Today’s Market Recap: Markets Edge Up Amid Iran Conflict and Fed Rate Scrutiny

Track the Market Trend

TradingKey - The major U.S. stock indices edged higher on Tuesday as investors began to look past the ongoing conflict in Iran, despite persistent energy price pressures. The S&P 500 rose 0.25% to 6,716.09, while the Nasdaq Composite climbed 0.47% to 22,479.53. The Dow Jones Industrial Average also saw a modest gain of 0.10%, closing at 46,993.26.

In the technology and mobility sectors, Micron Technology (MU) surged 4.44% ahead of its upcoming earnings report, fueled by optimism regarding memory chip demand. Uber Technologies (UBER) gained 4.26% following the announcement of an expanded robotaxi partnership with Nvidia (NVDA). Additionally, Qualcomm (QCOM) rose 1.62% after unveiling a $20 billion share buyback program and a dividend increase.

Sector-specific performance was mixed elsewhere. Airline stocks were bolstered by Delta Air Lines (DAL), which jumped 6.56% after raising its revenue guidance. Conversely, Eli Lilly (LLY) fell 5.94% after HSBC downgraded the stock to "reduce" and lowered its growth forecasts for obesity drugs. The Trade Desk also faced selling pressure, slipping 7.44% during the final hours of the session.

Blue Owl Capital (OWL) saw significant activity, closing up 4.45% at $9.15. While there was no specific catalyst for the move, trading volume spiked to 41.8 million shares — 57% above its three-month average. Despite the daily gain, the specialty finance firm remains down 15% since its 2020 IPO. Meanwhile, Tencent Music Entertainment Group plummeted 24.65% to $11.37. Despite beating revenue expectations and showing subscriber growth in its fiscal Q4 2025 results, an earnings miss and declining free user metrics triggered a wave of analyst downgrades. Volume for the China-focused platform reached 63.9 million shares, a staggering 823% above its usual average.

The Federal Reserve commenced its two-day policy meeting today against a volatile backdrop of geopolitical tension and crude oil prices once again topping $100 per barrel. While the central bank is widely expected to maintain current interest rates, market participants are waiting for Chair Jerome Powell’s Wednesday commentary for insights into the economic outlook and future policy shifts.

This cautious market sentiment was further highlighted by Bank of America’s Global Fund Manager Survey for March. The report, released today, indicated that fund managers remain increasingly concerned about global growth and rising inflation, leading to higher cash allocations and continued scrutiny of private credit markets.

Market Headline

U.S. President Donald Trump has stated that military operations against Iran do not require assistance from NATO, Japan, South Korea, or Australia. He noted that most NATO allies expressed a reluctance to get involved, asserting that the United States "does not need anyone's help." This comes as Iran announces its operations have entered an "accelerated phase," following confirmation from Tehran that President Larijani, his son, and a deputy were killed in an airstrike. Consequently, the Director of the U.S. National Counterterrorism Center, Christopher Kent, resigned while attributing the outbreak of war to Israel. Meanwhile, the deployment of the USS Gerald R. Ford in the Middle East may be extended through May, as the Israeli military vows to "hunt down" Iran's newly appointed Supreme Leader.

In response to the escalating conflict, Iran's Supreme Leader has rejected peace proposals with the U.S., insisting that the U.S. and Israel must be defeated and pay reparations. Iran reportedly launched its 59th wave of attacks on Tuesday, targeting U.S. military bases in Qatar, Kuwait, the UAE, Bahrain, and Iraq, with strikes also reported near the Bushehr nuclear power plant. Geopolitical tensions have spiked as the Iranian Parliament Speaker declared that the Strait of Hormuz would not return to its pre-war status. While France, Canada, Greece, and the Netherlands have declined to participate in military actions to reopen the Strait, Iran has significantly increased attacks on Middle East energy infrastructure. This led to a sharp rebound in oil prices; West Texas Intermediate (WTI) jumped over 5% on Tuesday, while Brent crude closed at a three-year high, marking its fourth consecutive day above $100 per barrel.

On the monetary front, "Fed Whisperer" Nick Timiraos suggests the Federal Reserve's focus has shifted from "when to cut rates" to "whether to cut at all." The escalating Middle East crisis has strengthened the consensus for the Fed to hold rates steady. Investors are now closely monitoring three key signals: the language of the policy statement, the "dot plot" projections, and Chair Jerome Powell’s press conference. Any hawkish signals could significantly impact interest rate expectations and the pricing of risk assets.

In trade news, transatlantic tensions may soon ease as the European Union advances the final approval process for a trade agreement with the U.S. The European Parliament's Committee on International Trade is scheduled to vote on the deal this Thursday, with a plenary session vote expected later this month or in April. If approved by Parliament and member states, the agreement would mark a major step in cooling trade frictions between the EU and the U.S.

In the technology sector, Nvidia CEO Jensen Huang highlighted during a GTC interview that low-latency inference is set to become the next explosion engine for the AI economy. He noted that AI models are transitioning from "generating information" to "executing tasks," creating real economic value. Huang also warned that a tight balance between the supply and demand of power, chips, and data centers will likely persist as a long-term industry characteristic.

Amazon CEO Andy Jassy projected during an internal all-hands meeting that AI could drive AWS annual sales to $600 billion by 2036 — doubling his previous forecast. Jassy defended the company’s $200 billion capital expenditure plan, stating that AI represents a rare opportunity to build a business of massive scale based on clear and strong demand signals.

The global chip supply faces a new threat as Samsung Electronics' largest union (SELU) prepares for its largest strike in history. The union plans an 18-day walkout starting May 21, which could impact roughly half of the chip production capacity at the Pyeongtaek campus. Analysts warn that this labor dispute, combined with aggressive talent poaching from competitors, could jeopardize Samsung’s earnings momentum and further strain the global semiconductor supply chain.

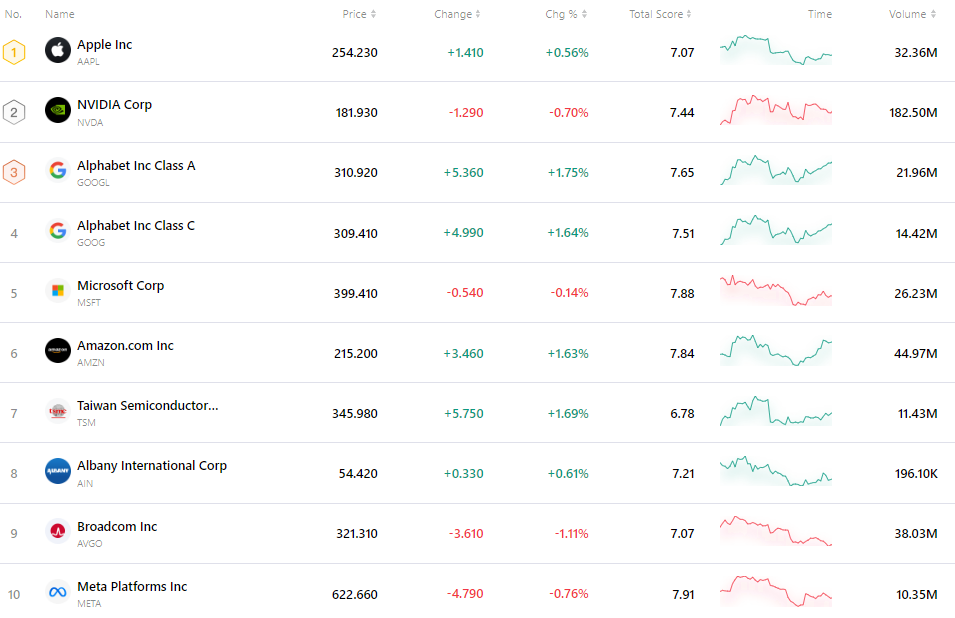

Top 10 Most Traded Stocks

The chart below lists the ten most actively traded stocks in the market. Due to their massive trading volumes and high liquidity, these stocks serve as critical benchmarks for tracking global market dynamics.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.