Today’s Market Recap: S&P Retreats, Financials Hit Hard as AI Tools Rattle Traditional Players

Track the Market Trend

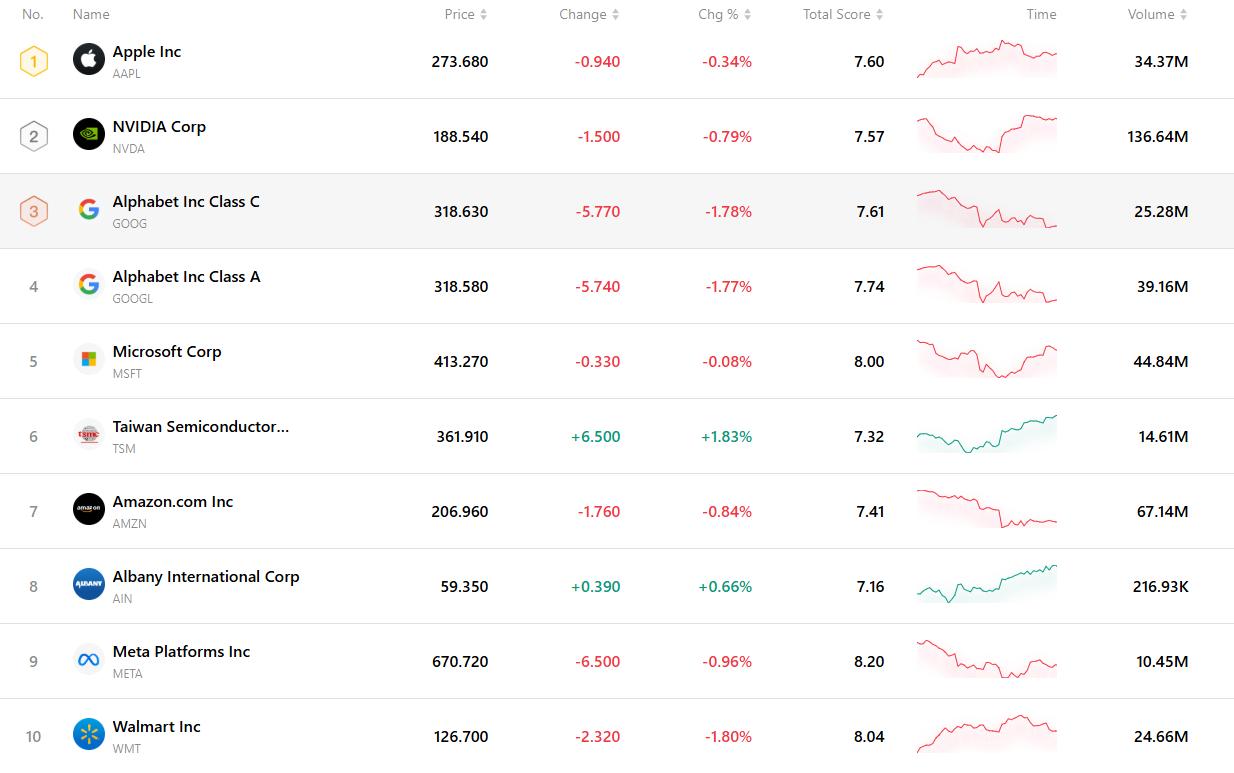

TradingKey - On February 10, 2026, U.S. equity markets ended the day in negative territory. The S&P 500 declined 0.33% to close at 6,941, while the Nasdaq Composite slipped 0.59%, finishing at 23,102.

Performance across e-commerce and cloud names was mixed. Alibaba Group (BABA) advanced 2.15% to $166.51, driven by strength in international retail momentum, while Walmart (WMT) slid 1.80% to $126.70 amid broad-based selling in U.S. consumer staples, highlighting the divergence between global and domestic narratives in both retail and cloud verticals.

Microsoft (MSFT) closed nearly flat at $413.27, down 0.08%. The stock remained range-bound as markets weighed a downgrade from Melius—citing near-term AI investment pressure—against bullish commentary emphasizing Microsoft’s long-term AI monetization potential.

Amazon (AMZN) declined 0.84% to settle at $206.90. Investors continued evaluating the company's aggressive $200 billion capital expenditure outlook for 2026, especially in AI and AWS infrastructure. Despite strong recent cloud growth and promising progress in AI content licensing, caution lingered around margin and earnings outlook.

Fresh uncertainty surrounding the impact of emerging generative AI tools triggered a selloff in financial service names, with Charles Schwab (SCHW) falling over 7%, reflecting broader concerns about automation in wealth management.

Memory-related semiconductor stocks also faced selling pressure. SanDisk (SNDK) dropped more than 7%, underperforming the broader tech sector on fears of softer demand and pricing headwinds.

Bitcoin (BTCUSD) traded lower during the session, falling nearly 4% from the intraday peak and briefly dipping below the $68,000 level, as crypto markets pulled back in line with broader risk sentiment.

Market Headline

Fears of AI disruption continue to rattle markets, expanding from software to financial services. Wealth management stocks sold off sharply on Tuesday after fintech platform Altruist unveiled a new AI tool designed to automate advanced tax strategies—a core offering of traditional advisors. Charles Schwab plunged more than 9% intraday, reflecting investor anxiety over long-term disintermediation. The selloff echoed Monday’s sharp losses in insurance brokerage stocks, triggered by Insurify’s AI launch, which sent the S&P 500 Insurance Index down nearly 4%—its steepest one-day decline since October 2025.

Alphabet’s record-breaking bond sale signals growing AI-driven capital needs. Alphabet’s 100-year sterling-denominated bond drew more than seven times the demand, raising nearly $32 billion across multiple currencies, including the company’s first-ever issuance in Swiss francs. As the first major tech firm to issue a 100-year bond since the dot-com era, Alphabet is leveraging public debt markets to fund its expanding investment in artificial intelligence. The offering—part of its broader multi-currency financing strategy—highlights rising capital demands among top-tier tech firms. Despite inherent long-term risk, investor demand showed continued confidence in Alphabet’s financial strength and dominance in the next wave of digital infrastructure.

Paramount (PARA) intensifies its hostile pursuit of Warner Bros. (WBD) with revised offer terms. Paramount Global is ramping up efforts in its unsolicited bid to acquire Warner Bros. Discovery, sweetening the offer by pledging to cover up to $2.8 billion in Netflix-related termination fees. The company also committed $1.5 billion in debt refinancing guarantees and introduced a quarterly “delay fee” of $0.25 per share should negotiations drag on. However, the all-cash offer remains at $30 per share, and analysts suggest that without a meaningful increase above $32 per share, the Warner Bros. board is unlikely to endorse the deal.

Coca-Cola (KO) signals slower growth ahead after a steep quarterly earnings hit. Coca-Cola’s Q4 GAAP operating income fell 32% year-over-year, primarily due to a $960 million non-cash impairment tied to its acquisition of sports beverage brand BodyArmor. For full-year 2026, the company projected organic revenue growth between 4% and 5%, falling slightly short of Wall Street’s consensus of 5.01% at the low end. After several years of price-driven growth, investors are becoming cautious about weakening consumer demand, particularly as inflation fatigue and price sensitivity begin to affect consumption patterns in the global beverage market.

Top 10 Most Traded Stocks

The chart below highlights the ten most actively traded stocks in the current market. With their substantial trading volumes and high liquidity, these names serve as key benchmarks for tracking global market dynamics.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.