitiv, TradingKey

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.