The Week on Wall Street: Market Wavers Between AI Euphoria and Rate Uncertainty

Previous Week’s Market Review & Analysis

• Macroeconomic Landscape:

The Federal Reserve maintained interest rates at 3.50% to 3.75% at its January meeting, a widely anticipated decision, with Chair Powell indicating a hold on policy while keeping future cuts open for later in 2026. Inflation data showed a mixed picture: the December wholesale inflation report was warmer than expected, with the Core Producer Price Index (PPI) jumping 0.7% month-over-month. However, the US annual inflation rate in February remained relatively stable at 2.8%, with core prices up 0.2% month-over-month and 3.1% annually. The labor market presented a subdued outlook, with the December jobs report revealing sluggish growth of 50,000 jobs and downward revisions of 76,000 from previous months. The unemployment rate edged down to 4.4%. US job openings fell in December to 6.5 million, the lowest in over five years. Consumer sentiment weakened materially, with the Consumer Confidence Index dropping to 84.5 in January from 94.2 in December. However, the University of Michigan consumer sentiment index showed a 0.9 point increase to 57.3 in February, driven by current conditions, though sentiment stagnated for non-stockholding consumers. Geopolitical tensions related to Iran also influenced markets.

• Market Performance Overview:

The U.S. equity markets experienced mixed performance over the week. The S&P 500 managed a slight gain of approximately 0.3%, closing at 6940, partially recovering with a 0.5% rise on Monday, February 2, snapping a three-day losing streak. In contrast, the Nasdaq Composite edged down 0.17% for the week, notably sliding 0.9% on Friday, February 2, while the Dow Jones Industrial Average declined 0.42%. Sector performance saw Energy outperform due to Iran tensions. However, Technology, Materials, and Industrials declined on Friday, February 2, whereas Consumer Staples recorded a 1.4% gain. Concerns around software companies' earnings also contributed to market declines later in the week. There was a discernible rotation towards small-cap and value stocks, with Industrials, Energy, and Consumer sectors benefiting.

• Key Events Analysis:

The Federal Reserve's decision to hold rates steady was a central event, having little immediate effect on U.S. stock markets. The fourth-quarter corporate earnings season was in full swing, with approximately one-third of S&P 500 companies reporting. A solid 75% surpassed EPS estimates, and 65% exceeded revenue forecasts, contributing to a 12% year-over-year earnings growth. However, disappointing earnings from a megacap tech firm unsettled investors, impacting the Nasdaq on Thursday. Notably, Microsoft shares declined despite beating profit estimates due to concerns over cloud growth and AI spending, while Meta shares surged on strong results and increased AI investment guidance. A significant policy development was President Trump's nomination of Kevin Warsh as the next Fed chair, which led to a reassessment of monetary policy expectations and contributed to rising Treasury yields. This nomination was seen to suggest a potentially more cautious approach to future rate cuts. The January 2026 jobs report was notably delayed due to a government shutdown.

• Flows & Sentiment:

Market sentiment was influenced by a mix of factors. The CBOE Volatility Index (VIX) rose 3.3% to 17.44 on Friday, February 2, indicating heightened fear. Gold and silver prices came under significant pressure, falling sharply after the Kevin Warsh nomination, driven by rising Treasury yields and a stronger U.S. dollar. Gold futures dropped over 11%, and silver futures plunged more than 31%, with gold briefly sinking below $4,500 per ounce on Monday, February 2. Overall consumer sentiment weakened in January, though an improvement in current conditions was noted in the University of Michigan's February sentiment data.

• Overall Assessment:

The week was characterized by market choppiness, with investors navigating mixed corporate earnings, rising Treasury yields, and the uncertainty surrounding the newly nominated Fed Chair. The market displayed a logic of shifting from high-beta to yield/value stocks, with an increasing discernment regarding companies' ability to generate profits from AI investments.

Next Week’s key market drivers & Investment Outlook

Upcoming Events:

The coming week will feature several key economic data releases, including the Employment Cost Index for Q4 2025 and U.S. Import and Export Price Indexes for December 2025 on Tuesday, February 10, 2026. The delayed Employment Situation report for January 2026, including average hourly earnings, nonfarm payrolls, and the unemployment rate, is scheduled for Wednesday, February 11, 2026. The Consumer Price Index (CPI) for January 2026 and Real Earnings for January 2026 are slated for release on Friday, February 13, 2026. Various Federal Reserve officials, including Governor Stephen I. Miran and Vice Chair Philip N. Jefferson, are also scheduled to speak throughout the week. Numerous corporate earnings reports are also anticipated on Tuesday, February 10, 2026.

• Market Logic Projection:

The market's attention will largely center on the delayed January jobs report and upcoming inflation data, which will provide further clarity on the health of the U.S. economy and the Federal Reserve's potential policy path. The implications of the new Fed Chair nomination and its influence on monetary policy expectations will remain a significant factor. We anticipate a continued rotation from growth-oriented equities into small-cap and value segments, with the Industrial, Energy, and Consumer sectors potentially attracting more capital.

• Strategy & Allocation Recommendations:

Our internal committee maintains a preference for growth over value and large-cap over small-cap segments, while closely monitoring the Communication Services, Healthcare, Industrials, and Technology sectors for potential increased exposure. In fixed income, we recommend a neutral weighting in core bonds, favoring mortgage-backed securities (MBS) over investment-grade corporates.

• Risk Alerts:

Key risks deserving attention include ongoing interest-rate uncertainty, potential geopolitical flare-ups (particularly involving Iran), and the challenges associated with the maturing AI investment cycle. The delayed resolution of the government shutdown and its potential impact on future data releases also remains a concern. The possibility of a firmer interest-rate stance under the new Fed Chair nominee could introduce further market volatility.

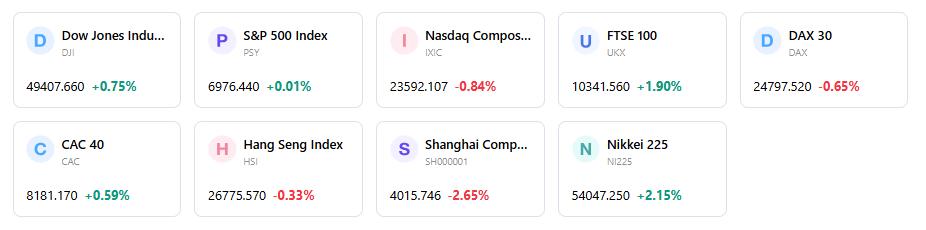

Markets Weekly

5-Day Index Performance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.