3 Reasons I'm Buying Amazon Stock Hand Over Fist Right Now

Key Points

In Amazon's most recent quarter, AWS had its best revenue growth in the past 13 quarters.

Amazon's advertising business is a high-margin, high-growth segment.

Automation has allowed Amazon's e-commerce business to run more profitably.

For a while, Amazon (NASDAQ: AMZN) was the poster child for growth stocks. Unfortunately, that hasn't been the case over the past five years, with its stock only up 38%, underperforming the S&P 500's nearly 67% gains in that time.

Will AI create the world's first trillionaire? Our team just released a report on the one little-known company, called an "Indispensable Monopoly" providing the critical technology Nvidia and Intel both need. Continue »

This year hasn't gotten off to a great start, either. As of the market open on March 26, Amazon's stock is down about 6.5% year to date. One silver lining, though, is that it has been the theme for almost every mega tech company this year. If you look past Amazon's stock price struggles, its business remains rock-solid, and there are three reasons why I'd double down on the stock.

Image source: The Motley Fool.

1. AWS is poised for a growth turnaround story

Let's start with Amazon's most important profit machine: Amazon Web Services (AWS). It's the world's leading cloud platform, with a 28% market share as of the end of last year. It has lost some ground to Microsoft's Azure and Google Cloud, but it remains one of the most crucial foundations in the tech world because so many apps and websites rely on it.

In 2025, AWS accounted for 18% of Amazon's revenue but 57% of its operating income (profit from its daily businesses). A lot was made of AWS's relatively slow revenue growth in recent quarters, but its most recent quarter was a nice turnaround, increasing revenue 24% year over year. That was AWS's fastest-growing quarter in the past 13 quarters.

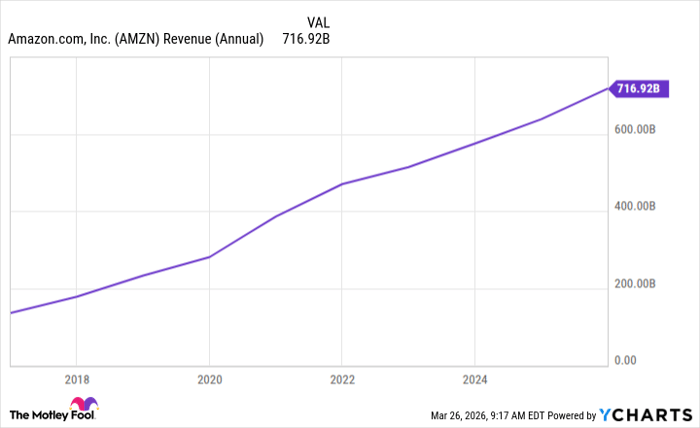

AMZN Revenue (Annual) data by YCharts

AWS's good quarter should hopefully be a sign of what's to come as the AI boom continues, and companies need more cloud and computing capacity. The platform has a $244 billion backlog (companies that have signed contracts but haven't yet received services), indicating it has more demand than it can physically handle right now.

Some investors may not be happy with Amazon's $200 billion spending plan for 2026, but I'm sure they'll be happy with the long-term benefits. Not every dollar will go to AWS, but much of it will go to data centers and AI hardware that will inevitably benefit AWS.

2. Advertising is becoming a legitimate business

Amazon's advertising business doesn't get the attention its e-commerce and cloud businesses do, but it's quietly becoming one of Amazon's brightest areas. In its most recent quarter, advertising revenue increased by 23% year over year to over $21.3 billion.

Amazon has two of the advertising world's most essential things: data and eyeballs. It has billions of online purchases, insight into what people are looking to buy, and many people who use services like Prime Video, Twitch, Fire TV, and Alexa.

That's tons of data it can use to help advertisers run better-targeted campaigns. Add in the platforms it has that allow advertisers to reach millions, and it's the best of both worlds.

Advertising is also a high-margin business because it doesn't take much additional cost to bring on more customers. Much of the infrastructure is in place; Amazon is simply selling digital space, and it's becoming one of its most impressive businesses. It was Amazon's fastest-growing segment until AWS's growth in this past quarter.

3. E-commerce is becoming more efficient

For most of Amazon's existence, the role of its e-commerce business was to generate as much revenue as possible, even if it meant operating at a loss. It sounds backwards, but it allowed them to prioritize growth and getting customer loyalty. It wasn't until around 2017 that its e-commerce business became consistently profitable.

Now, e-commerce is becoming more efficient as it makes a huge push for automation. This has unfortunately led to quite a few layoffs (along with overhiring during the pandemic), but it makes long-term sense for Amazon.

Last July, Amazon announced that it had deployed its 1 millionth robot, with most operating in its 300 global facilities. Using robots allows Amazon to operate more profitably by processing orders faster and reducing handling costs. E-commerce isn't going anywhere, so this investment is well worth making.

Don’t miss this second chance at a potentially lucrative opportunity

Ever feel like you missed the boat in buying the most successful stocks? Then you’ll want to hear this.

On rare occasions, our expert team of analysts issues a “Double Down” stock recommendation for companies that they think are about to pop. If you’re worried you’ve already missed your chance to invest, now is the best time to buy before it’s too late. And the numbers speak for themselves:

- Nvidia: if you invested $1,000 when we doubled down in 2009, you’d have $434,524!*

- Apple: if you invested $1,000 when we doubled down in 2008, you’d have $47,376!*

- Netflix: if you invested $1,000 when we doubled down in 2004, you’d have $503,861!*

Right now, we’re issuing “Double Down” alerts for three incredible companies, available when you join Stock Advisor, and there may not be another chance like this anytime soon.

*Stock Advisor returns as of March 30, 2026.

Stefon Walters has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon. The Motley Fool has a disclosure policy.