The Week on Wall Street: Fed’s Emergency Cut and Tariff Rulings Spark Sector Rotation Amid Macro Strains

Previous Week’s Market Review & Analysis

TradingKey - The macroeconomic landscape presented a mixed picture, with initial Q4 2025 real GDP estimates at a lower-than-expected 1.4%, partly due to a 43-day government shutdown. Inflation remained a concern, as Core PCE printed an unrounded 0.355% month-over-month (0.4% rounded), the largest monthly increase in a year. Producer prices also turned higher. However, January 2026 CPI inflation fell to 2.4% year-over-year, and core inflation moderated to 2.5% year-over-year. The Federal Reserve executed an emergency 50-basis-point rate cut, the first inter-meeting cut since March 2020, citing "recent strains in financial markets" and a need to maintain stability following three bank failures. Geopolitical tensions with Iran added to market uncertainty. The Supreme Court striking down White House tariffs initially injected uncertainty but markets rallied on the news, overshadowing sticky inflation and disappointing Q4 GDP. However, the administration signaled alternative tariff measures are being pursued. January 2026 nonfarm payroll employment rose by 130,000, with the unemployment rate at 4.3%. Job gains were concentrated in health care, social assistance, and construction, leading some Fed officials to question the broader strength of the labor market.

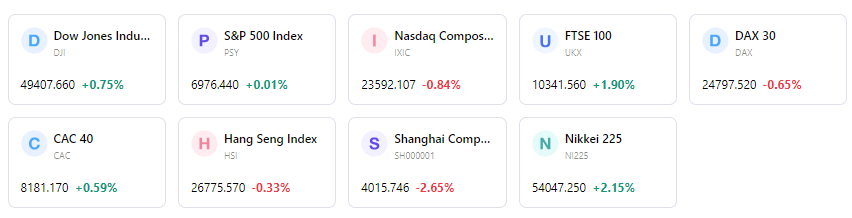

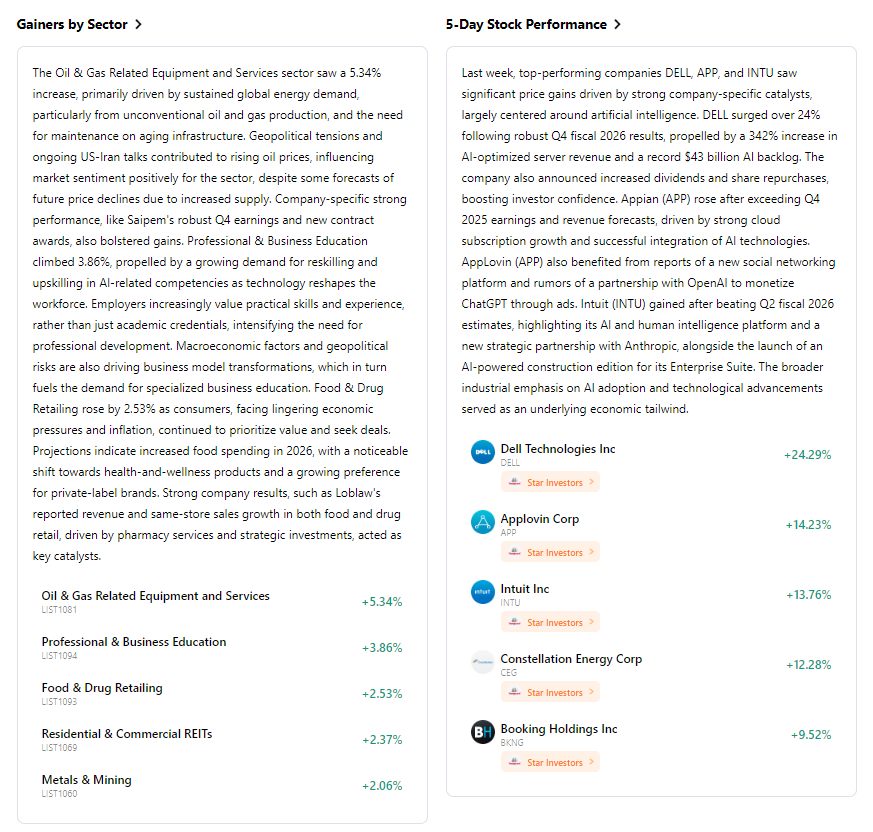

Market performance saw a choppy week ending in the green. The S&P 500 advanced 1.07%, the Nasdaq Composite rallied 1.51%, and the Dow Jones Industrial Average inched up 0.25%. A notable sector rotation is underway, with industrials, consumer defensives, and energy stocks leading the market higher, while technology, communication services, consumer cyclicals, and financials have underperformed. Energy stocks were up over 22% year-to-date through February 18, and industrials up 16.05%. The week's key events included a speech from Fed Governor Waller on February 23, the Supreme Court's tariff ruling, and several corporate earnings, including Ovintiv and Viatris. Fund flows and sentiment were impacted by the emergency Fed cut, as the VIX rose, signaling increased fear, and the dollar saw a significant drop against the euro. Overall, the market exhibited a disconnect between robust equity performance (particularly in specific sectors) and underlying economic concerns, amplified by unexpected monetary policy action and persistent inflation.

Next Week's Key Market Drivers & Investment Outlook

Upcoming events include a heavy slate of economic data, with the ISM Manufacturing Index on Monday, March 2, JOLTS Job Openings on Tuesday, March 3, and the ADP Employment Report, ISM Non-Manufacturing Composite, and the Federal Reserve's Beige Book on Wednesday, March 4. The week culminates with the crucial Employment Report, including Non-Farm Payrolls, Unemployment Rate, and Average Hourly Earnings, on Friday, March 6. Corporate earnings season continues, with RadNet reporting Monday, March 2, after the close, and a large number of companies, potentially including some of the Magnificent Seven (e.g., Nvidia), scheduled throughout the week, particularly on Thursday, March 5.

Market logic projection anticipates continued focus on labor market data and inflation indicators to assess the Fed's policy path, especially after the recent emergency rate cut. The rotation into "real economy" sectors is expected to persist. Strategy recommendations lean towards a continued overweight in industrials, consumer defensives, and energy, given their relative outperformance. Risk alerts include the potential for ongoing financial market instability following the emergency Fed action, the uncertain impact of evolving trade policies, and the implications of concentrated job growth on overall economic health.

Markets Weekly

5-Day Index Performance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.