Borrowing $18 Billion! Oracle Bets Big on AI — Can Its Transformation into a “GPU Operator” Succeed?

TradingKey - Tech giant Oracle (ORCL.US) issued $18 billion in investment-grade bonds on Wednesday, marking the second-largest corporate bond deal of the year.

The entire sum will be funneled into building out its AI infrastructure, signaling the legacy software company’s accelerating transformation into a GPU-powered data center operator.

According to sources, the offering was divided into six tranches, including a rare 40-year bond. The final yield spread was set at 137 basis points over U.S. Treasuries — tighter than the initial marketing guidance of around 165 bps. The strong investor demand allowed Oracle to secure favorable terms, reflecting market confidence in its strategic direction.

“This is not the, ‘If we build it, they will come,’” Schiffman said of Oracle in an interview. “They’ve already come, contracts are in place, the demand is there. Now they just have to put the infrastructure in place. And I think that’s why people are so confident from the credit side, why they’re going to be able to borrow so much money at pretty reasonable rates.”

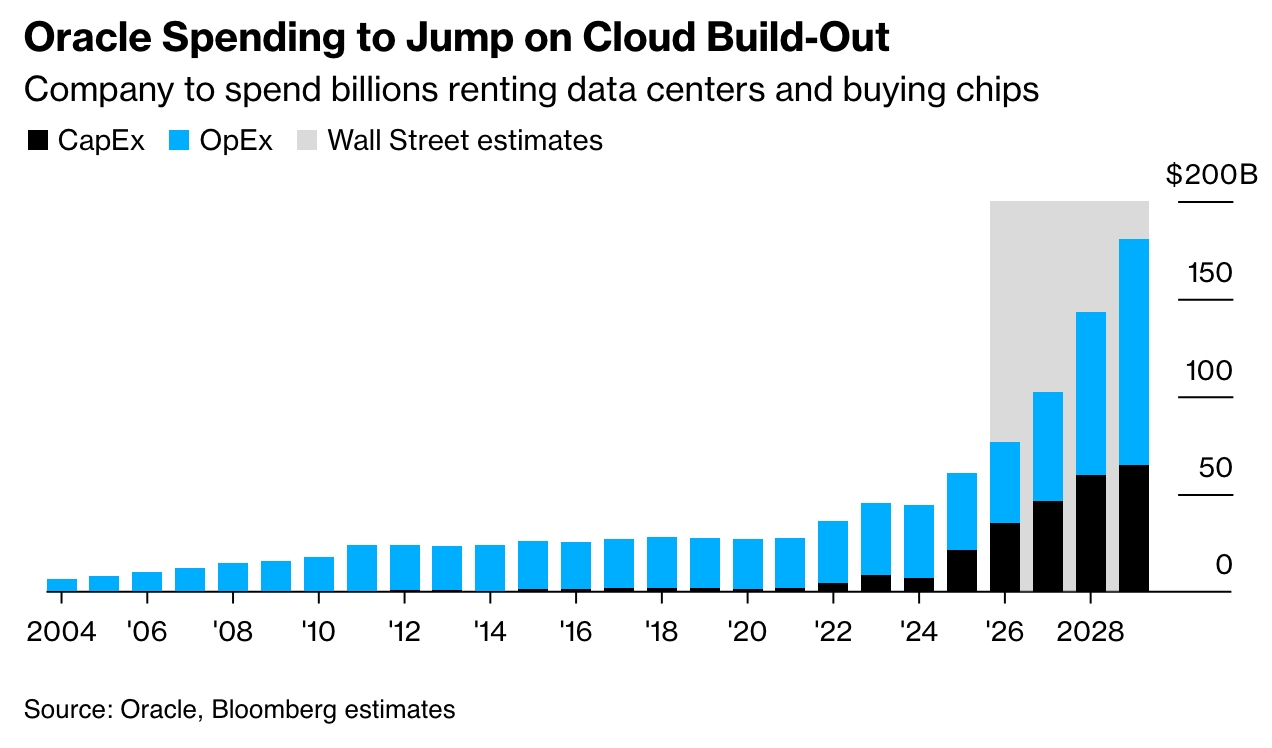

This debt raise comes as Oracle begins fulfilling massive cloud infrastructure deals with clients like OpenAI and Meta. The company is expected to spend hundreds of billions of dollars over the coming years on leasing, building, and operating data centers.

According to a recent Morgan Stanley report, Oracle’s cloud revenue could surge from about $18 billion today to $144 billion by fiscal 2030. AI-driven compute services alone are projected to account for 60% of total revenue, fundamentally reshaping the company’s business model. This outlook is underpinned by multi-hundred-billion-dollar contracts with tech giants and an RPO (Remaining Performance Obligations) backlog exceeding $450 billion, providing exceptional visibility into future growth.

Yet, this bet comes at a steep price. Morgan Stanley estimates that Oracle may need to invest up to $405 billion in capital expenditures over the next five years to deliver on its commitments.

Even more challenging is the shift in profitability. Oracle once generated high-margin income from software licensing with minimal incremental cost. The new AI data center business, however, is capital-intensive, with significantly lower margins. Morgan Stanley forecasts that Oracle’s operating margin will gradually decline from around 44% today to approximately 38% by 2030.

Overall, Oracle’s current stock price already reflects much of the bullish sentiment. Morgan Stanley argues that further upside will hinge on two key variables:

- Whether AI segment margins can exceed expectations

- Whether the company can effectively control costs and improve operational efficiency during rapid scaling.

For investors, Oracle is no longer just a stable “cash cow.” It has become a long-term, high-stakes bet on the future of global AI infrastructure — one whose success or failure will profoundly shape the competitive landscape.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.