POP MART: Pit stop to refuel, tire swap, back in the race! ---

On the afternoon of Mar 25 (Beijing time), Pop Mart (9992.HK) released its H2 2025 results, and the stock tumbled 22% intraday. On a headline basis, H2 performance was broadly in line with Bloomberg consensus, though below some earlier bullish buy-side models. Stripping out the print itself, investors were also disappointed by a cautious 2026 outlook from management, and the two factors combined to drive the afternoon selloff.$POP MART(09992.HK)

Key takeaways are as follows. Please see details below.

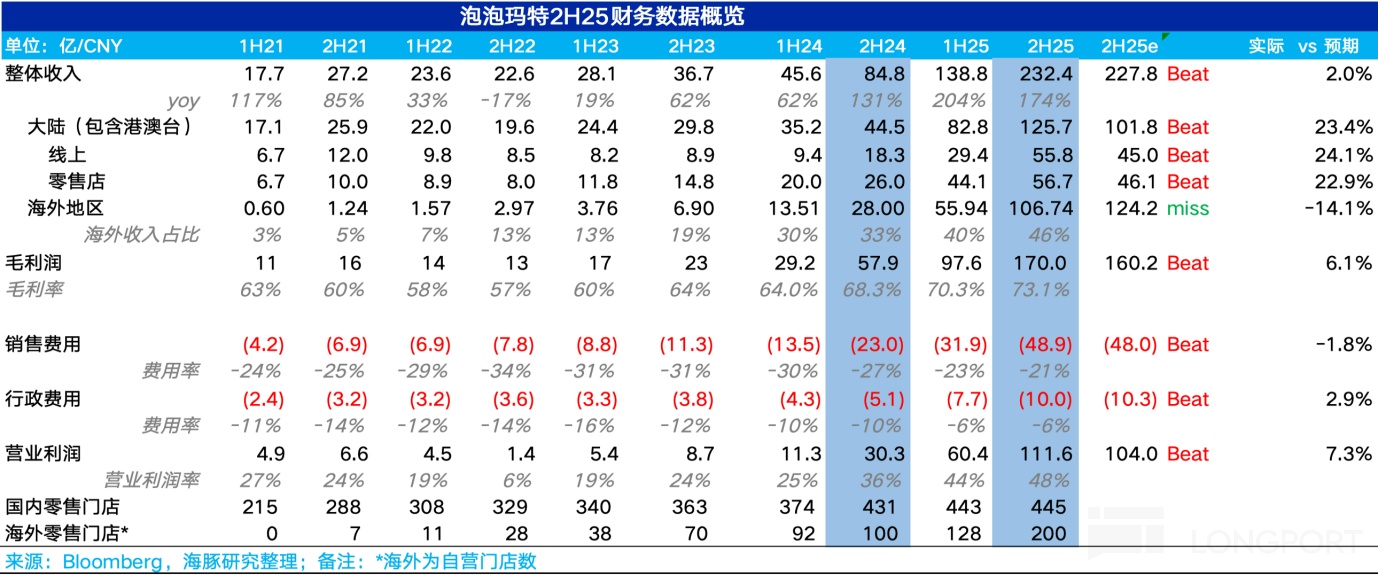

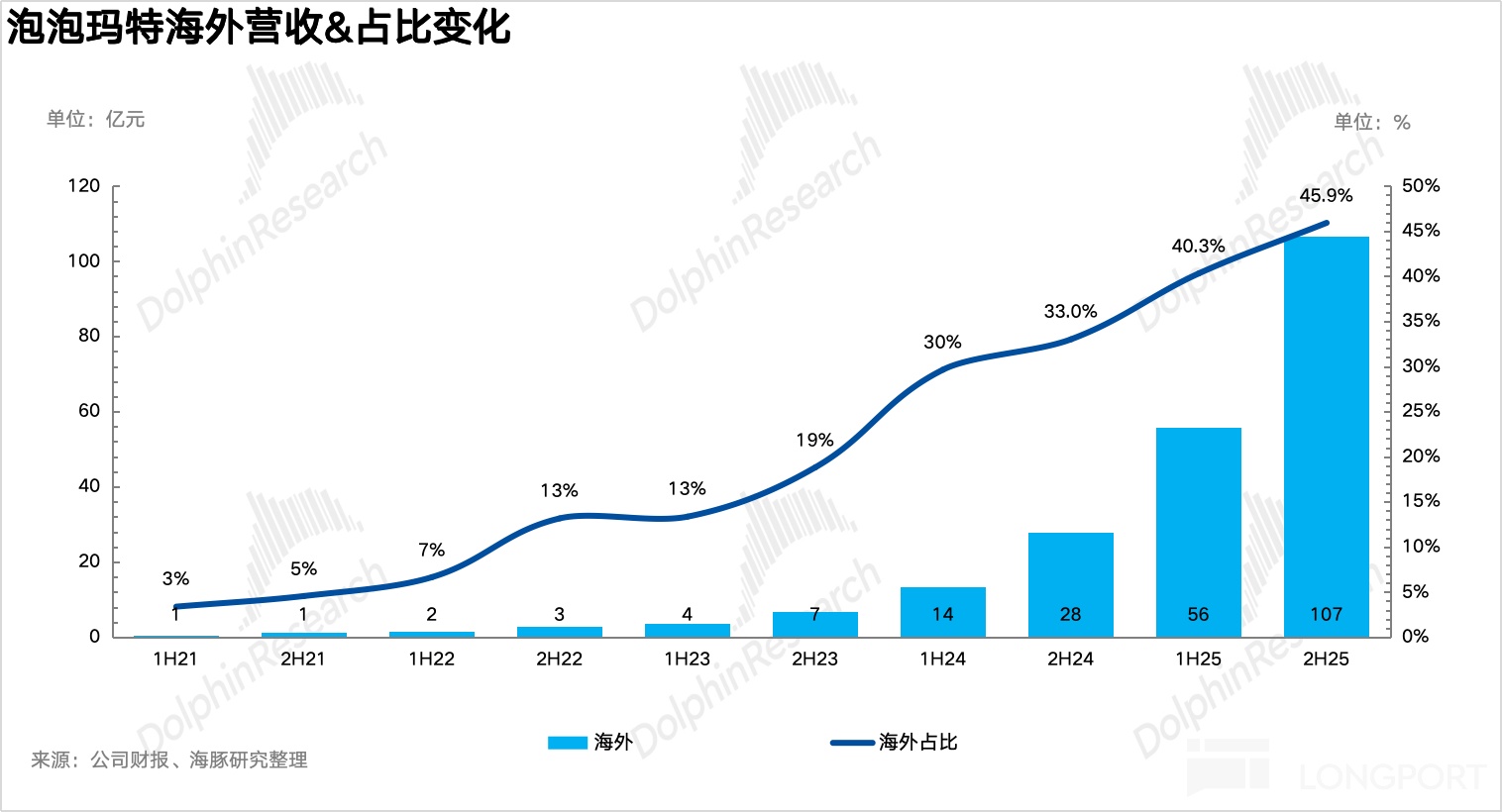

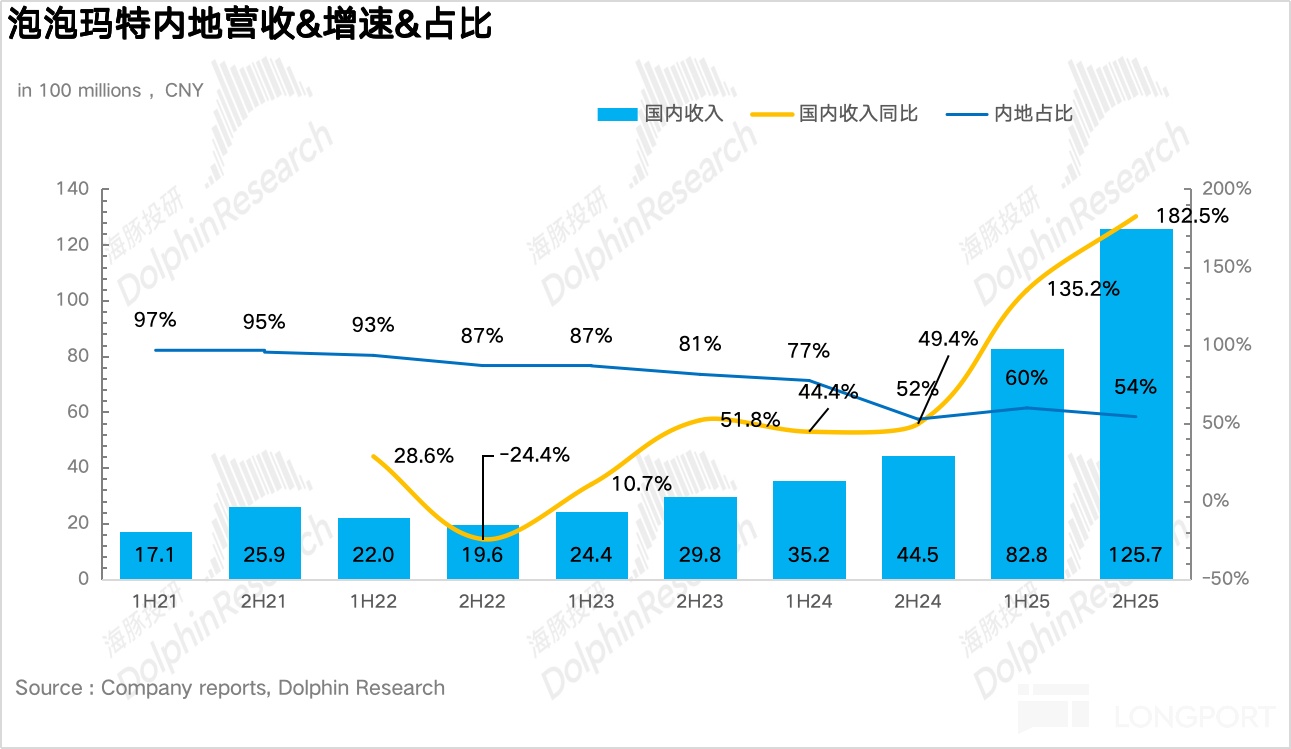

1) Overseas revenue missed. In 2H25, Pop Mart reported revenue of RMB 23.2bn (+174% YoY), with growth moderating from the 200%+ pace in 1H. By segment, domestic revenue came in at RMB 12.6bn (+183% YoY), driven by tighter omni-channel ops with a strong online contribution, accelerating QoQ and beating the Street. Overseas grew 281% YoY but decelerated vs. 1H, especially in North America; vs. the 10x+ surge in Q3, lack of refined local ops led to a visible slowdown in offline sales after Nov, and Black Friday did not deliver the expected spike, taking growth below 500% and weighing on overall overseas momentum.

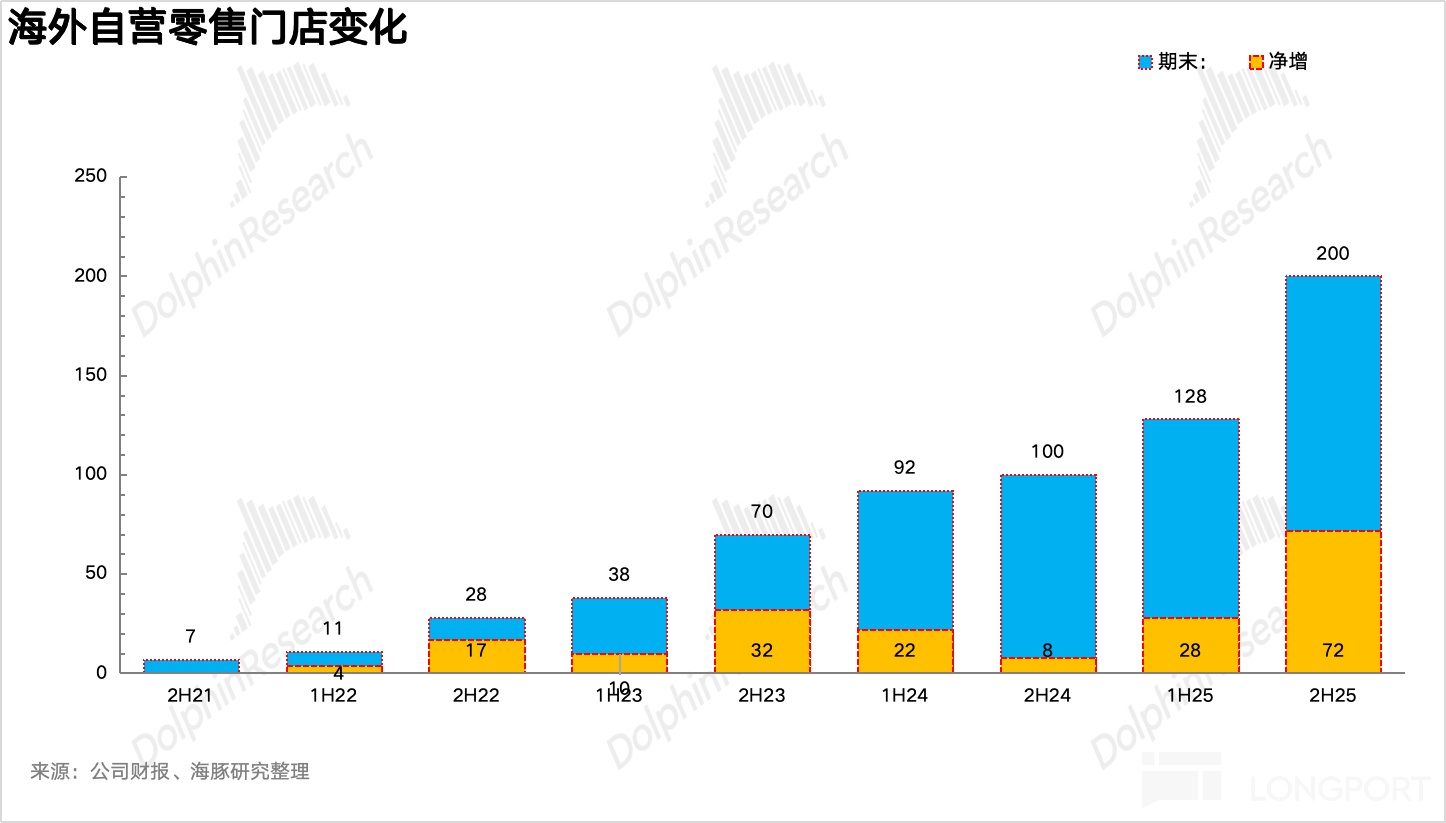

2) Faster overseas store openings. To capture LABUBU-driven traffic, the company accelerated overseas expansion in 2H, adding a net 72 stores, mostly in North America, and deploying a cluster strategy across core districts in New York and Los Angeles.

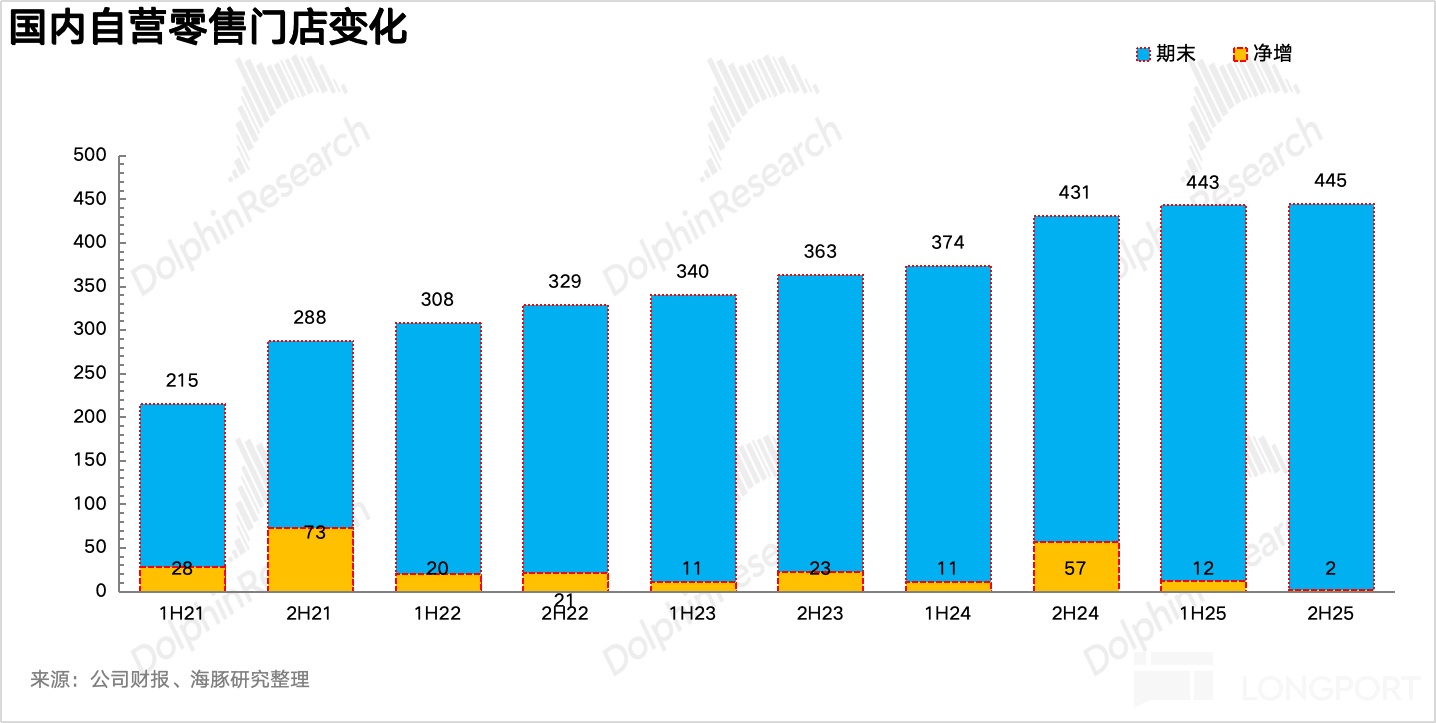

Domestically, only two net new stores were added, with focus on upgrades for existing locations; after expanding floor space by 30%–50%, sales per sqm roughly doubled.

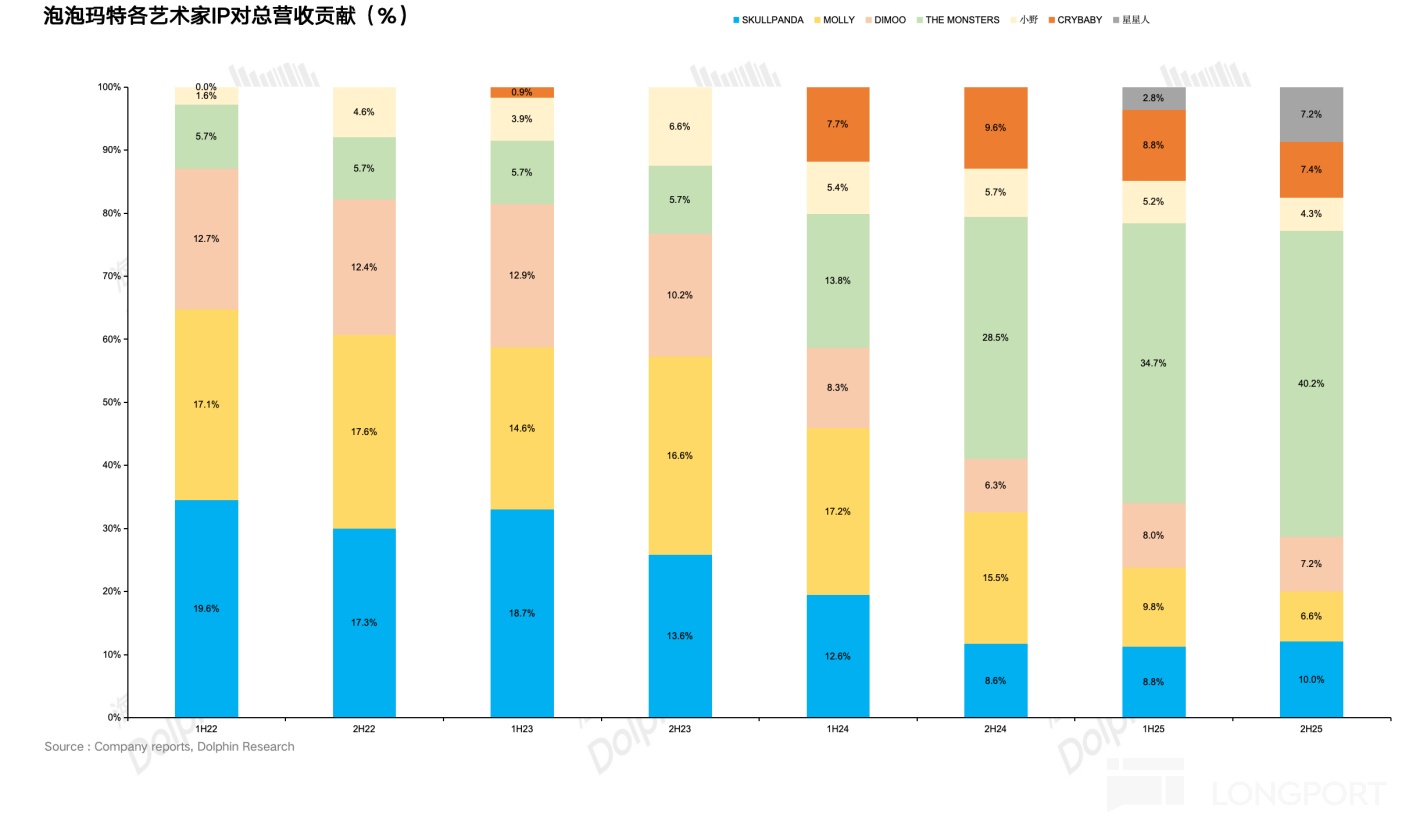

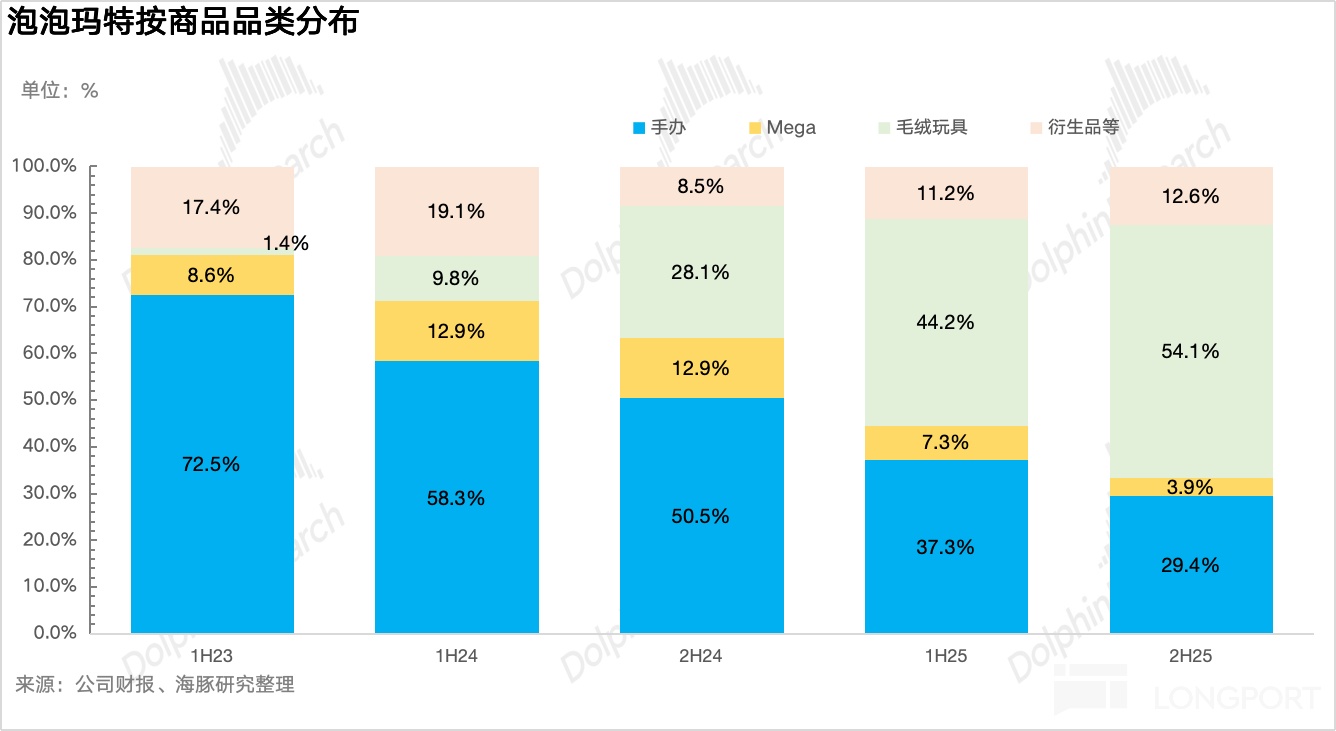

3) Higher mix from The Monsters. As LABUBU capacity ramped in 2H, The Monsters mix rose from 34.7% in 1H to 40%. Other legacy core IPs, including Molly and Dimoo, were softer with share declines. The bright spot was the Xing Xing Ren series, now the fastest-growing IP, with mix up from below 3% in 1H to 7.2%.

4) Plush now contributes roughly half. By category, blind-box figurines kept losing share, while higher-margin plush surged. Beyond LABUBU, other flagship IPs are also shifting into plush, with the overall plush mix up from 44% in 1H to 54%. In addition, POP BLOCK (blocks) doubled vs. 1H on the back of Molly Architecture and LABUBU Forest launches, showing solid momentum.

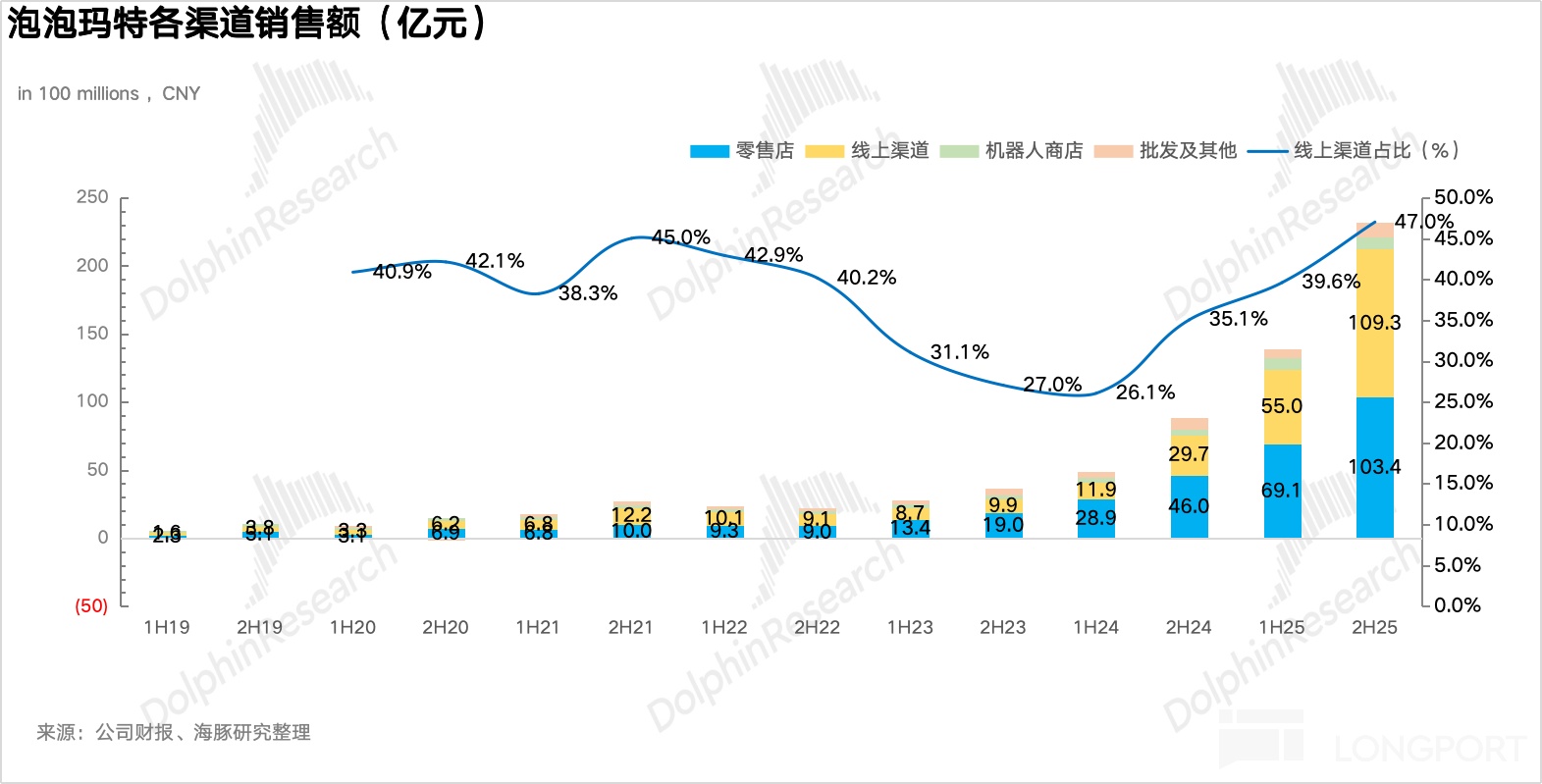

5) Online outperformed. By channel, Pop Mart ramped livestreams on platforms such as Douyin in 2H, materially lifting online conversion. It also added more gamified features in the official WeChat mini-program (e.g., team draws, disclosed odds for rare pieces), which concentrated and activated private traffic, driving online revenue up over 200% YoY and ahead of the overall market.

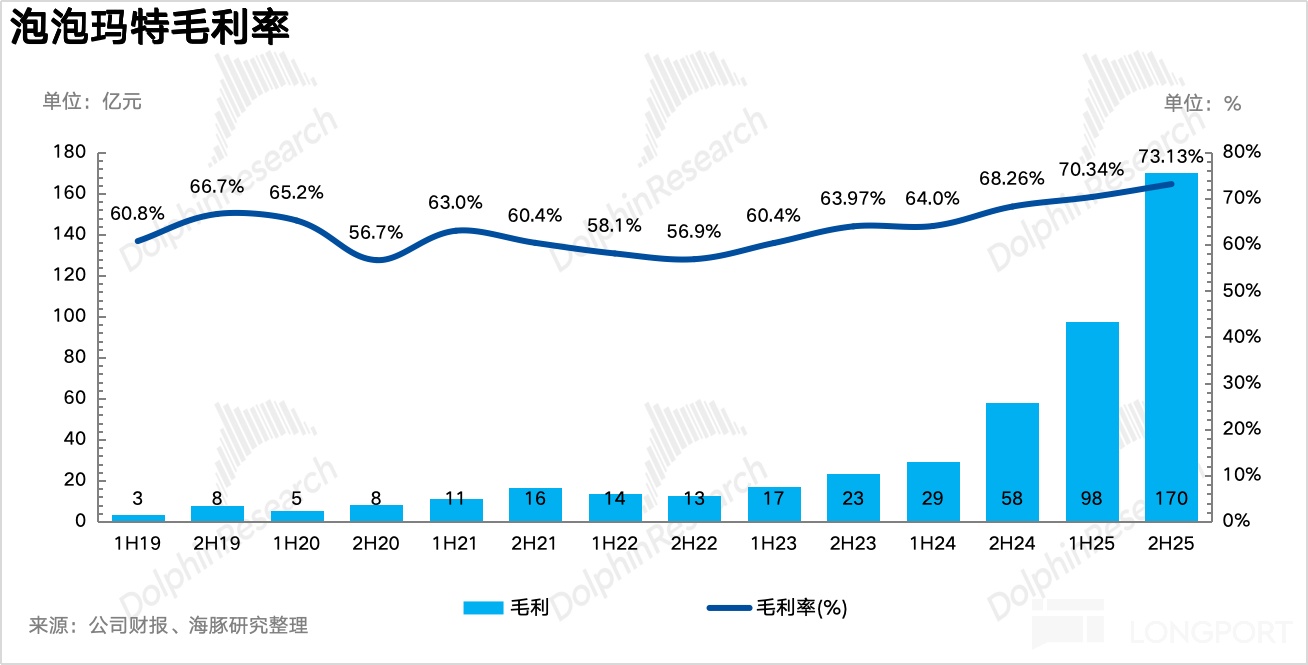

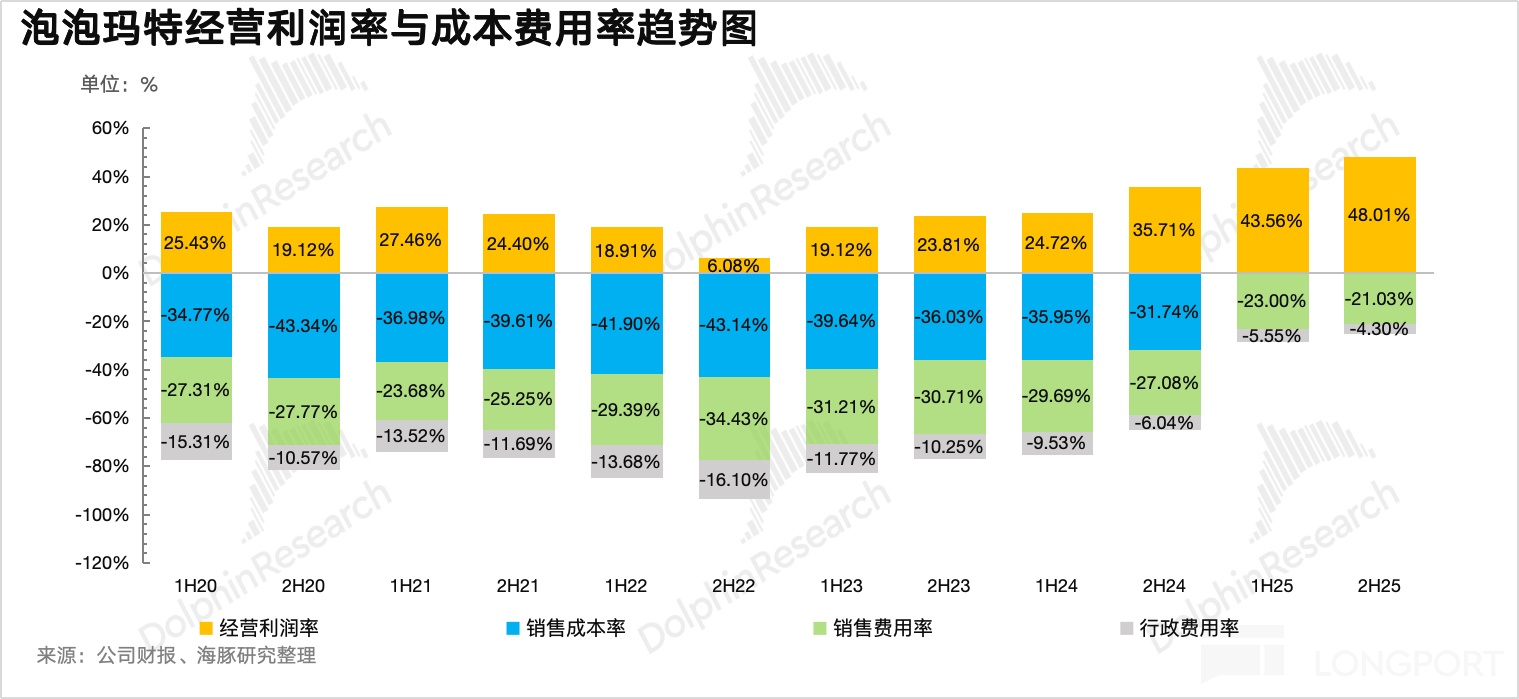

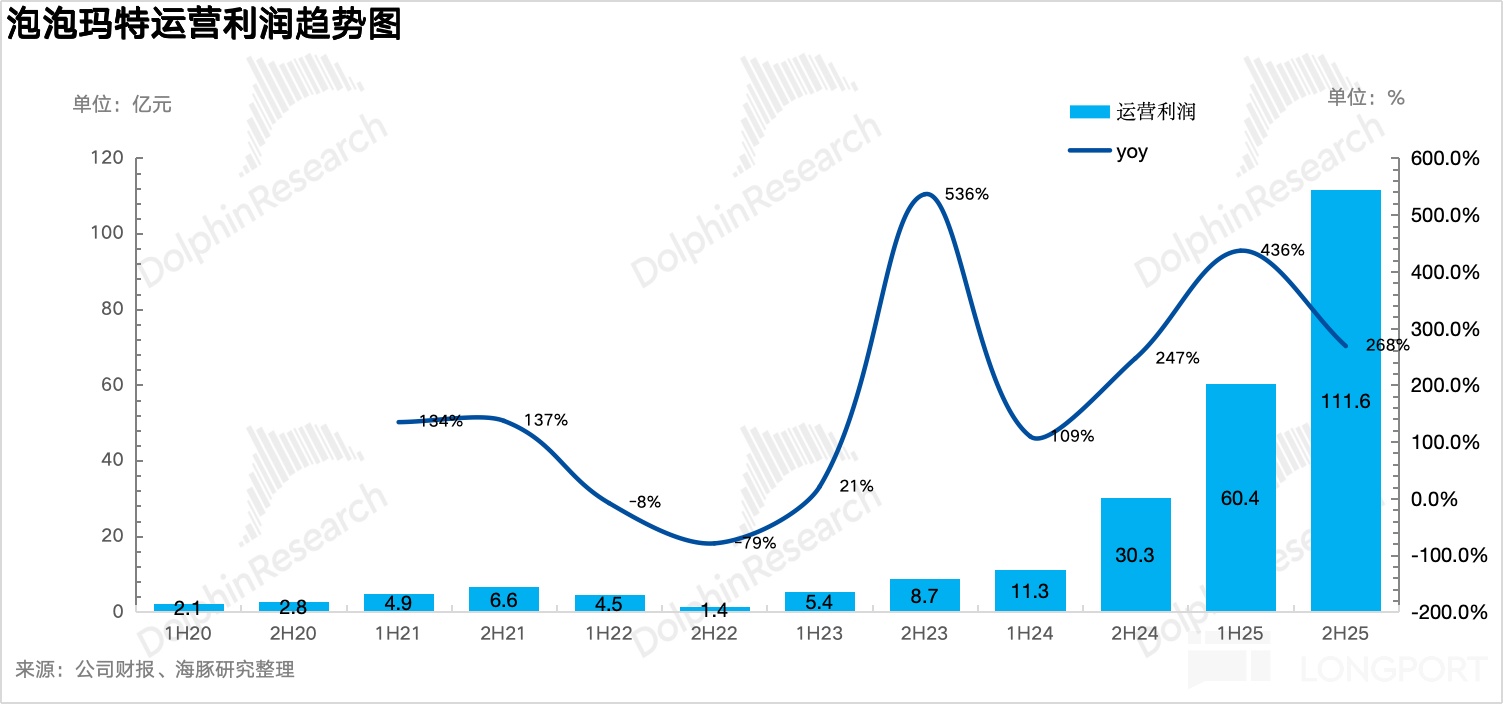

6) Operating leverage kept expanding. With a richer mix of higher-margin overseas sales and a surge in plush, gross margin reached 73% in 2H, a record high. On opex, a higher online mix boosted acquisition efficiency, taking the sales expense ratio down 600bps to 21%, while G&A was disciplined, down 400bps to 6%, lifting core OPM to 48%, also a record.

7) Guidance. On the call, management guided 2026 revenue growth of at least 20%. Ex-store expansion, this implies low-single-digit same-store growth; in their words, it will be a year of 'pit stop' maintenance.

8) Detailed financials:

Dolphin Research view:

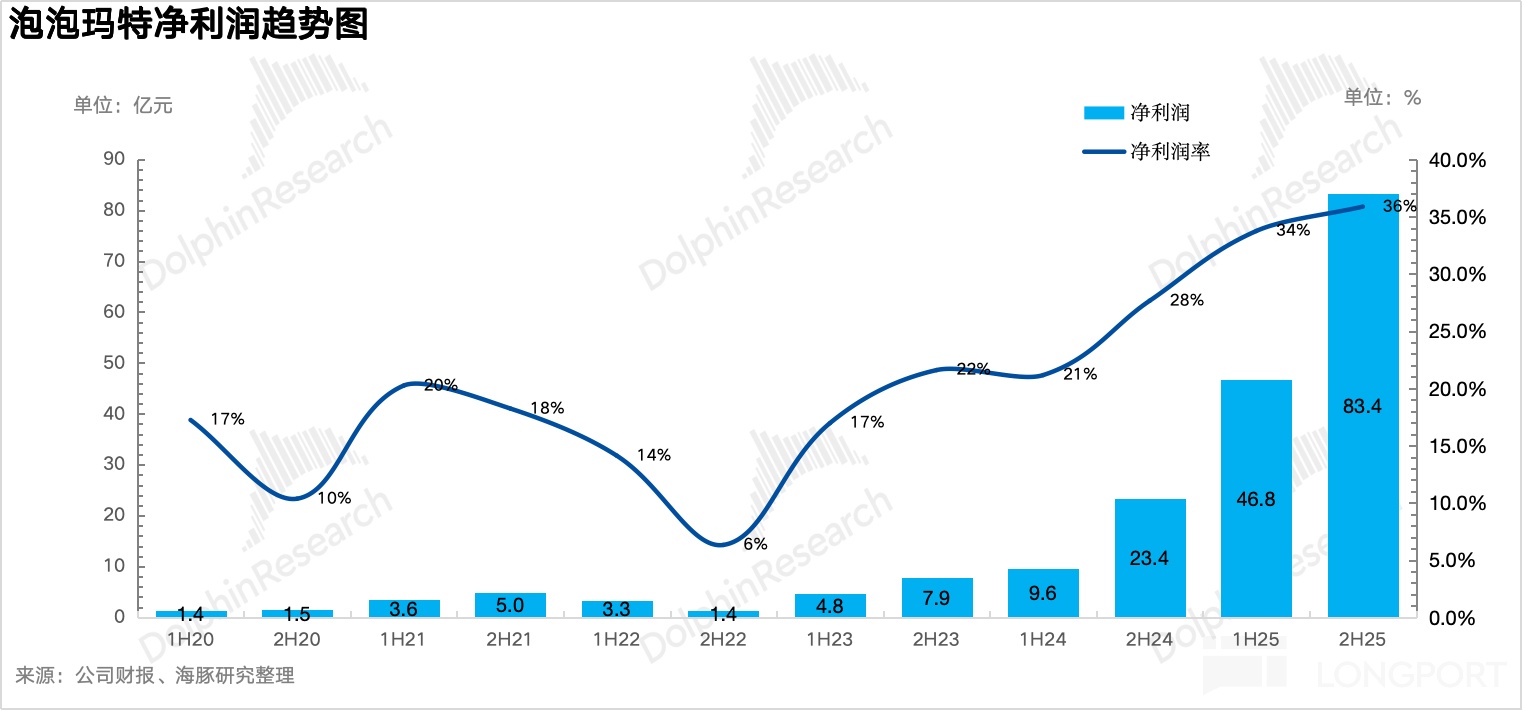

As discussed above, H2 numbers were not bad and at least matched our expectations. In our view, the main reason for the sharp selloff was guidance falling short of expectations.

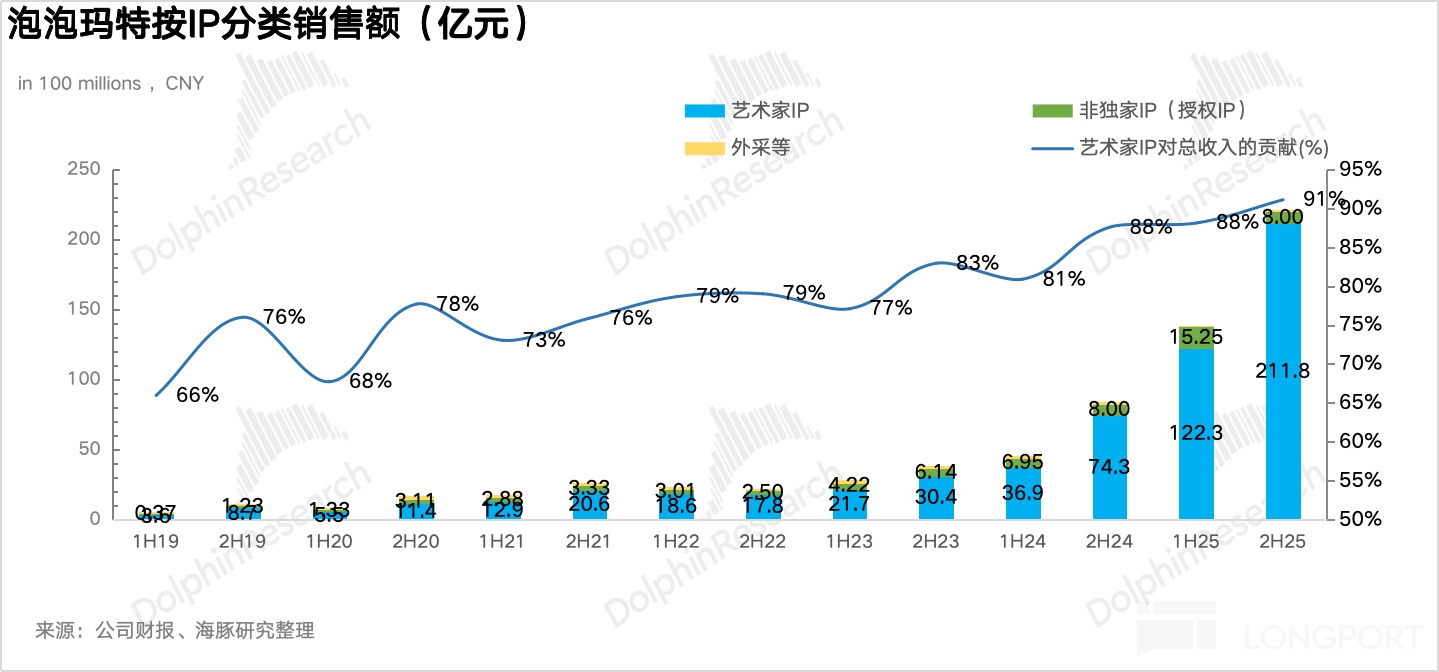

Pop Mart is essentially an IP incubation and distribution platform across the value chain, comparable in model to a streaming platform like Netflix. If Netflix fears a content gap, Pop Mart worries most about IP aging and pipeline gaps. The business moved from Molly to SKULLPANDA, Dimoo, and The Monsters, and any gap without a breakout hit would immediately dent growth—similar to Netflix in a light content year.

From that lens, The Monsters surpassing 40% mix is not ideal, as any drop in LABUBU heat without a comparable successor would have a large impact on earnings. In fact, at least in China, secondary-market prices, search volumes, and topic heat all point to a clear downtrend for LABUBU. We see this as the key reason behind the sharply slower guidance.

To mitigate that risk, Pop Mart has visibly accelerated new-IP launches since Q4 last year. While Supertutu and After-school Merodi saw lukewarm reception, the company’s industrialized 'star-making' system—sourcing ideas from global artists, quickly assessing potential via an internal select-test-scale mechanism, then leveraging strong channels and supply chain—has proven successful. With stepped-up IP creation, we believe it is only a matter of time before a new breakout akin to Xing Xing Ren emerges.

On valuation, with the LABUBU-driven hyper-growth phase now behind us, the model shifts to a more ops-intensive approach to lift store productivity. Based on management’s 2026 profit growth target of 20%, net profit of RMB 15.6bn, and the post-plunge multiple of only ~13x, the stock now trades at a plain-vanilla retail valuation that looks unduly punished. As overseas ops improve and IP creation/ops continue, a rerating above 20x (RMB 312bn/HKD equivalent) looks likely.

Management also highlighted a 5-year roadmap toward an IP-centric group structure (theme parks, film & gaming). The current valuation does not reflect that optionality, and any upside surprise in group-level execution would represent additional rerating room.

Detailed earnings review below:

I. Overseas revenue below expectations

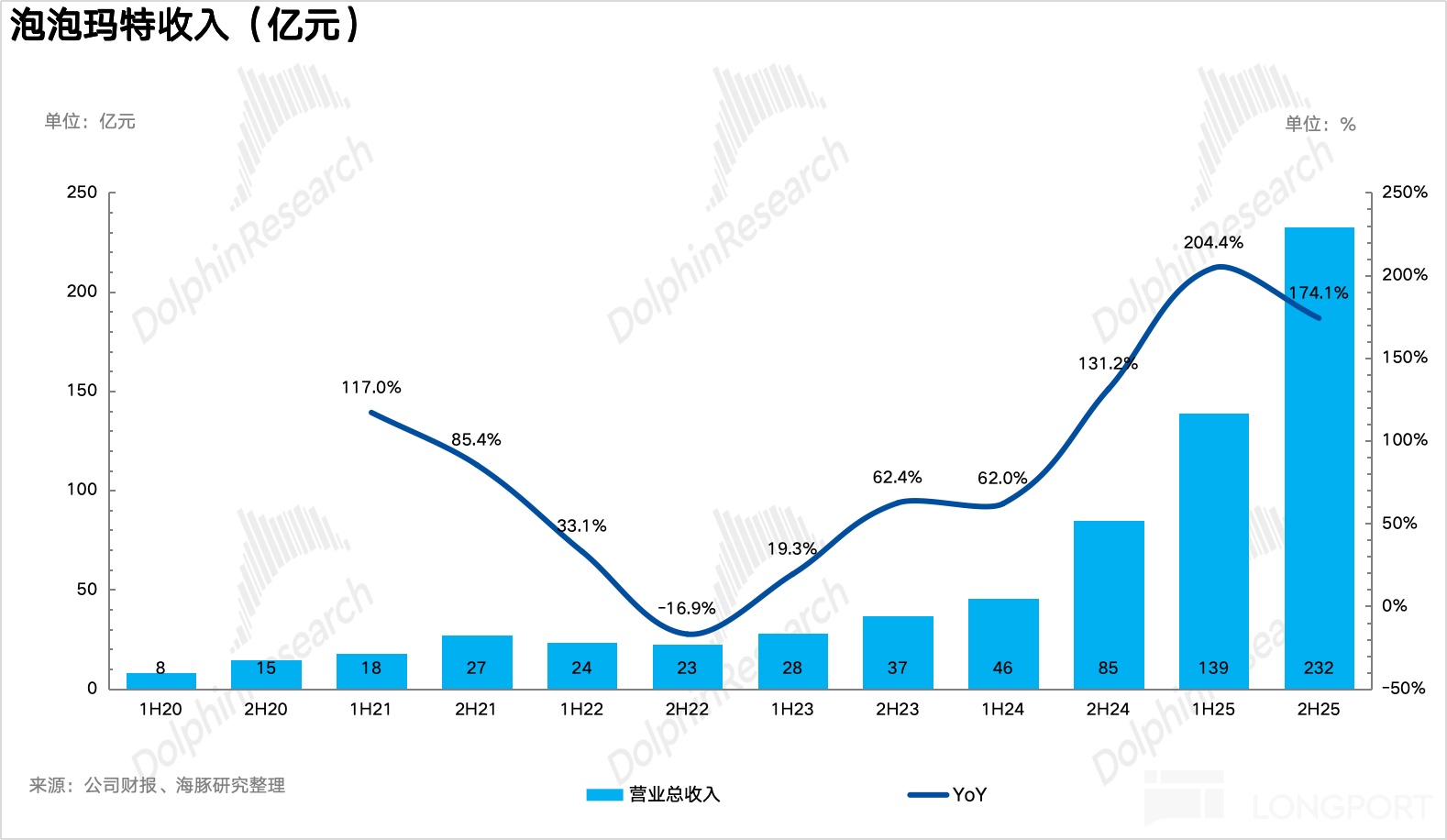

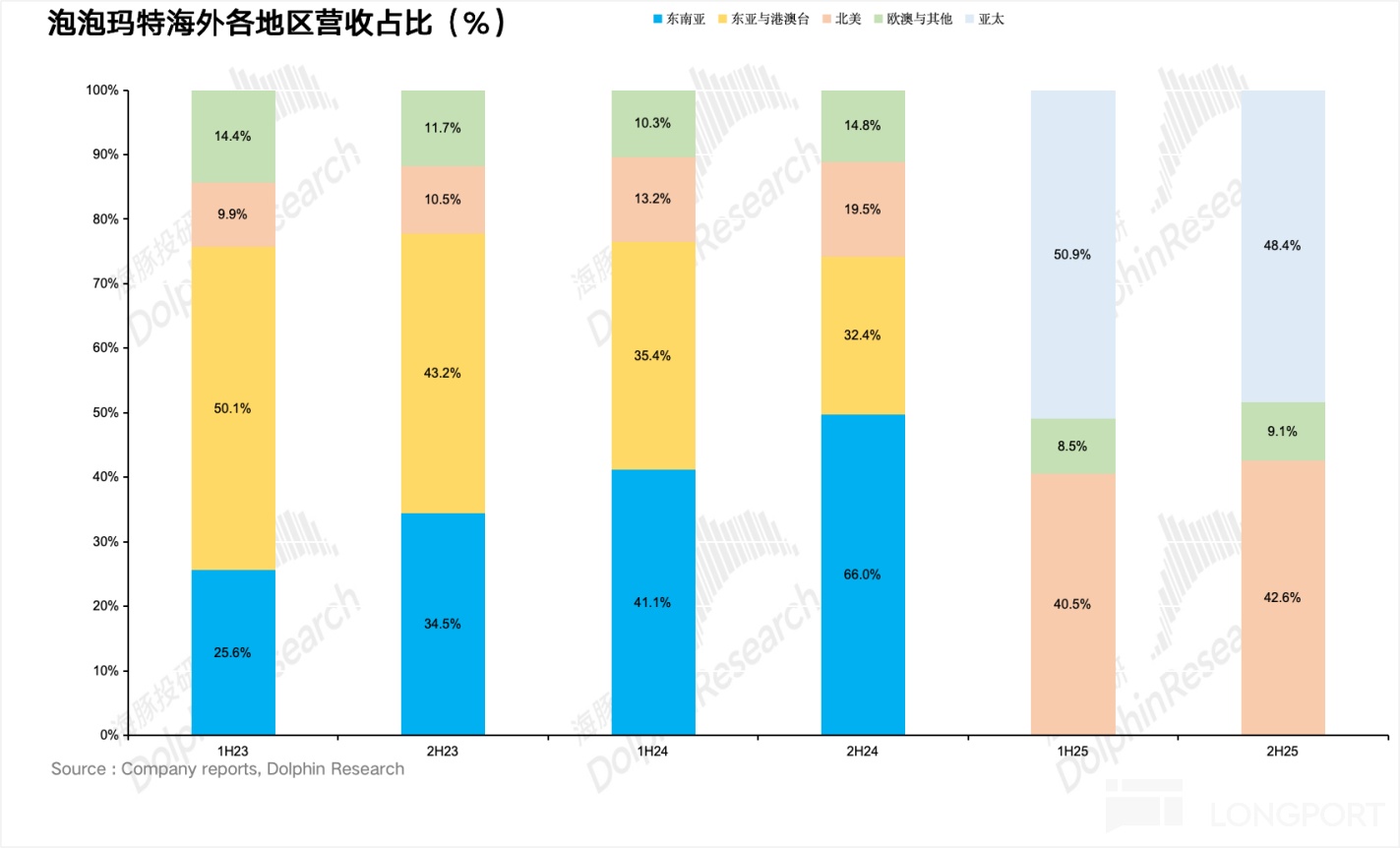

In 2H25, Pop Mart delivered total revenue of RMB 23.24bn (+174% YoY). Overseas revenue reached RMB 10.67bn (+281% YoY), with growth decelerating vs. 1H, and mix rising from 40% in 1H to 46%.

North America: 2H revenue was RMB 4.54bn (+733% YoY), with mix jumping from below 20% a year ago to 43%. Management stepped up collaborations with local artists and streetwear brands, and visibility in mainstream cultural moments such as Thanksgiving parades improved affinity, making North America the market with the highest single-store productivity and fastest growth globally (per-store revenue est. RMB 45–50mn).

However, rapid store rollout in North America temporarily outpaced refined ops, leading to weaker offline trends after Nov. Black Friday did not deliver the expected spike, growth fell below 500%, and this constrained overseas performance.

Europe: After nearly a year of testing, Pop Mart expanded in the UK, France, Spain, the Netherlands, Denmark, and Belgium in 2H. Revenue reached RMB 970mn (+135% YoY), now close to a 10% mix.

Asia-Pacific: Revenue was RMB 5.16bn (scope changed; no YoY comparison). Thailand and Singapore shifted from a 'hyper-growth' phase to 'steady growth,' tempering momentum, and Southeast Asia’s rainy season weighed on offline footfall.

Domestic revenue reached RMB 12.57bn (+183% YoY), accelerating vs. 1H. Drivers included higher mix of premium-ticket items such as LABUBU mini (RMB 99–149) and Halloween plush (RMB 199–299). In addition, broader IP peripherals (accessories, stationery, desserts) lifted ARPU among members.

II. Faster overseas store rollout

In 2H, Pop Mart added a net 72 overseas stores, primarily in North America. By end-2025, North America had over 60 stores across NYC, Los Angeles, Chicago, Miami, etc. In Dec, the first Canadian store opened in Vancouver, kicking off the second key market in North America, with Toronto planned for early 2026 to complete coverage of core cities on both coasts.

Strategically, most new stores in 2H were full-standard long-term flagships with larger footprints, designed to absorb LABUBU-driven traffic.

In Europe, 18 net stores were added in 2H, an acceleration vs. 1H. By end-2025, the company covered the UK, France, Germany, Italy, the Netherlands, and Spain, making Europe the second growth engine overseas.

APAC saw 16 net new stores; with a higher base, focus shifted to format upgrades. In Dec, Pop Mart opened its first store in Manila, filling the last strategic gap in Southeast Asia.

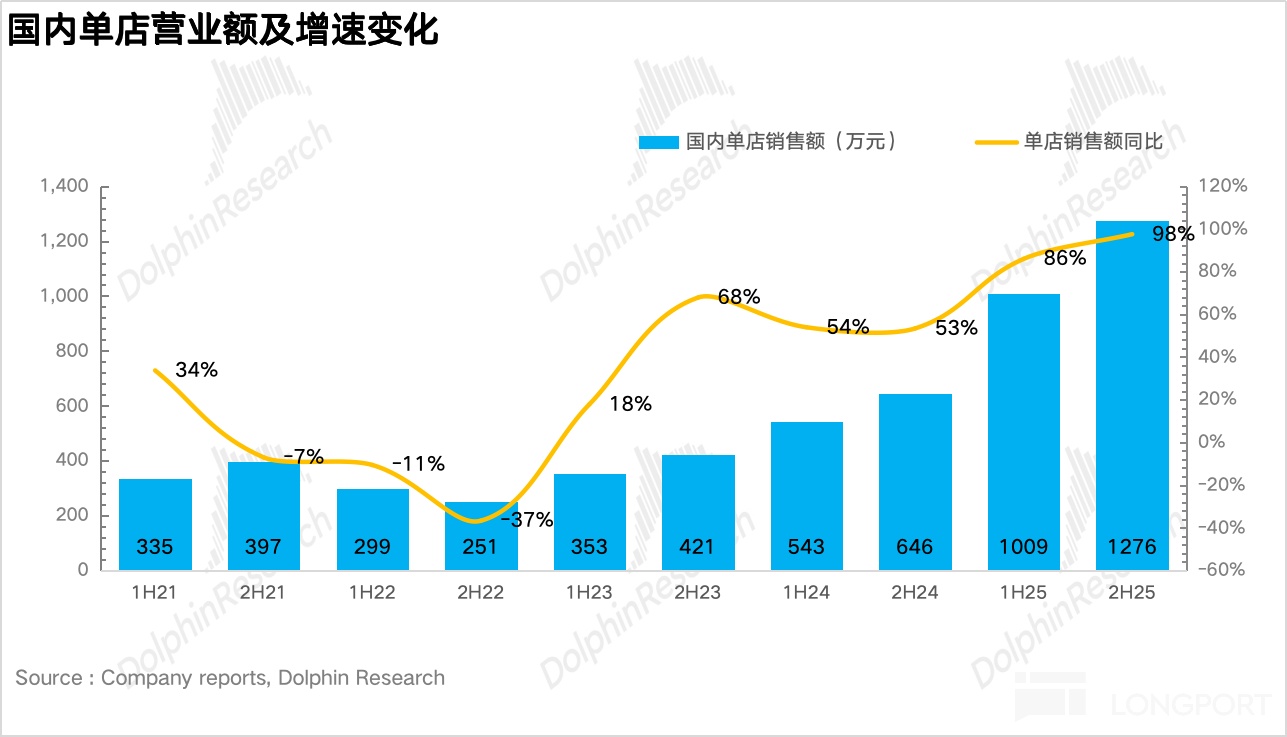

Domestically, Pop Mart closed underperforming neighborhood and basement stores and upgraded into high-end malls, cultural-tourism landmarks, and top shopping centers, resulting in just two net new stores in 2H. This is far slower than overseas, concentrating resources on international expansion. The limited net adds imply domestic store count is near saturation, and future gains will rely on refined ops to lift store productivity.

At the single-store level, upgrades and category expansion drove average domestic per-store revenue to an estimated RMB 12.76mn in 2H (+98% YoY), with both traffic and basket size up sharply YoY.

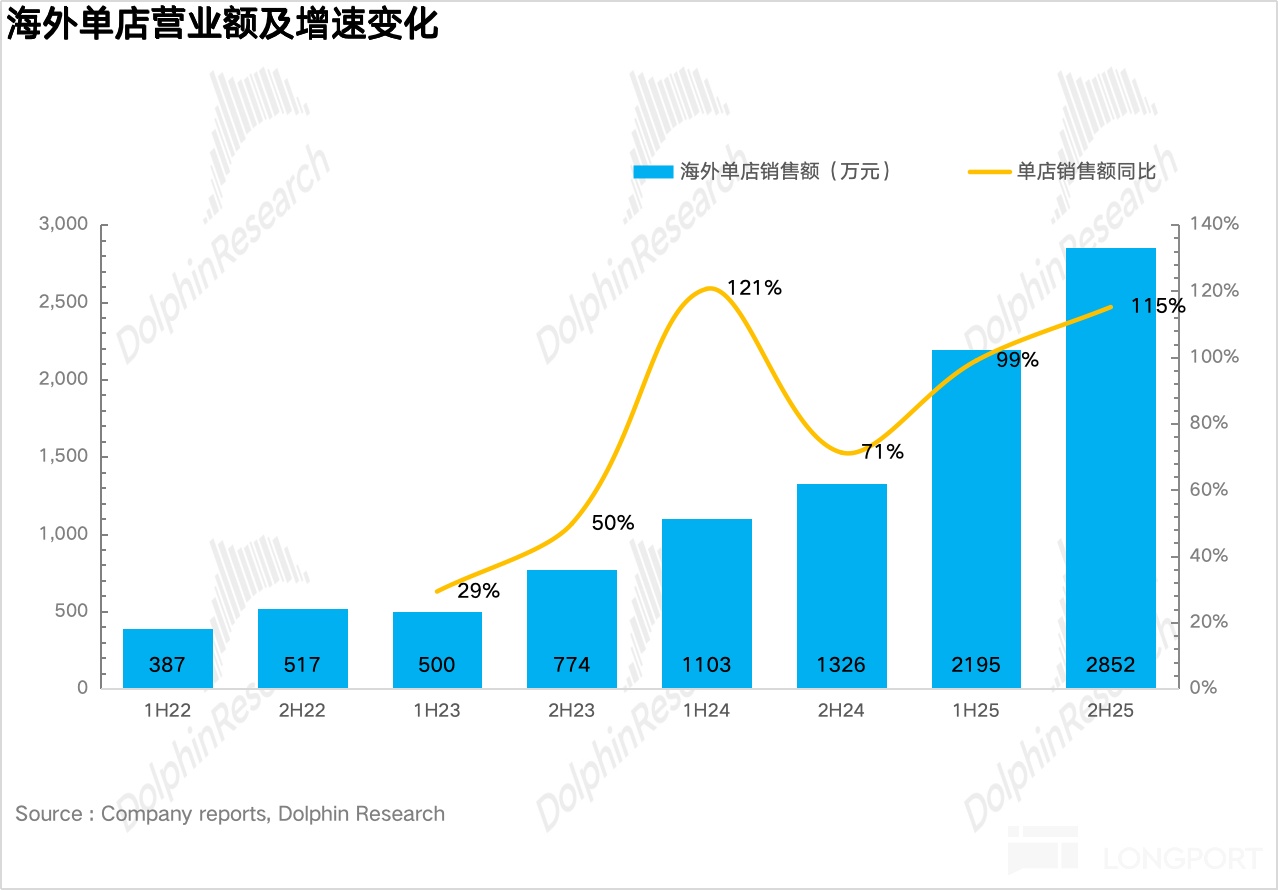

Overseas per-store revenue averaged RMB 28.52mn (+115% YoY). The gap vs. domestic narrowed, mainly because overseas store openings accelerated materially in 2H.

Overall, while overseas white space remains, stores are ultimately conversion venues; if product heat cools and sales slow, stores can become a drag, so the core variable remains IP heat sustainability.

III. The Monsters mix climbed further

By IP contribution, as LABUBU’s 2H capacity bottlenecks eased, The Monsters mix rose from 34% in 1H to 42%, a new high, making it the core IP.

Given softer trends in other core IPs like Molly and Dimoo with share declines, maintaining 2025’s explosive growth into 2026 would be difficult without either a blocks-category boom or a new top-tier IP.

Meanwhile, Xing Xing Ren—the key push domestically—saw mix up from 3% in 1H to 7%, with full-year revenue expected at RMB 2.5bn. As overseas markets are still early in recognizing Xing Xing Ren, a 2026 ramp abroad should help offset domestic growth moderation.

IV. Plush secured the No.1 category spot

By product mix, blind-box figurines kept losing share while higher-margin plush surged. Beyond LABUBU, other flagship IPs are also moving into plush, lifting the overall plush mix from 44% in 1H to 54%. POP BLOCK doubled vs. 1H on launches such as Molly Architecture and LABUBU Forest, and momentum remains strong.

V. Online mix rose significantly

Channel-wise, Pop Mart increased livestream frequency on Douyin and other platforms in 2H, driving a notable uplift in online conversion. It also added more features to the official WeChat mini-program (e.g., team draws, disclosed odds for rare pieces), which concentrated and activated private traffic, taking online revenue up more than 200% YoY, outpacing the market.

VI. GPM hit a record high

With the share of higher-margin overseas sales rising (overseas GPM roughly 10pts above domestic) and a richer mix of plush, H2 GPM reached 73%, a new high.

VII. Operating leverage expanded; profitability climbed

Sales expense ratio fell 600bps to 21% on better online acquisition efficiency, while G&A fell 400bps to 6% on disciplined investment. Core OPM rose to 48%, a record high.

Related articles:

Earnings Season

Mar 26, 2025 earnings take: Pop Mart: Running the sewing machine hot—can the rally continue?

Mar 26, 2025 earnings take: Pop Mart: Overseas legend—an unstoppable surge?

Aug 20, 2024 earnings take: Pop Mart: Is PDD’s overseas push too low-end? Style matters abroad

Aug 21, 2024 call notes: 'Sprinting' Pop Mart: '60%+ full-year growth; 200% overseas'

Mar 28, 2022 earnings take: Pop Mart: Even trend toys can’t escape the squeeze

Mar 28, 2022 call notes: Pop Mart’s new magic trick?

Deep Dives

Nov 28, 2024: Pop Mart: Just toys—why the grand comeback?

Dec 10, 2024: Pop Mart: Overseas boom, bubble unpopped

Risk disclosure and disclaimer: Dolphin Research disclaimer and general disclosures