U.S. IPO Profitability Test: Can Circle and CoreWeave Justify Their Surging Stock Prices?

TradingKey - On Tuesday, August 12, Circle (CRCL) and CoreWeave (CRWV) will respectively release their first and second earnings reports since going public. Both stocks have more than doubled since their IPOs in 2025, but concerns over their business models and profitability remain. The latest results will test the sustainability of their valuations.

As of writing, CoreWeave’s stock has surged over 250% since its late March listing, while Circle has risen fivefold since its June IPO, reflecting strong investor appetite for artificial intelligence and cryptocurrency sectors.

Retail investors played a key role in driving the rally for both IPOs, but over the past one to two months, several Wall Street firms have expressed skepticism about the companies’ business models and valuation outlooks, prompting investors to take profits. CoreWeave plunged about 40% in July, while Circle dropped over 20% in the second half of July.

Accounting firm Armanino said these quarterly results absolutely matter as one of the things that has stopped companies from filing for IPOs was the ability to forecast their results.

Circle: The Good and Bad of Rate Cuts

According to Bloomberg, analysts expect Circle’s Q2 2025 revenue to reach $647 million, with an adjusted EPS loss of $0.08 per share.

Circle’s revenue is heavily reliant on interest income from short-term U.S. Treasury securities backing its stablecoin USDC. From 2022 to 2024, income from managing stablecoin reserves accounted for 95.3%, 98.6%, and 99.1% of its operating revenue, respectively. As a result, Circle’s business “lifeline” is tied directly to Federal Reserve monetary policy.

Several Wall Street firms believe Fed rate cuts will pose risks to Circle’s business. Goldman Sachs estimates that for every 25-basis-point rate cut, Circle’s revenue could decline by 5.5% and EPS by 10.5%. JPMorgan projects that with $60 billion in USDC in circulation, a 100-basis-point drop in interest rates would reduce Circle’s reserve income by $600 million and EBITDA by $200 million.

In response to criticism over its single revenue stream, Circle said it will increasingly rely on non-reserve income, such as payment and transaction services.

On the other hand, looser monetary policy could boost market risk appetite and stimulate the cryptocurrency market where USDC is widely used.

JPMorgan updated its rate forecast last week, expecting the Fed to cut rates four times this year, for a total of 100 basis points.

Needham analysts said that under looser monetary policy, speculative activity in the crypto sector will increase.

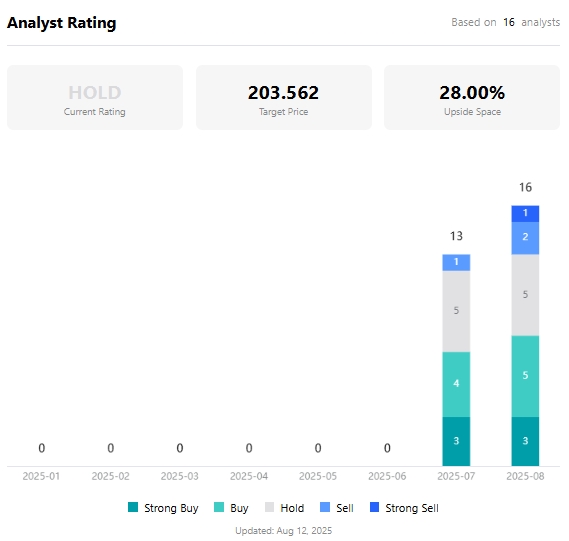

Given this, Needham issued a “Buy” rating with a target price of $250. According to TradingKey, the average analyst target price for Circle is $204, implying a 28% upside from current levels.

Analyst Target Prices for Circle, Source: TradingKey

CoreWeave: Is Capital Spending Overstated?

Analysts expect CoreWeave’s Q2 adjusted EPS loss of $0.23 per share and revenue of $1.082 billion, within the company’s guidance range of $1.06–1.1 billion.

CoreWeave’s core business is high-performance computing services based on Nvidia GPUs, operating AI data centers that provide on-demand or prepaid GPU computing power to companies such as Microsoft, OpenAI, Meta, and IBM for AI model training, inference, and high-performance computing tasks.

Nvidia holds about 7% of CoreWeave, giving the cloud provider a near-exclusive supply chain advantage — priority access to Nvidia’s most advanced chips.

To purchase more infrastructure to meet new customer demand, CoreWeave disclosed last quarter that its capital expenditures for the year could reach $20–23 billion. Since then, however, the company has raised only $5 billion in debt financing.

Some analysts point out that CoreWeave’s main challenge is fundraising, and it needs sufficient capacity to issue stock and raise more debt.

Bank of America analysts noted that CoreWeave is issuing large amounts of debt to maintain operational momentum in a competitive market, but rising debt burdens could erode profitability and remain the biggest concern for the company’s fundamentals.

According to Tipranks, the average analyst target price for CoreWeave is $108, implying a 17% downside from recent levels.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.