Arm Shares Plunge 8% After Hours — Profit Warning and Chipmaking Pivot Raise Concerns

TradingKey - Arm (ARM.US) delivered a mixed first-quarter earnings report for its fiscal Q1 2026, sending its stock down over 8% in after-hours trading. While revenue beat expectations, profit declined sharply, and weak guidance for the next quarter raised concerns about the company’s costly pivot into AI and chip manufacturing — a strategic shift now facing investor skepticism.

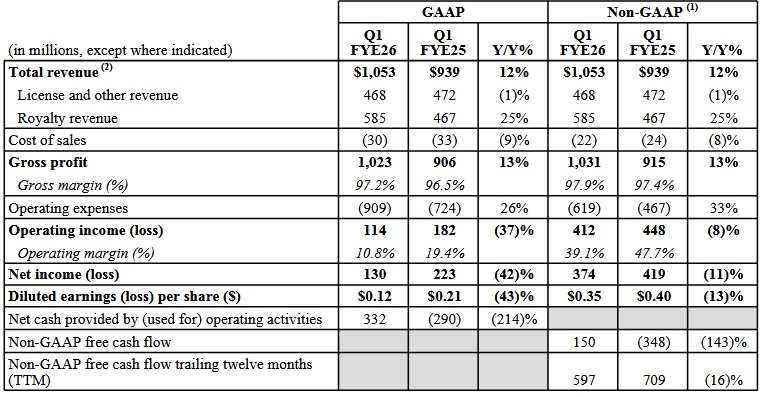

On Wednesday, July 30, Arm reported results for the quarter ended June 30, 2025:

- Revenue: $1.05 billion, up 12% YoY, slightly below the $1.06 billion consensus

- Net income: $130 million, down 42% from $223 million a year ago

- Non-GAAP EPS: $0.35, in line with expectations

Arm Q1 FY2026 Financial Highlights, Source: Arm

Arm said the quarter marked its second-highest revenue ever, and the best first-quarter performance in company history.

Revenue Breakdown: Royalties Strong, Licensing Soft

- Royalty revenue (from chip sales): $585 million, up 25% YoY — a record high

- License revenue (upfront design fees): $468 million, slightly down YoY due to timing and size of licensing deals, as well as fluctuations in backlog recognition

The decline in licensing revenue was expected, but investors are now focused on forward-looking risks — particularly profitability and future strategy.

Weak Guidance Sparks Sell-Off

Arm projected Q2 revenue between $1.01 billion and $1.11 billion, roughly in line with the $1.06 billion consensus.

However, adjusted EPS guidance of $0.29–$0.37 — with a midpoint of $0.33 — fell short of the $0.36 forecast, signaling margin pressure ahead.

CEO Signals Strategic Shift — But at What Cost?

CEO Rene Haas said the company is increasing investments beyond traditional chip design, positioning Arm for the AI-driven computing boom.

Hass said that they are investing aggressively to capture long-term growth in AI, data centers, and automotive. These investments will pressure near-term profits — but they’re essential for the future.

Currently, Arm’s revenue comes from two core streams:

- Licensing (55%): One-time fees from chipmakers for access to Arm’s architecture

- Royalties (45%): Ongoing fees based on sales of chips built using Arm’s designs

Haas revealed that Arm is exploring a bold new direction: developing small, modular chiplets — self-contained silicon blocks that can be integrated into larger custom chips or sold as standalone products.

This move would mark a fundamental shift — from a licensing-only model to a player in chip design and packaging, potentially competing directly with chipmaker giants.

However, Haas declined to share details on the type of semiconductor technology, manufacturing partners or launch timeline.

However, some analysts warn that Arm’s pivot carries significant execution and competitive risks:

- Entering a capital-intensive, low-margin segment where it has no track record

- Facing off against well-funded, vertically integrated rivals

- Diverting focus from its core, high-margin IP business

“This isn’t a natural extension; it’s a leap into the unknown,” said one semiconductor strategist.

Smartphone Growth Slows — A Core Challenge

Arm’s royalty revenue is heavily tied to the smartphone market, which is now under pressure from Trump’s tariffs and weaker-than-expected demand.

Arm CFO admitted that growth in the smartphone industry has not been as strong as we anticipated.

This was echoed by Qualcomm, another mobile chip leader, which reported that Q2 smartphone chip revenue grew just 7% YoY — down from 12% in Q1 and below expectations — contributing to weak overall revenue growth.

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.