Intel Q2 Revenue Up But Profits Stagnate: Can Razor-Thin Q3 Guidance Break Downward Spiral?

TradingKey - On July 25, Intel (INTC) reported its second-quarter earnings, with revenue exceeding market expectations. Still, net income and earnings per share (EPS) fell short due to impairment charges and one-time costs.

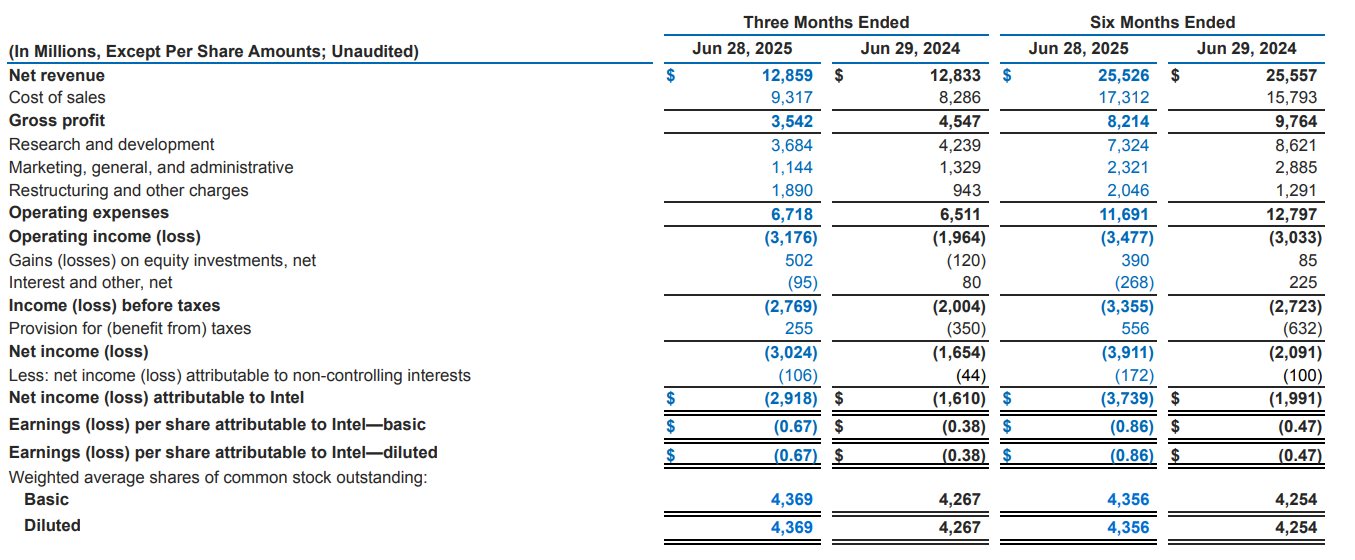

The company’s Q2 revenue reached $12.8 billion, surpassing Wall Street analysts’ previous estimate of $11.8 billion. Net loss widened to $2.9 billion, significantly deteriorating from last year’s loss of $1.61 billion.

Source: INTC

Among business segments, the foundry business emerged as the "hardest-hit area" dragging down overall performance. The segment reported Q2 revenue of $4.4 billion but suffered a loss of $3.17 billion.

In response to this severe situation, Intel CEO Lip-Bu Tan announced a series of adjustment measures, including canceling planned projects in Germany and Poland, slowing down construction progress of the Ohio facility, and reducing the 2025 total capital expenditure target from the originally planned $20 billion to $18 billion.

Tan stated that the company had invested "too much and too fast" in the past, leading to the underutilization of factories. Moving forward, the company will ensure that "every investment must be economically viable."

Looking ahead to Q3, Intel provided relatively positive guidance, forecasting revenue of approximately $13.1 billion, above the market expectation of $12.65 billion, and EPS is expected to reach a breakeven level, indicating potential improvement in the company’s operational performance.

Following the earnings release, Intel’s after-hours stock price initially rose 2% before turning negative, ultimately closing down 4.64%. From a longer-term perspective, Intel’s stock has declined 28% over the past 12 months, though it has still gained 13% year-to-date.

Source: Google Finance

Recommended Articles

Comments (0)

Click the $ button, enter the symbol, and select to link a stock, ETF, or other ticker.