Better Artificial Intelligence Stock: SoundHound AI vs. C3.ai

Key Points

Both SoundHound AI and C3.ai thrived thanks to customer demand for their artificial intelligence offerings.

SoundHound AI is experiencing significant revenue growth with Q2 sales up more than 200% year over year.

C3.ai stock sports an attractive valuation, and the company gained a new CEO.

The artificial intelligence (AI) sector is booming, leading to a surge of businesses touting AI expertise. Two such companies are SoundHound AI (NASDAQ: SOUN) and C3.ai (NYSE: AI).

SoundHound specializes in consumer-oriented AI voice solutions, such as the ability to take customer orders at restaurant drive-thrus. In contrast, C3.ai concentrates on enterprise AI applications for organizations, including the U.S. government.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Could one of these businesses represent a compelling investment opportunity in the hot AI sector? The answer isn't straightforward, so let's take a closer look at SoundHound and C3.ai.

Image source: Getty Images.

Unpacking SoundHound's success

SoundHound is experiencing robust revenue growth with second-quarter sales rising 217% year over year to $42.7 million. Its AI voice platform has been adopted by customers in sectors such as automotive, financial services, and restaurants.

Its strong sales performance prompted management to boost 2025's revenue outlook to between $160 million to $178 million. That's about double 2024's $84.7 million.

The company's sales are up thanks to strategic acquisitions made last year. However, the acquired businesses added to costs, resulting in a Q2 operating loss of $78.1 million.

Although the loss is substantial, SoundHound has $230 million in cash and equivalents with no debt on its Q2 balance sheet. This can sustain operations in the short term while it works to reduce expenses.

In fact, the company expects to reach adjusted EBITDA profitability by the end of the year. Its Q2 adjusted EBITDA was negative $14.3 million.

Dissecting C3.ai's current business

C3.ai's business model relies on partners such as Microsoft to help sell its AI solutions to businesses and governments. The approach worked well for its 2025 fiscal year, ended April 30, where it delivered record fourth-quarter revenue of $108.7 million, representing 26% year-over-year growth.

However, fiscal 2026 kicked off with a period of transition for C3.ai. CEO Tom Siebel had to relinquish his role for health reasons, and the company announced a new CEO, Stephen Ehikian, on Sept. 3.

In addition, C3.ai restructured its sales and services organization, disrupting the team's ability to deliver revenue. Adding to this, Siebel stated his health issues "prevented me from participating in the sales process as actively as I have in the past."

According to management, these factors led to revenue of $70.3 million in its fiscal first quarter, ended July 31, a decline from the prior year's $87.2 million. On top of that, Q1 operating expenses increased to $151.3 million from $124.8 million a year ago.

The combination of falling sales and rising costs is a concerning sign, and led to a Q1 operating loss of $124.8 million, up from the prior year's loss of $72.6 million. The situation looks like it will extend into fiscal Q2 as well.

That's because the company estimates fiscal Q2 sales to come in between $72 million to $80 million. While this is an uptick from Q1 revenue of $70.3 million, it's a notable drop from the previous year's $94.3 million.

Making a choice between SoundHound and C3.ai stocks

C3.ai's year-over-year revenue decline and current organizational upheaval point to SoundHound as the better AI stock to buy. Not so fast. Another factor to consider is share price valuation.

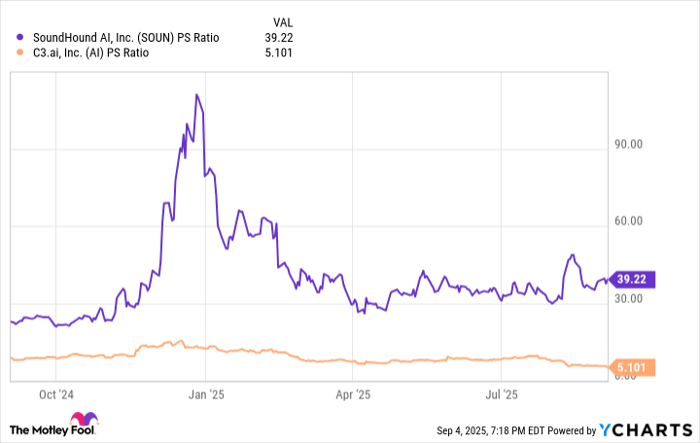

This can be evaluated using the price-to-sales (P/S) ratio, which measures how much investors are willing to pay for every dollar of revenue produced over the trailing 12 months.

Data by YCharts.

SoundHound's P/S multiple is sky-high compared to C3.ai's, which suggests SoundHound shares are pricey, although not as expensive as they were around the start of 2025.

Meanwhile, C3.ai's sales multiple indicates its stock price is at a reasonable level. With a new CEO and organizational changes designed to strengthen its sales channel, the company looks capable of bouncing back from its current revenue slowdown.

C3.ai also sports a strong balance sheet. Assets totaled $1 billion compared to total liabilities of $187.6 million. This includes cash, cash equivalents, and short-term investments of $742.7 million.

Yet C3.ai's attractive valuation comes with risk. Can new CEO Stephen Ehikian deliver the double-digit, year-over-year sales growth the company enjoyed under Tom Siebel?

Given this open question, SoundHound has the edge as the better AI investment right now, especially if it can maintain its strong sales growth while continuing down the path to profitability. But because of SoundHound stock's elevated valuation, it's best to wait for the share price to drop before deciding to buy.

Should you invest $1,000 in SoundHound AI right now?

Before you buy stock in SoundHound AI, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and SoundHound AI wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $670,781!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,023,752!*

Now, it’s worth noting Stock Advisor’s total average return is 1,052% — a market-crushing outperformance compared to 185% for the S&P 500. Don’t miss out on the latest top 10 list, available when you join Stock Advisor.

*Stock Advisor returns as of September 8, 2025

Robert Izquierdo has positions in C3.ai, Microsoft, and SoundHound AI. The Motley Fool has positions in and recommends Microsoft. The Motley Fool recommends C3.ai and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

Related Articles

Amazon Stock Predictions for 2026 to 2030: Will They Exceed Expectations and Achieve Major Long-Term Goals?

TradingKey - As we head into 2026, many investors are questioning where Amazon (AMZN) fits into the technology world.

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

USD Dollar Trend Forecast: Dollar Index Falls Below 97.0 to 4-Year Low, Will the Dollar Continue To Fall or Bottom Out in 2026?

TradingKey - In January 2026, the US Dollar Index continued its downward trend from 2025, officially breaking below the key 97.0 level and reaching a low of 95.5, marking a nearly four-year low since February 2022.