US NFP Nightmares Preview: A Tiny August Revision, a Huge Annual Benchmark Cut And a Fed in Flux

TradingKey - Whether it’s the July nonfarm payrolls report or Federal Reserve Chair Jerome Powell’s remarks at the Jackson Hole symposium, the message is clear: the U.S. labor market is weakening. Wall Street expects modest job growth and a rebound in the unemployment rate in August, a balanced outcome that could support a September rate cut. However, a massive downward revision — a “terrifying scene” — and anomalies on the supply side could plunge the Fed into deeper uncertainty.

This Friday, September 5, the U.S. Bureau of Labor Statistics (BLS) will release the August nonfarm payrolls report — the first since former BLS Commissioner Erika McEntarfer was removed by President Trump and the final key employment report before the Fed potentially restarts rate cuts.

According to Bloomberg, economists forecast:

- August nonfarm payrolls: +75,000

- Unemployment rate: 4.3%, up from 4.2% in July

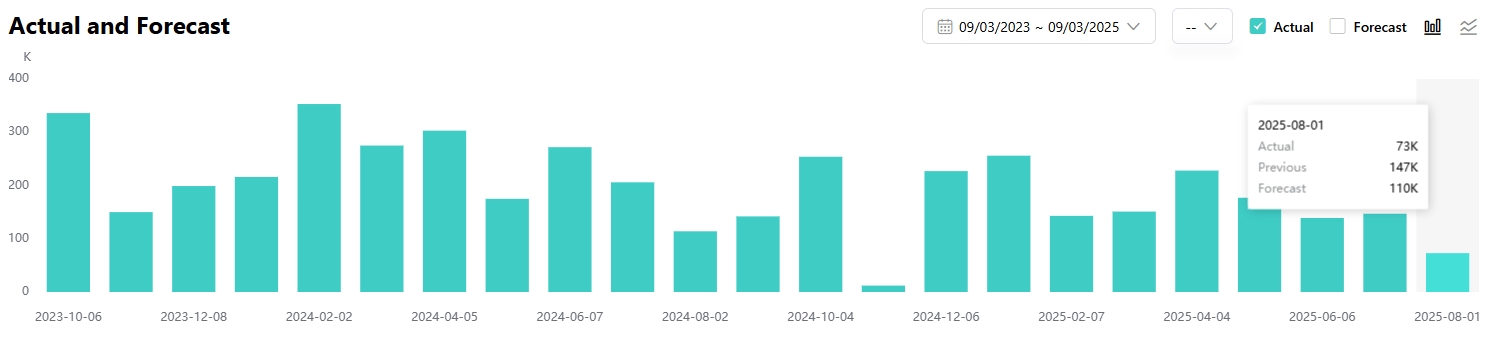

U.S. Nonfarm Payrolls, Source: TradingKey】

A slowdown in U.S. job growth has become a broad consensus among economists. Even Powell, who at the July FOMC meeting insisted he saw no signs of labor market weakness, reversed course by late August, acknowledging that downside risks to employment are rising.

Bank of America Merrill Lynch offered a relatively optimistic forecast, expecting 90,000 new jobs in August, well above July’s 73,000. The bank noted that the four-week average of initial jobless claims remains moderate, and continuing claims have declined, suggesting a slight rebound in job growth.

After Powell’s unexpected dovish turn at the end of August, BofA said that even if Friday’s report shows stronger-than-expected job growth, market pricing for a September rate cut remains firmly in place.

Bill Adams, Chief Economist at Comerica Bank, said the best-case scenario for financial markets would be modest job growth with a slightly higher unemployment rate — indicating the economy is not in recession, while labor market softness justifies Fed rate cuts.

However, Adams also outlined a worst-case scenario: falling employment, declining labor force participation, and a falling unemployment rate — suggesting both labor supply and demand are weakening.

Adams warned that the Fed may lack the tools to respond effectively in such a situation.

This “both weak” labor market dynamic — weak on both supply and demand — is exactly what Powell fears, which he described as a “strange balance.” Such an abnormal situation signals rising downside risks and could manifest as a surge in layoffs and a rapid rise in unemployment.

Watch for Downward Revisions to August’s Report

After the July report’s sharp downward revisions to the prior two months, the importance of historical revisions in assessing labor market health has grown.

BofA Merrill Lynch said market focus will center on the revision to July’s nonfarm payrolls. Given that every monthly report this year has been revised downward and survey response rates were low in July, the initial July figure of 73,000 jobs faces significant downside risk.

The bank’s analysts said that if July’s jobs are revised down again, it would suggest labor market weakness is more persistent than expected.

Morgan Stanley economists believe the Fed has already opened the door to rate cuts, but the size of the cut will depend on whether labor market risks continue to outweigh inflationary pressures.

Annual Benchmark Revision Faces “Collapse” Risk

Just days after the August report, the BLS will release its annual benchmark revision on September 9, covering the period from April 2024 to March 2025.

Wall Street expects this revision could cut up to 900,000 jobs, highlighting the extent of overstatement in U.S. employment data and the depth of labor market weakness. Last September, the BLS revised down 818,000 jobs.

Goldman Sachs pointed out that job overcounting stems from the BLS’s long-standing “birth-death model”, which fails to capture real-time employment dynamics, and from the decline in undocumented immigration affecting labor supply.

Goldman said the model overestimated job growth by 45,000 per month in H2 2024, while Standard Chartered estimated the overcount at 70,000 per month. In total, the annual revision could remove 550,000 to 800,000 jobs.

Nomura expects a downward revision of 600,000 to 900,000 jobs, citing similar issues with undocumented immigration and new business estimation. The Quarterly Census of Employment and Wages (QCEW) does not capture undocumented workers, while the nonfarm payrolls survey does.

However, Nomura downplayed the potential impact of this large revision on rate cut expectations and capital markets, calling it an expected dovish signal that investors and Fed officials have already priced in.

A 25-basis-point rate cut in September is now fully priced in, but some suggest that if more downward revisions emerge, a 50-bp cut is not out of the question.

Nomura said that unless there are mass layoffs or severe financial stress, it’s unlikely the Fed would deliver a 50-bp cut or multiple consecutive cuts.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.