SMIC Q2 Revenue Up But Profits Shrink: How Capacity Expansion & Price Wars Squeezed Margins?

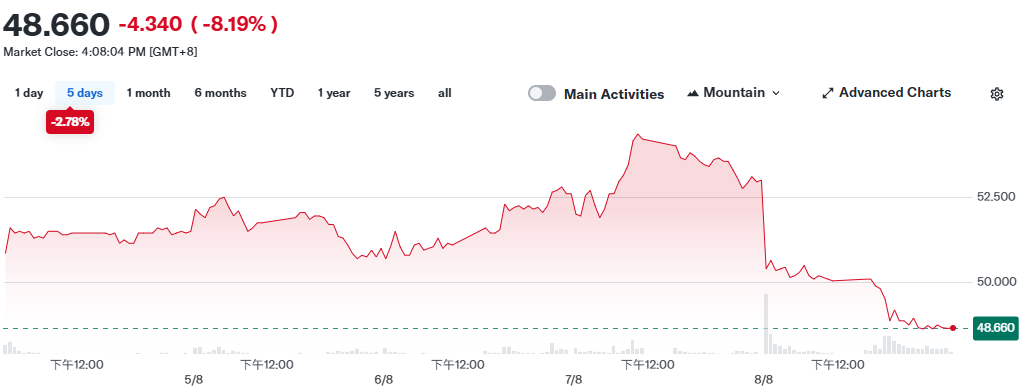

TradingKey - Semiconductor Manufacturing International Corporation (SMIC), China’s chip manufacturing leader, faced immediate selling pressure on August 8 following its quarterly results disclosure. Shares plunged 8.19% to HK$48.66 by press time.

Source: Yahoo Finance

Financial reports showed the company generated $2.209 billion in revenue for Q2, a 16.2% year-over-year increase.

Contrasting sharply with revenue growth, net profit declined 19.5% year-over-year to $132.5 million – missing market expectations and falling short of the $145 million average estimate from FactSet analysts.

SMIC management had publicly acknowledged production challenges in May that directly impacted yield rates for premium products. Fluctuating yields not only disrupted production efficiency but also weakened the company’s pricing power during client negotiations, dragging down average selling prices.

Secondly, intensifying pricing competition across the foundry sector persisted despite SMIC’s statement that order volumes still exceed current capacity. Management admitted the company "will not lead price hikes but will follow if peers adjust," reflecting ongoing price battles where foundries must carefully balance market share against profit margins.

Simultaneously, SMIC’s ongoing capacity expansion – critical for long-term competitiveness – inevitably drove up depreciation costs, exerting sustained pressure on short-term margins.

Q2 capital expenditures reached $1.885 billion, significantly higher than Q1’s $1.415 billion, further negatively impacting the company’s profit performance.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.