Middle East Conflict Persists, Asian Stocks Plunge on Risk Aversion, Local Markets Show Resilience

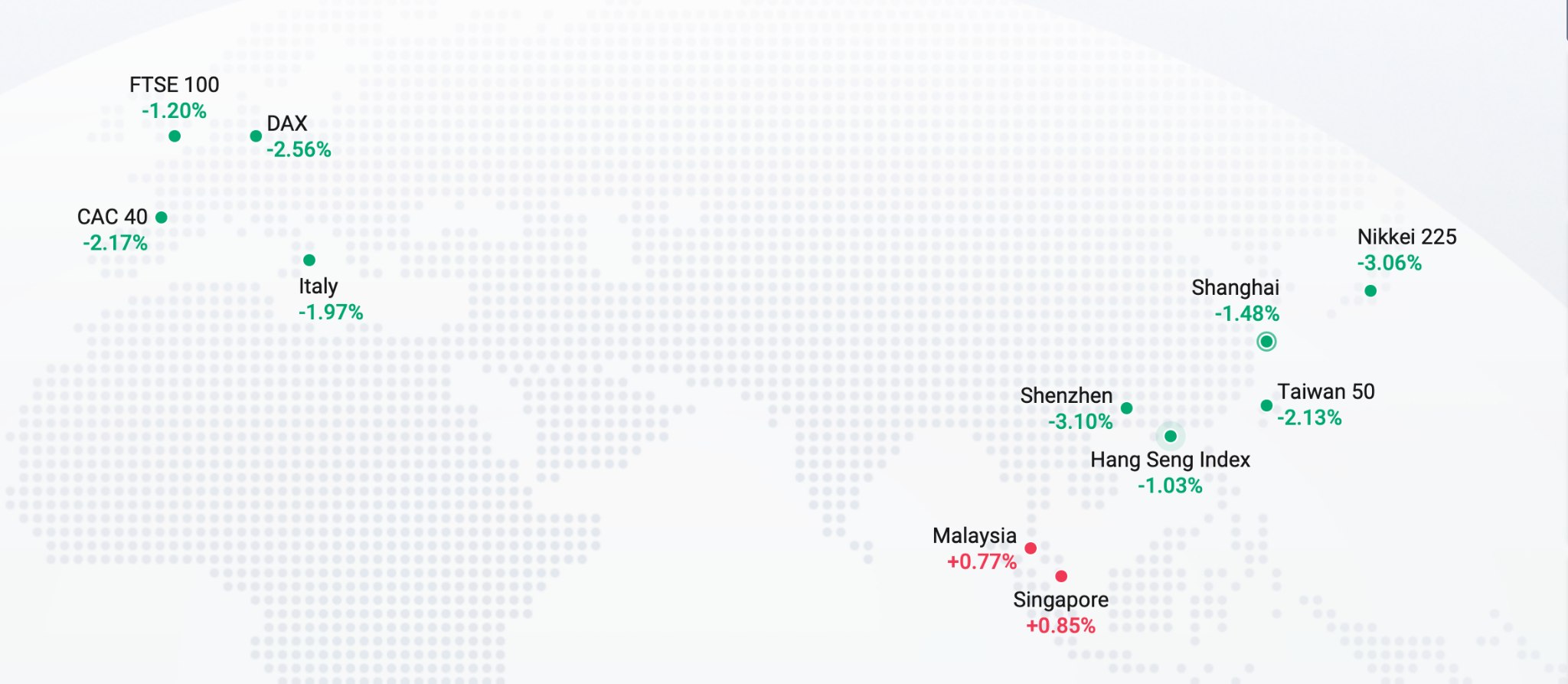

TradingKey - During the Asian trading session, Asia-Pacific equity markets plummeted, with the Nikkei 225 falling over 3.3% to 56,124. The TOPIX dropped 3.3% to 3,769 points. The KOSPI closed down sharply by 7.2% at 5,792.2 points. The Shanghai Composite Index fell over 1.4%, the Shenzhen Component Index dropped more than 3%, and the Hang Seng Index declined over 1%.

Singapore and Malaysian equity markets showed resilience, with both the FTSE Straits Times Index and the FTSE Bursa Malaysia KLCI rising over 0.7%.

International oil prices rose again by over 2%, while gold gains narrowed and silver tumbled more than 5%.

It is worth noting that the KOSPI recorded its largest single-day drop since August 5, 2024, with Hyundai Motor falling nearly 12% and SK Hynix dropping over 11%.

Tensions in the Middle East show no signs of easing. On March 2 local time, Iranian media reported that Jabbari, a commander of the Islamic Revolutionary Guard Corps, stated that any vessel attempting to pass through the Strait of Hormuz would be destroyed, adding that Iran would not allow a single drop of oil to leave the region.

A senior U.S. military official stated that Iran has not patrolled the Strait of Hormuz nor implemented blockade measures. Currently, there is no evidence of sea mines in the relevant waters, although commercial vessels are navigating the area with caution.

Market expectations for oil prices have further intensified. Related assets have provided localized resilience for global equity markets, though the overall market remains under pressure.

Timothy Moe, Chief Asia-Pacific Equity Strategist at Goldman Sachs, said in a media interview that the Middle East situation could serve as a catalyst for an "overdue technical correction" in the market. However, from a strategic perspective, he viewed this as an opportunity to position in Asian assets, as the region's fundamentals remain constructive.

This content was translated using AI and reviewed for clarity. It is for informational purposes only.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.