“King of Knockoff Weight-Loss Drugs” Still Struggling — Hims & Hers Misses Revenue, Stock Drops 12% After Hours

TradingKey - Despite a 73% year-on-year revenue increase in Q2 2025 that highlights the growth potential of the digital health sector, Hims & Hers (HIMS), a high-profile player in the AI-driven telehealth space, continues to face mounting legal and operational challenges. The negative impact on its weight-loss drug business appears more severe than analysts anticipated.

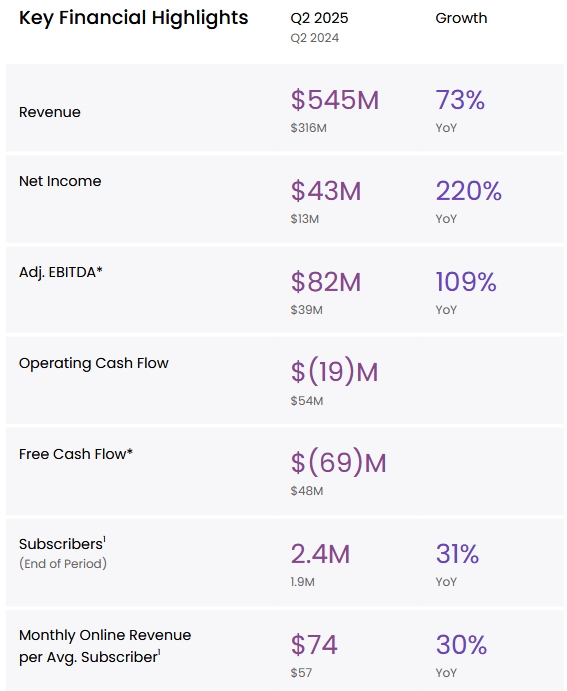

On Monday, August 4, telehealth provider Hims & Hers (referred to as Hims) reported its second-quarter 2025 results:

- Revenue: $545 million, up 73% YoY, but below the $552 million consensus

- Net income: $42.5 million, up 220% YoY

- EPS: $0.17, above the expected $0.15

Hims & Hers Q2 2025 Financial Metrics, Source: HIMS

The company projected Q3 revenue of $570–590 million, with a midpoint of $580 million, slightly below the $583 million forecast. It also expects Q3 EBITDA of $60–70 million, well below the $77.1 million consensus estimate.

Weight-Loss Drug Sales Weigh on Outlook

Analysts believe the underperformance in revenue and guidance stems primarily from ongoing challenges in its GLP-1 weight-loss drug segment.

Hims initially built its business on selling personal care and prescription products, including treatments for male hair loss, erectile dysfunction, and female contraception. In 2024, it launched compounded semaglutide — a cheaper, unapproved version of branded drugs like Ozempic and Wegovy — aiming to kickstart a “second growth curve.”

However, the weight-loss drug segment has since become a liability.

- In February 2025, after the FDA announced the resolution of shortages in branded GLP-1 drugs, Hims’ stock plunged nearly 30%

- In June, Novo Nordisk suspended supply to Hims, citing misleading marketing practices, dealing another blow to its weight-loss business and triggering another 30% drop

Sales Decline Despite Subscriber Growth

In Q2, GLP-1 drug sales fell from $230 million in Q1 to $190 million, even as the number of subscribers showed modest growth.

Investors are now closely watching how Novo Nordisk’s supply suspension and Eli Lilly’s ongoing lawsuits against compounding pharmacies could further impact Hims’ business model and regulatory risk.

Morgan Stanley noted that Hims could still benefit from:

- Strong user growth

- Expansion into high-potential areas like weight management and hormone replacement therapy (HRT)

- Margin improvements from platform scale and operational efficiency

But the firm also warned of downside risks, including:

- Ongoing drug supply shortages

- Intensifying competition from traditional pharma and digital health rivals

- Regulatory changes affecting compounding pharmacies and telehealth prescribing practices

Stock Volatility Continues

Despite the Q2 revenue beat and strong EPS, Hims’ stock dropped 12% in after-hours trading.

Year-to-date in 2025, the stock has surged 161.99%, reflecting investor appetite for high-growth telehealth plays — but the latest results show that sustainability remains in question.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.