2 Top Buffett Stocks to Buy and Hold in 2025

Warren Buffett made some big moves last year. The portfolio of his holding company, Berkshire Hathaway, saw some massive shifts in position sizes, including some huge selling of its biggest position. Moving into the new year, two Berkshire positions in particular look compelling right now.

This fintech stock is too cheap to pass up

Fintech stocks are growth machines, at least in theory. A company that offers financial services directly through a smartphone can, theoretically, scale much faster and more economically than a competitor relying on physical branches.

Start Your Mornings Smarter! Wake up with Breakfast news in your inbox every market day. Sign Up For Free »

The issue, however, is that asset-light businesses are often easy to start up. We've seen that in the U.S., where fintech businesses abound. Watch television or listen to the radio, and seemingly within minutes, you'll hear multiple ads for digital banks vying for your patronage. So while the category in general is growing and can be quite profitable, rampant competition has suppressed growth rates for individual companies and stymied their ability to scale profitability.

The exception to the rule has been Nu Holdings (NYSE: NU). While Berkshire Hathaway did trim its position last year, it still retains a $1.2 billion position in what I believe to be the best fintech stock on the market today.

Nu's secret isn't necessarily in its business model, but in its geographies of focus. The company is focused on just three markets: Mexico, Brazil, and Colombia. In the long term, it intends on expanding into much of Latin America, targeting the region's 650 million residents. The financial services industry of these markets varies greatly from more mature markets like the U.S. In less than 10 years, for instance, Nu has been able to go from nearly zero customers to commanding a 56% market share among Brazilian adults. Imagine more than half of Americans using a single bank. That's how much market power Nu commands.

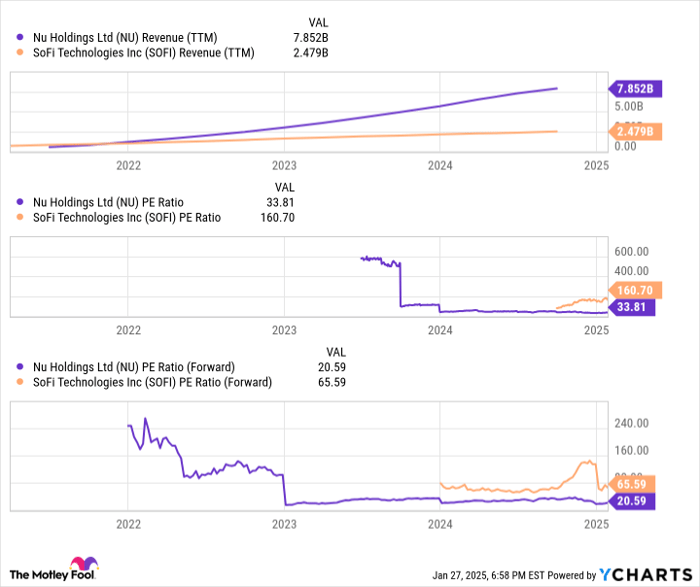

Compared to a U.S. competitor like SoFi Technologies, Nu has been able to maintain higher growth rates with superior profitability. Its growth journey has slowed due to market penetration, but shares now trade at just 33 times trailing earnings and 20 times forward earnings. That's a steal for a business expected to grow revenue by double digits for many years to come.

NU Revenue (TTM) data by YCharts. PE = price-to-earnings.

Bet alongside Buffett on this rebound stock

Warren Buffett cut his teeth as a value investor. Over the years, he has strayed further into other categories like growth investing. But when it comes to Berkshire's $2.4 billion stake in Sirius XM Holdings (NASDAQ: SIRI), this looks like a pure value play.

Sirius has dealt with stagnating revenues for many years now. It's generating the same revenue today that it did in 2022. But for the most part, the company has been profitable, with ample amounts of free cash flow over that time period. It has used the excess cash to aggressively buy back stock and support a growing dividend. After a 50% decline in share price over the last 12 months, that dividend now yields nearly 5%. On a forward earnings basis, the stock now trades at just 6.8 times next year's expected profits.

There's no doubt that Sirius XM shares are cheap. The high dividend yield, ample cash generation, and minuscule forward valuation should perk up the ears of nearly every value investor. Some stocks, however, are cheap for a reason. Streaming services continue to provide heavy competition to Sirius XM's satellite radio offerings. Management recently lowered its guidance for the coming years, predicting additional subscriber losses and lower-than-expected revenues. Free cash flow fell to $93 million last quarter from $291 million the same quarter a year ago, with full-year free cash flow guidance falling to just $1 billion.

Sirius XM's market cap is now just $7.4 billion, providing an exceptional free cash flow yield. While the business is struggling to grow, its strong financial situation -- even though slightly weakened -- should give it the firepower to either reinvent itself or sustain itself until subscriber growth reemerges. There's risk here, especially if guidance moves lower again this year. But the price seems right for risk-tolerant value investors like Buffett.

Should you invest $1,000 in Sirius XM right now?

Before you buy stock in Sirius XM, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sirius XM wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $735,852!*

Stock Advisor provides investors with an easy-to-follow blueprint for success, including guidance on building a portfolio, regular updates from analysts, and two new stock picks each month. The Stock Advisor service has more than quadrupled the return of S&P 500 since 2002*.

*Stock Advisor returns as of January 27, 2025

Ryan Vanzo has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Berkshire Hathaway. The Motley Fool recommends Nu Holdings. The Motley Fool has a disclosure policy.

Related Articles

Why Sanae Takaichi Winning Japan’s Diet Election Led to a Surge in Japanese Stock Indices?

TradingKey - Reports indicate that the ruling coalition led by Japanese Prime Minister Sanae Takaichi has secured a single-party majority in the parliamentary elections held on Sunday (February 8). Following the news, the yen weakened slightly, while the Nikkei Index surpassed 57,000 for the first t

A Crash After a Surge: Why Silver Lost 40% in a Week?

TradingKey - Spot silver (XAGUSD) prices continue to decline. Silver plunged 20% on Thursday, breaking below $71 per ounce, with the sell-off intensifying on Friday as prices fell further below $64. Compared to the all-time high set on January 29, silver prices have retraced more than 40%, wiping out nearly all gains accumulated over the previous month.

Is Bitcoin’s Four-Year Cycle Dead in 2026?

Is the Bitcoin 4-year cycle dead? After 2025 broke historical records with a red post-halving year, institutional analysts explore if the Bitcoin price has decoupled from the halving countdown. Analyze the impact of spot ETFs, global liquidity, and the roadmap to the 2028 halving in this 2026 market

Why Ripple ETFs are Winning the Capital War Against Bitcoin

While Bitcoin and Ethereum ETFs face massive outflows, XRP ETFs have defied market trends with a historic 30-day inflow streak reaching $1.37 billion. Explore why institutional "smart money" is rotating into Ripple, the structural impact of the "Liquidity Lock," and why analysts set a 2026 price tar