BHP Group Ltd Stock Moved Up by 3.36% on Feb 11: A Full Analysis

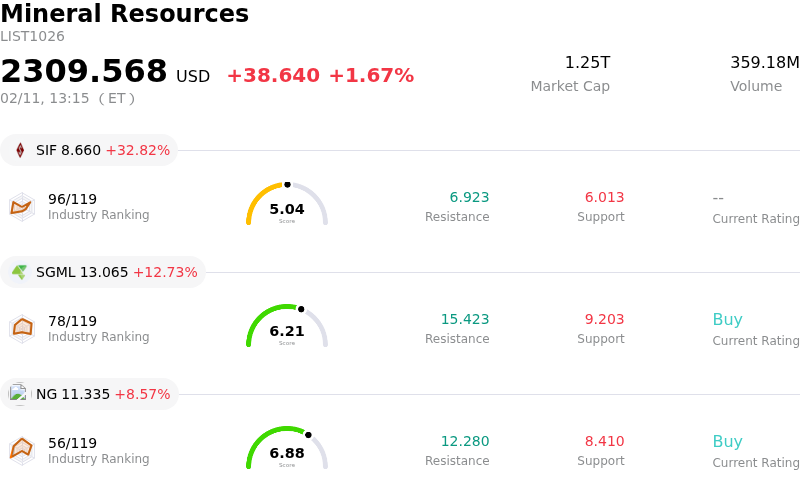

BHP Group Ltd (BHP) moved up by 3.36%. The Mineral Resources industry is up by 1.67%. The company outperformed the industry. Top 3 gainers of the industry: SIFCO Industries Inc (SIF) up 32.82%; Sigma Lithium Corp (SGML) up 12.73%; NovaGold Resources Inc (NG) up 8.57%.

BHP's share price saw a positive movement today, largely driven by a combination of company-specific operational improvements, a strong outlook for key commodities, and supportive macroeconomic factors.

A significant contributing factor is the company's recent announcement regarding a productivity upgrade to its Western Australian iron ore haul trucks. This enhancement is projected to substantially increase iron ore output annually, translating into tens of millions of dollars in additional revenue, which directly impacts the company's financial prospects. This operational improvement builds on BHP's already strong iron ore production, with its Western Australia operations recognized as a low-cost producer globally, and stable guidance for the fiscal year 2026.

Furthermore, the company's focus on copper, a critical "future-facing" commodity, is bolstering investor confidence. BHP recently upgraded its group copper production guidance for fiscal year 2026 following strong output in the first half of the year. The company is also actively increasing its investment in copper projects, notably in Argentina, signaling a strategic push into this high-demand metal. The broader market for copper remains robust, supported by strong global demand tied to the energy transition and the expansion of AI-driven data centers, despite some short-term demand fluctuations. Industry analysts continue to see a positive long-term trend for copper.

The overall mining sector outlook for 2026 remains stable, with supportive commodity prices. While iron ore prices have shown some volatility, they are expected to maintain a firm bias in the short term due to recovering demand. Macroeconomic conditions are also playing a role, with a weaker US dollar providing additional support for dollar-denominated commodities like copper, benefiting resource companies. Analyst forecasts are positive, indicating strong year-over-year earnings growth for BHP in fiscal year 2026.

The observed intraday volatility could be attributed to typical market fluctuations in commodity prices throughout the day and varying reactions to general macroeconomic data releases. However, the prevailing sentiment appears to be driven by the company's strategic positioning in critical commodities and its operational efficiency improvements.

Technically, BHP Group Ltd (BHP) shows a MACD (12,26,9) value of [2.44], indicating a buy signal. The RSI at 63.86 suggests neutral condition and the Williams %R at -24.47 suggests oversold condition. Please monitor closely.

BHP Group Ltd (BHP) is in the Mineral Resources industry. Its latest annual revenue is 51.26B, ranking 3 in the industry. The net profit is 9.02B, ranking 2 in the industry. Company Profile

Over the past month, multiple analysts have rated the company as HOLD, with an average price target of 57.97, a high of 73.00, and a low of 48.00.

Company Specific Risks:

- Macquarie downgraded BHP to "neutral" due to a bearish outlook on iron ore price trends, anticipating market weakness in fiscal years 2026 and 2027, despite recent strong operational performance.

- Berenberg issued a "Sell" rating, citing concerns over structurally higher capital expenditure, an "expensive" dividend no longer adequately covered by free cash flow, and a projected increase in net debt exceeding the company's target range by 2030.

- BHP faces ongoing pricing pressures from China, including restrictions on Jimblebar iron ore imports and potential annual losses of up to $1 billion from incremental discounts on iron ore fines products due to protracted negotiations.

- The Jansen Potash Project Stage 1 has experienced significant cost escalation, with the total investment estimate rising to US$8.4 billion, indicating potential capital misallocation and project execution risks.