In 2026, Should Investors Buy Gold or Hold the Dollar?

Global assets faced localized volatility in 2026 due to geopolitical conflicts. Gold experienced a sharp correction from record highs, pressured by liquidity demand, inflation, and a stronger dollar, despite its safe-haven status. The U.S. Dollar Index showed short-term resilience, supported by economic data and high interest rates, but faces long-term challenges from fiscal deficits and inflation. While the dollar offers liquidity, gold's role in wealth preservation and credit hedging is becoming strategically essential amid U.S. credit erosion and de-dollarization trends. Market consensus views gold's decline as a bull market correction, with institutions maintaining long-term price targets.

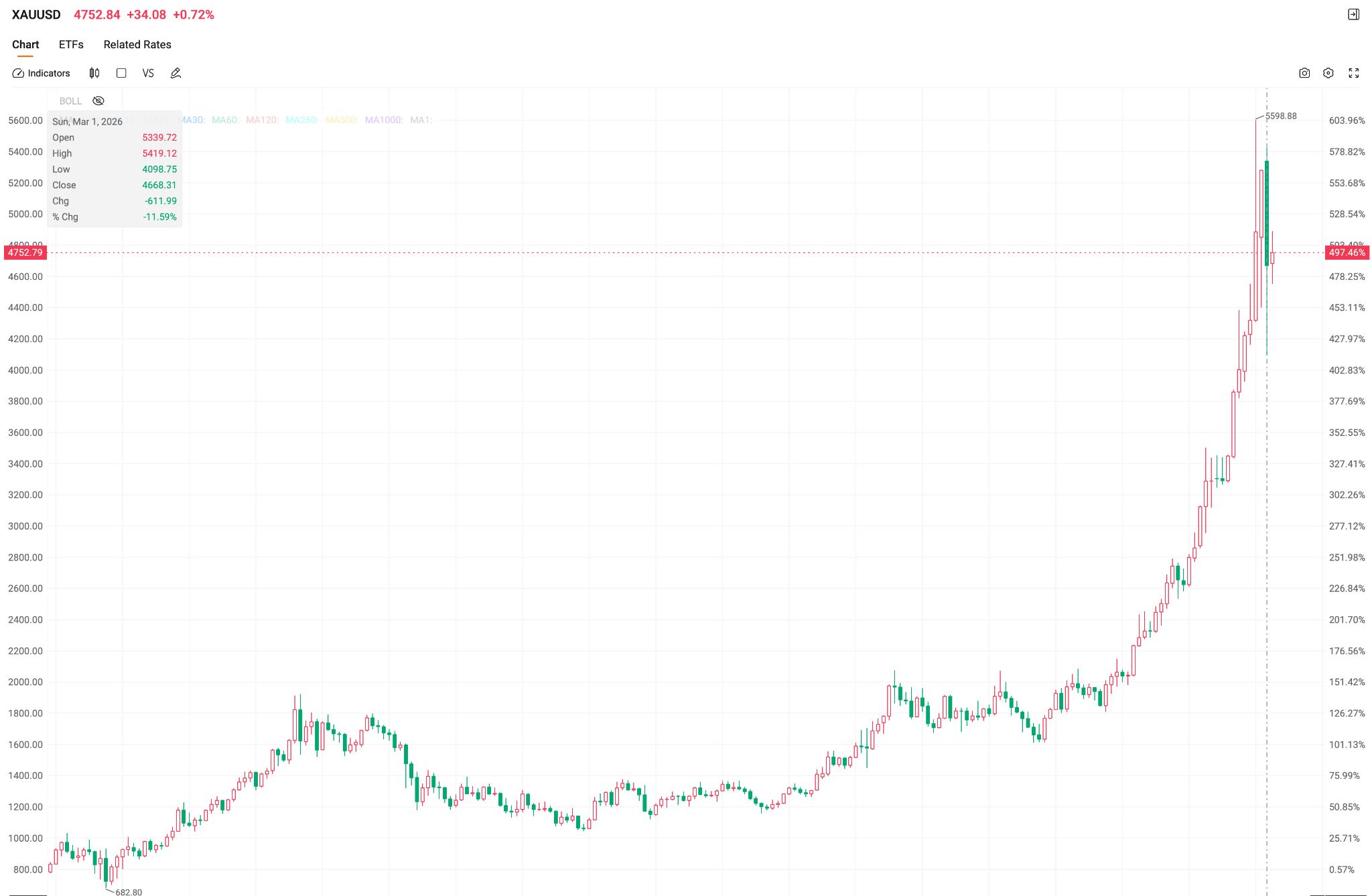

TradingKey - In 2026, global assets exhibited a localized seesaw effect against the backdrop of geopolitical conflicts. Gold, traditionally known as a safe-haven asset, suffered a sharp correction after hitting all-time highs in late January 2026, while oil prices continued to surge amid geopolitical tensions.

Accompanying the liquidity crunch triggered by conflicts in the Middle East, gold not only failed to function as a safe haven but also briefly turned into a risk-like asset. Its safe-haven status was suppressed by factors such as liquidity demand, global inflation expectations, and a strengthening U.S. dollar. In March alone, gold prices plummeted 11.6%, marking its worst monthly performance since June 2013.

Meanwhile, the U.S. Dollar Index rebounded after dipping to the 95 level in late January. Fueled by the outbreak of the U.S.-Iran conflict in February, the index strengthened in March, repeatedly breaking above the 100 mark before retreating on expectations of a de-escalation; overall, it continued the range-bound oscillation seen in 2025.

Currently, global investors are focused on whether to buy gold or hold the U.S. dollar. Fundamentally, this choice between core assets is a market bet and judgment on whether the "U.S. dollar credit system is beginning to fray."

Gold Prices: Short-term Pressure Does Not Alter Long-term Logic

During the Asian session on April 23, spot gold traded near $4,700 per ounce, having pulled back approximately 16% from its record high of $5,595 on January 29.

Gold prices have remained under pressure recently. On one hand, this is attributed to profit-taking following a prolonged rally. Some investors have chosen to lock in profits to extract liquidity. During the U.S.-Iran conflict, driven by persistent safe-haven sentiment, gold—which had previously benefited significantly—was widely used as the primary choice for liquidity extraction, allowing for portfolio rebalancing into other assets that incurred losses due to geopolitical conflict.

On the other hand, the surge in oil prices caused by geopolitical conflicts has led to a rapid resurgence in global inflation, significantly dampening rate cut expectations for most central banks. Using the Federal Reserve as a benchmark, the market had expected two rate cuts in 2026 before the conflict fully escalated. However, following the full outbreak of hostilities and oil prices repeatedly hitting periodic highs, traders completely priced out expectations for a Fed rate cut this year. Markets even briefly placed bets on a rate hike, which led to a stronger U.S. dollar, suppressing the appeal of dollar-denominated gold.

Data released by the U.S. Bureau of Labor Statistics showed that the annual U.S. CPI rate for March 2026 was 3.3%, in line with expectations, while PPI rose by 4%, significantly lower than the expected 4.5%. Although the BLS data suggests that most inflationary indicators were not as extreme as the market feared, the reality of a short-term spike in implicit inflation has been fully priced into market expectations. This implies that the start of the Federal Reserve's rate-cutting cycle remains far off.

[The probability of a Fed rate cut this year is only about 20%; Source: CME Group]

CME data indicates a 100% probability that the Federal Reserve will keep interest rates unchanged in April. Rate cut expectations have been compressed to nearly zero, leaving gold—a non-interest-bearing asset—under continued pressure.

However, Wall Street institutions almost unanimously believe this is merely a "correction within a bull market."

In January 2026, Goldman Sachs raised its year-end gold price target from $4,900 to $5,400 per ounce, citing growing demand from private investors, continuous central bank purchases, and the expectation of two Fed rate cuts within the year. Monthly central bank purchases are expected to remain at 60 tons.

Meanwhile, despite market bets on a slim possibility of a rate cut this year, Goldman Sachs still projected in March that the Federal Reserve would cut rates in September and December of this year.

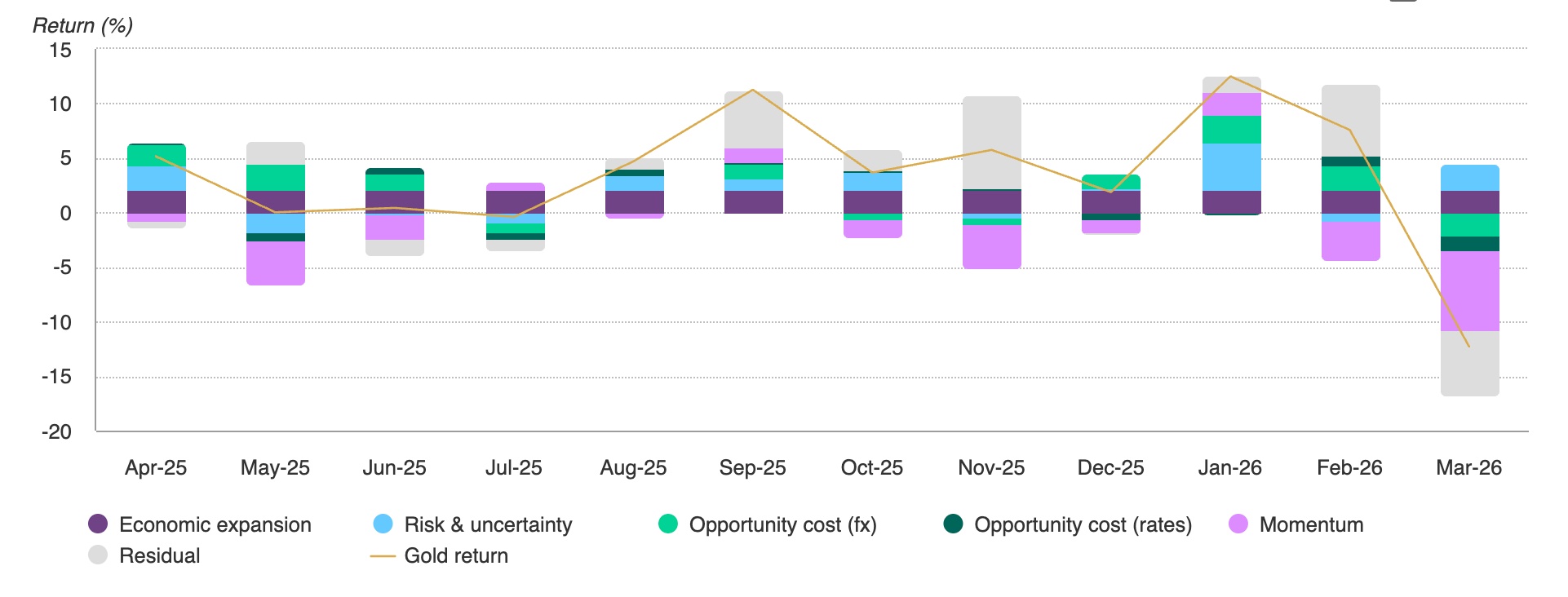

[The decline in March was influenced by momentum factors; Source: Bloomberg, World Gold Council]

The World Gold Council believes that gold's weak performance in March was driven by deleveraging and liquidity dynamics rather than fundamental factors. Rising U.S. real interest rates and a stronger dollar were the primary causes, and the Council maintains that gold's fundamentals remain robust.

Despite having previously lowered its gold price forecast for the second half of the year, Morgan Stanley still predicts that gold will rise to $5,200 in the latter half of 2026. Judging by market confidence, the long-term investment thesis for gold remains widely accepted by the market.

US Dollar: Short-Term Resilience Fails to Mask Credit Erosion

As of April 23 ET, the U.S. Dollar Index stood at 98.6, down approximately 2% from its late-March high but remaining within a volatile yet strong range. Previously, the U.S. released March retail sales figures, which showed stronger-than-expected growth indicating that the U.S. economy remains resilient. Combined with the return of safe-haven demand due to recurring tensions in the Middle East and the Fed's maintenance of high interest rates providing underlying rate support, the dollar maintains its strength in the short term.

However, the long-term structural challenges facing the dollar cannot be ignored. As the U.S. fiscal deficit expands and inflation expectations undergo a structural shift upward, the safe-haven function of U.S. Treasuries has significantly weakened. At this stage, geopolitical risk is evolving from a "tail risk" into a "base case." If the timeline of geopolitical risks continues to stretch, the dollar's safe-haven attributes will gradually erode, meaning that demand for the dollar may exhibit a trend of marginal decline.

Meanwhile, as of the end of 2025, the total value of gold reserves held by non-U.S. central banks globally reached approximately $3.93 trillion to $4.2 trillion, exceeding the total amount of U.S. Treasuries held overseas during the same period. The value of gold in central bank reserves has historically surpassed that of Treasuries, and "de-dollarization" demand exhibits strong price stickiness amid sanctions anxiety.

Against this backdrop, the Federal Reserve's rate-cut path has reached a stalemate. The market estimates the probability of a cumulative 25-basis-point rate cut by June at only 1.7%, meaning the previously anticipated cuts are unlikely to materialize. While high interest rates certainly support the dollar's short-term exchange rate, they also mean that U.S. fiscal debt costs continue to climb, further eroding the foundation of the dollar's credit.

This situation creates a paradox for the dollar's resilience; therefore, in the long run, the dollar will continue to face the structural contradiction of its long-term value being eroded.

Fundamental Differences Exist in the Allocation Logic of Gold and the Us Dollar

From a historical perspective, gold and the US dollar both undoubtedly possess safe-haven attributes, but fundamental differences remain at their core.

The core function of the US dollar is "liquidity and safe-haven," with its short-term strength supported by current interest rates providing certainty for cash holders. However, in a stagflationary environment triggered by energy supply shocks, the hedging logic of traditional broad asset classes frequently fails, and the dollar's safe-haven function cannot cover all risk scenarios.

While gold serves a safe-haven function, its essence remains rooted in the core functions of "value preservation and credit hedging." As the US fiscal deficit nears $40 trillion and dollar credit is eroded, gold's intrinsic attribute of not depending on any sovereign credit gives it irreplaceable allocation value.

Core asset selection for 2026 cannot be simplified into a binary choice of "buying gold versus holding US dollars"; rather, they must be evaluated separately from an asset allocation perspective. The certainty brought by the short-term interest rate advantage of the US dollar remains suitable as part of a liquidity allocation.

Amid the structural wave of "de-dollarization," the long-term value of gold as a credit hedging tool for major global nations is upgrading from a trading option to a strategic allocation necessity.

Driven by the resonance of normalized geopolitics and the erosion of US sovereign credit, it is not far-fetched for gold to surpass $5,000 once again in 2026.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.