DELL: AI on a tear, legacy biz heats up; firing on all cylinders!

DELL released its FY2027 Q1 (quarter ended Apr 2026) results after hours on May 29 Beijing time.

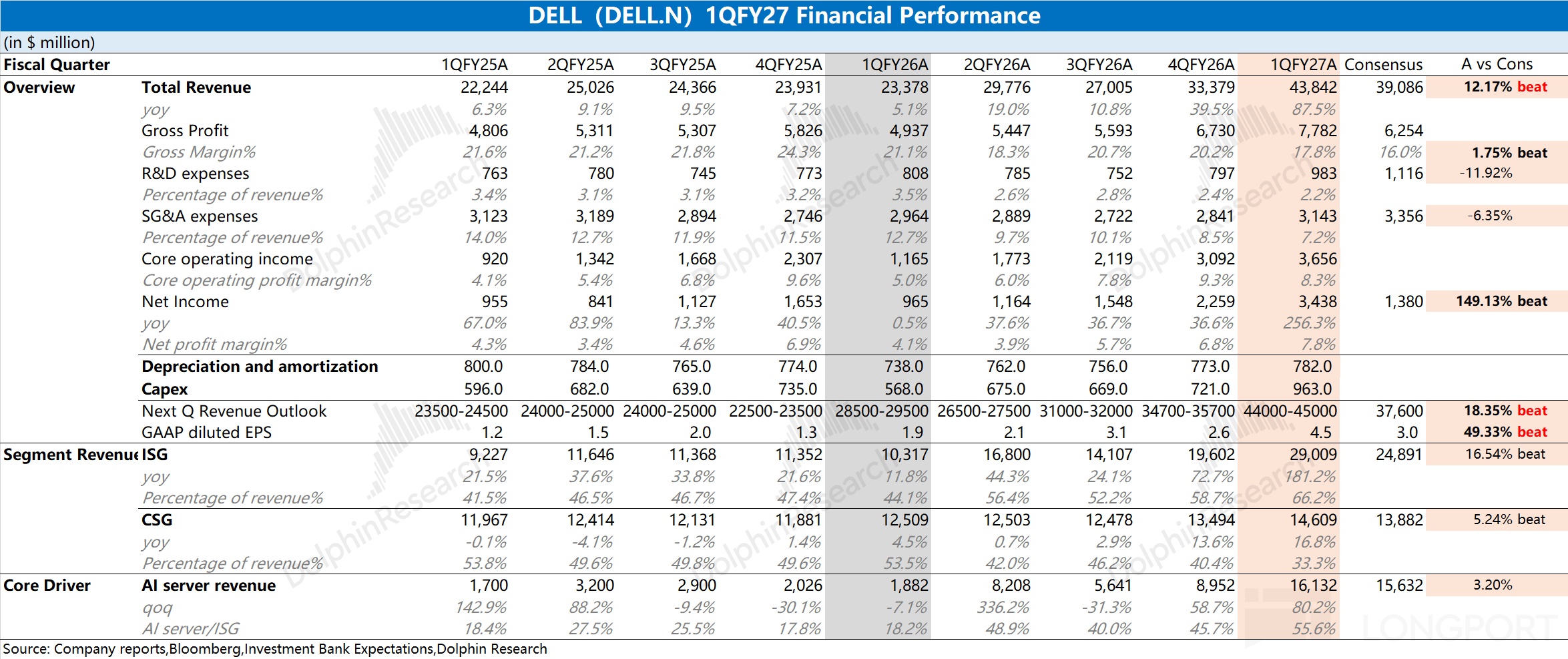

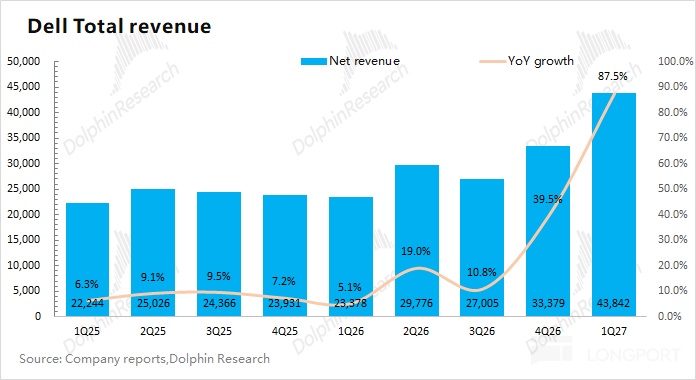

1. Core results: $Dell Tech(DELL.US) revenue was $43.8bn (+87% YoY), well above consensus ($39.0bn). QoQ revenue rose by $10.5bn, driven mainly by AI server shipments.

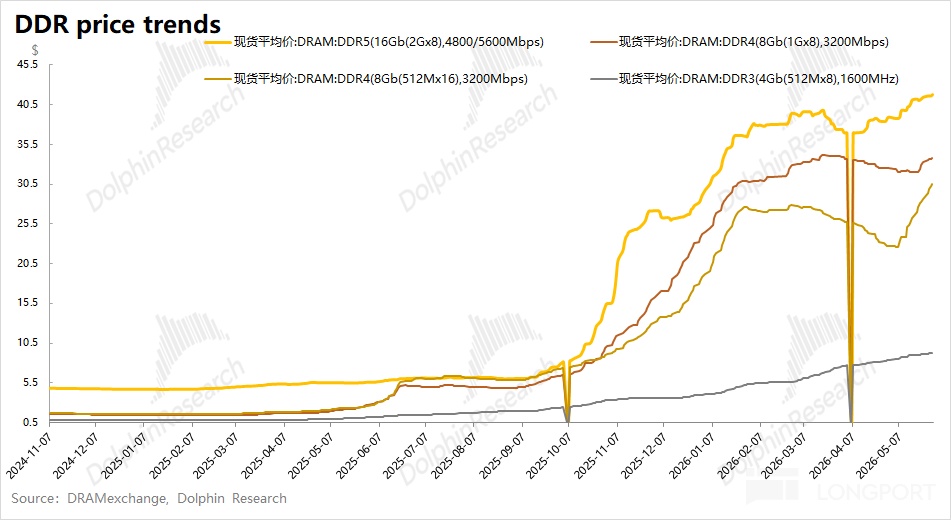

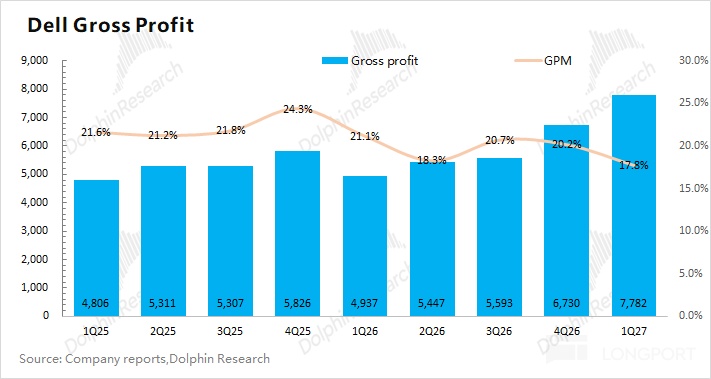

Gross margin was 17.8%, down 240bps QoQ but ahead of consensus (16%). The margin contraction reflected higher storage costs and mix shift toward lower-margin hardware.

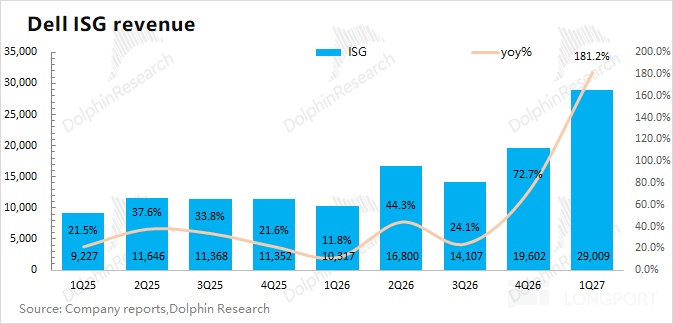

2. ISG (Infrastructure Solutions): Q1 revenue was $29.0bn, up $9.4bn QoQ and far above consensus ($24.9bn). The QoQ step-up came from AI server growth and a rebound in traditional servers.

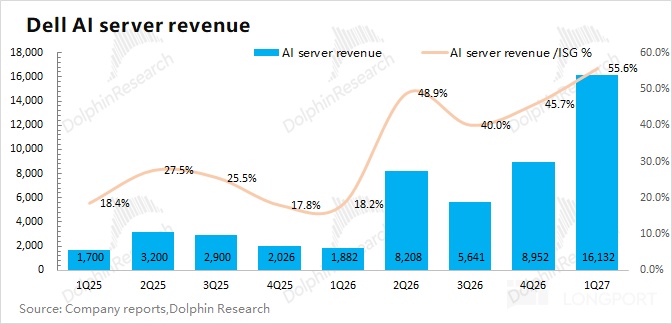

① AI servers: AI server revenue was about $16.1bn, topping raised buy-side expectations ($15.6bn).

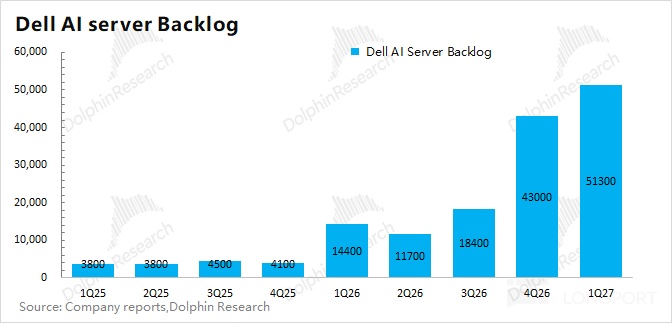

New AI orders reached $24.4bn in the quarter, taking AI backlog to $51.3bn by quarter-end. Dolphin Research estimates next-quarter AI server revenue at $15.5bn+ amid clear supply constraints.

② Other: Beyond AI servers, legacy areas also rebounded. Traditional server-related revenue was roughly $8.5bn (+92% YoY), well above consensus ($5.0bn) and the key source of the beat. Storage contributed about $4.3bn (+8% YoY) .

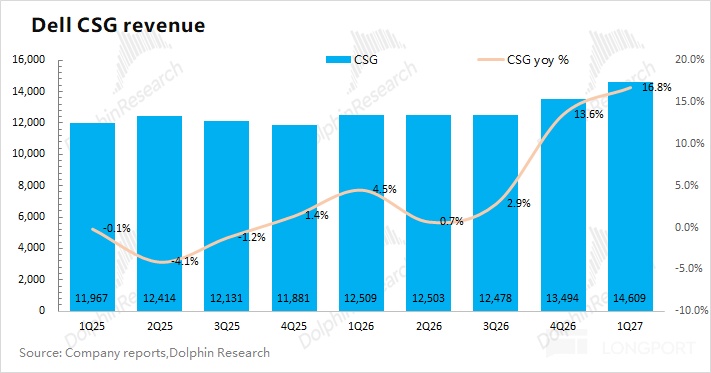

3. CSG (Client Solutions): Q1 revenue was $14.6bn (+17% YoY), above consensus ($13.9bn). By customer type: commercial revenue was $13.0bn (+18% YoY); consumer was $1.6bn (+9% YoY).

4. Next-quarter guidance: DELL guides FY2027 Q2 revenue of $44–45bn, above consensus ($37.6bn). GAAP EPS is guided at $4.5, beating consensus ($3).

Dolphin view: Broad beat as AI and traditional servers both take off

DELL delivered an all-round beat, with revenue up $10.5bn QoQ and growth accelerating. The quarter was propelled by ISG (servers) shipments.

AI revenue reached $16.1bn, up $7.2bn QoQ and above raised expectations ($15.6bn). New AI orders were $24.4bn (vs. $10–15bn expected), pushing AI backlog to $51.3bn by quarter-end and underpinning high growth ahead.

Heading into earnings, the Street had already raised AI server expectations. The biggest surprise came from traditional servers: Q1 traditional server revenue hit $8.5bn (+92% YoY), smashing consensus ($5.0bn) and driving the beat. Consensus had assumed only a steady uptick, but demand is clearly inflecting.

Recent share gains have been fueled by rising AI server expectations. DELL is transitioning from GB200 to GB300, which should lift ASPs. It benefits from both volume and price tailwinds, plus a legacy server recovery; AI momentum, in particular, helped the multiple break above the traditional range ceiling.

Management raised full-year guidance: FY revenue to $165–169bn, up by $17bn (prior $138–142bn). Q1 itself was about $10bn above the prior quarterly run-rate, and Dolphin Research sees the full-year guide as conservative with room for further raises.

Outside the print, investors focused on the following:

a) Ongoing tightness in storage: The biggest downstream impact is on PCs, where the cost-to-price-to-demand transmission cooled end-market growth to 4% in Q1.

Meanwhile, rising storage prices pressured hardware margins across PCs and servers. GPM fell to 17.8%, reflecting cost inflation, yet still beat the 16% Street view, underscoring solid cost control.

b) AI servers: the key swing factor as legacy faces pressure.

Hyperscalers have lifted capex outlooks, and Dolphin Research estimates the four core cloud players (Alphabet, Meta, Microsoft, and Amazon) could spend $700bn+ in 2026, up ~80% YoY.

With capex accelerating, DELL had struggled to break $10bn in quarterly AI servers, capping AI re-rating potential. This quarter’s $16.1bn, up $7.2bn QoQ, showcased tangible high growth, reflecting robust AI server demand and higher ASPs from the GB200→GB300 transition.

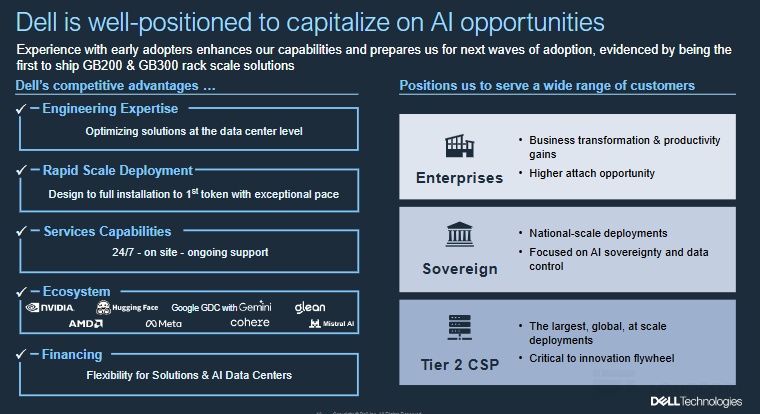

DELL has deep ties with NVIDIA, offering Blackwell and Vera Rubin options and collaborating on the next-gen Feynman platform. Especially in Tier-2 CSPs (Neocloud) and public sector/enterprise, these customers typically avoid direct ODM sourcing given integration needs; they prefer OEMs with full solutions.

DELL provides full-stack, end-to-end services, spanning desktop AI workstations (GB10/GB300 DGX), rack servers, storage, networking, software orchestration (OpenManage), and services (installation, tuning, 24/7 support). This end-to-end model positions DELL to win more in Tier-2 CSP and public sector markets.

DELL’s market cap is $204.7bn, implying ~16x FY2027 post-tax core OP on assumptions of 60% revenue growth, 17% GPM, and a 17% tax rate. Historically, the multiple has ranged 8–20x PE, and after the sharp estimate revisions, today’s PE sits just above the mid-range.

After the recent rally, the market has priced in faster AI growth. Leading sell-side shops now model $65bn of AI revenue (+163% YoY), implying investors expect a guide-up post-print.

Management raised full-year AI guidance to $60bn (from $50bn), which Dolphin Research still views as conservative: ① 1H AI revenue should reach $31.6bn, and with Rubin upgrades in 2H, revenue should not be lower; ② backlog already exceeds $50bn, and grew even as AI revenue surged, signaling persistent undersupply.

Overall, AI is accelerating, traditional servers are clearly rebounding, and PCs/margins beat expectations. Operations are improving across the board, and there is scope to raise the full-year outlook again. With AI tailwinds and high growth, DELL deserves to trade beyond traditional frameworks, and its multiple could keep breaking past historical ceilings.

Details on DELL (DELL.N) below:

I. DELL overall results

1.1 Revenue

In FY2027 Q1 (26Q1), DELL delivered revenue of $43.8bn (+87% YoY), beating consensus ($39.0bn) . QoQ revenue rose $10.5bn, led by ISG growth; within that, AI revenue rose $7.2bn QoQ and traditional servers rose $2.7bn QoQ.

1.2 Gross profit

Gross profit was $7.8bn (+35.6% YoY) in FY2027 Q1 (26Q1).

GPM was 17.8%, down 240bps QoQ but above consensus (16%) .

The decline reflected: ① higher storage costs; ② mix shift toward lower-margin ISG, which diluted blended GPM.

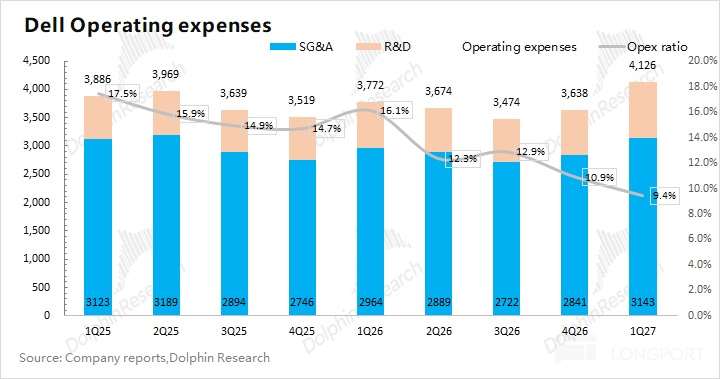

1.3 Opex

Operating expenses were $4.1bn in FY2027 Q1 (26Q1), up 9% YoY. Scale benefits drove the opex ratio down to 9.4% this quarter.

Breakdown: 1) R&D was $980mn, up 22% YoY, with increased investment momentum. 2) SG&A was $3.1bn, up 6% YoY.

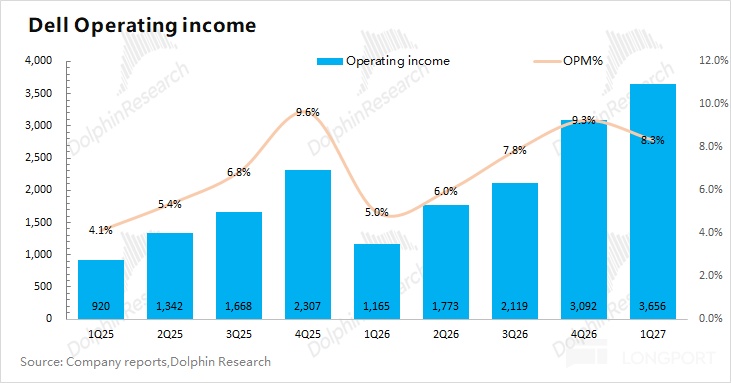

1.4 Net profit

Core operating profit was $3.66bn in FY2027 Q1 (26Q1), up 214% YoY, with a core OPM of 8.3%. Growth on the bottom line was driven by the sharp revenue increase.

II. Core segments: AI accelerates, traditional rebounds

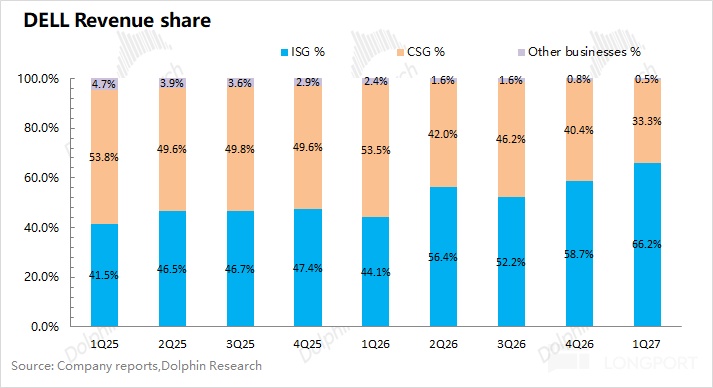

By segment, ISG expanded on AI server strength, reaching 66% of revenue this quarter.

Based on management’s growth framework, FY2026–FY2030 CAGR for ISG (11–14%) will outpace CSG (2–3%), lifting ISG’s mix further.

ISG is the most important part of the company. By sub-segment:

2.1 ISG (Infrastructure Solutions)

ISG revenue was $29.0bn in FY2027 Q1 (26Q1), up 181% YoY, far above consensus ($24.9bn) .

Detail: ① AI servers were about $16.1bn, up $7.2bn QoQ, and the main ISG driver. ② Traditional servers and related were $8.5bn (+92% YoY). ② Storage was $4.3bn (+8% YoY).

ISG growth was powered by both AI and traditional servers. Traditional servers began a sharp rebound, while AI’s high growth now accounts for over half of ISG.

Beyond reported AI revenue, management disclosed leading indicators in new AI orders and backlog. New AI orders were $24.4bn (ahead of the $10–15bn range), and AI backlog reached $51.3bn, setting up sustained FY2027 growth.

On supply, DELL has deep collaboration with NVIDIA, offering Blackwell, Vera Rubin, and working on the next Feynman platform. As GB200→GB300→Rubin upgrades roll through, AI server ASPs should keep rising.

On the customer side, Tier-2 CSPs (Neocloud) and public sector/enterprise typically do not buy directly from ODMs due to integration complexity; they need OEMs that offer full-stack solutions. DELL’s end-to-end capabilities make it a preferred choice and should drive order wins in these markets.

Although management raised full-year AI revenue guidance to $60bn (from $50bn), Dolphin Research still sees it as conservative. 1H can deliver $31.6bn, and with Rubin upgrades, 2H should not be lower. With $50bn+ in AI backlog, further guide-ups are likely.

2.2 CSG (Client Solutions)

CSG revenue was $14.6bn in FY2027 Q1 (26Q1), up 17% YoY, beating consensus ($13.9bn) .

By mix: commercial remained the core at $13.0bn (+18% YoY), while consumer revenue was $1.6bn (+9% YoY).

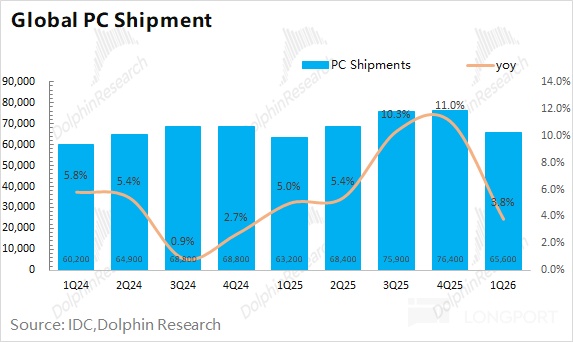

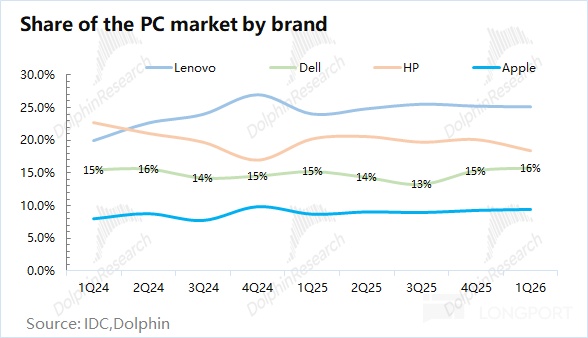

Global PC shipments were 65.6mn units in Q1 2026 (+4% YoY), with growth decelerating. DELL shipped 10.3mn units (+7% YoY), outpacing the market and lifting share to 15.7%.

While PC demand remains soft overall, DELL’s commercial-heavy mix reduces exposure to the consumer cycle. Commercial PCs still grew 18% this quarter.

Amid ongoing storage price increases, DELL raised PC pricing earlier this year, passing through part of the cost. Shipments still grew YoY, indicating strong brand and execution.

Net-net, storage tightness will continue to weigh on PCs, but given mix and execution, CSG should remain on a steady upward track.

Related DELL (DELL.N) coverage by Dolphin Research:

Earnings calls and reviews

Feb 27, 2026 Trans: Dell (Trans): AI orders exclude Rubin; legacy also stays positive

Feb 27, 2026 First Take: DELL: Can doubling AI offset storage tightness?

Nov 26, 2025 Trans: Dell (Trans): Value lies in L11+ end-to-end solutions

Nov 26, 2025 First Take: DELL: Storage hikes add friction? AI guide supports

Aug 29, 2025 Trans: Dell (Trans): AI server shipments balanced across halves

Aug 29, 2025 First Take: Dell: Are the ‘crazy’ AI orders just a flash in the pan?

Deep dives:

Jul 11, 2025 Deep Dive: AI double buffs: A new spring for Dell?

Jul 9, 2025 Deep Dive: Dell: Riding the AI wave with a comeback

Risk disclosure and disclaimer: Dolphin Research disclaimer and general disclosures

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.